Brexit, Uncertainty and Pension Losses: there is a lot of that going around

You have to wonder what Brexit will be blamed for next. Even The Wall Street Journal on Monday reported on the front page, “Pensions Pressed Further by Brexit.”

The front-page article reported, “For officials who manage retirements of public and private-sector workers, Brexit exacerbated problems that have been roiling pensions around the world for years. The low-rate environment has pulled down returns, inflated funding gaps, encouraged larger investment risks and prompted plan officials to scale back future investment assumptions.”

Now “this problem is snowballing,” said Colorado Treasurer Walker Stapleton. The article explained, “Pensions determine their assets and liabilities through formulas that depend heavily on the fluctuation of interest rates. When those rates fall, investment returns suffer and obligations to future retirees become larger.”

To the extent that Brexit causes pension fund managers and legislators to get real about the assumptions they use to set funding and benefit policies, then it was a gift to public employees depending on those funds, and the taxpayers who are on the hook for shortfalls. So far most funds have only changed funding formulas (taking more from taxpayers and current employees) while leaving current retirees largely untouched (except for perhaps changes in their COLAs).

I can just imagine sitting in pension hearings this winter, and hearing the State Board of Investment and pension funds blame Brexit for their poor performance. Last year the excuse was that people are living longer. A few years ago, it was the market crash. It is never about the fundamentals of the plans.

I called a financial executive I correspond with on pensions to talk about this. He confirmed what was bothering me: it was not Brexit per se, that is Great Britain leaving the European Union, that will hurt the balance sheet for pension funds. It was that the Brexit vote was unexpected, and therefore caused uncertainty in the market. Here is how he put it: “Whenever there is uncertainty, there is a sell-off, or a flight to liquidity.”

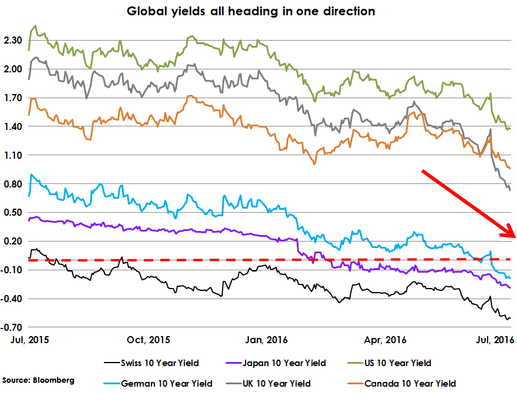

Things are settling down, at least across the pond (Great Britain’s new Prime Minister Theresa May has curtsied before Queen Elizabeth and so forth), and the equity markets not only recovered but soared. So there is a bump for the funds even if we are still operating in this never-ending zero interest rate environment where the yield on bonds continues a steep decline.

My financial expert put it this way, “Brexit did not change the fundamental flaws of public pension funding. Brexit just highlighted one of the flaws: public pension funds in particular have pegged their assumed rates of return well above what the market has produced or is expected to produce, and there is no way to catch up, even if you threw everything into a risky alternative and closed your eyes.”

Pension funds around the country have been slowly adjusting to the new market reality, slowed by the awful fact that when you drop the assumed rate of return, it means the reported unfunded liability grows. Then it gets harder to hide behind excuses.

The article reported, for example, “New York City reduced its return target to 7% in 2013, but that assumption is likely still unrealistic, said Lawrence Golub, a financier and member of the New York State Financial Control Board, which monitors the city’s finances. The assets returned 3.5% in fiscal 2015.

“The 7% is too high for planning purposes,” he said. “It’s not conservative.”

To bring it home: most of Minnesota’s public funds recently shifted from 8.5% to an 8% assumed rate of return (with Teachers TRA still stuck at 8.5%), remaining a stubborn outlier in the nation. That means, among other things, that the contributions coming into the funds are too low, and the unfunded liability of about $16 to $17 billion is wildly underestimated.

And as I have pointed out many times, it also means that taxpayers and current public employees are being asked to pay more and more to make up the shortfall. The taxpayer is getting less in terms of public services while paying more– and oh by the way, will not share in that guaranteed pension she is funding.

Similarly, many public employees will leave their jobs before they have vested, thus contributing to someone else’s retirement but not securing their own. These funds are so back loaded that if you do not stick around for 25 to 30 years, you do not get much in the way of a benefit. In fact, the plans are designed around the assumption that people will leave their money on the table.

Just as I cheered on the Brits as they said “Cheerio” to the bureaucrats and union officials running their lives from Brussels, I would encourage young public employees to demand their own Brexit from the sclerotic defined pension system. It was not designed with their mobility or retirement security in mind, and like the EU, is designed and run by old-fogey bureaucrats and union officials in St. Paul.

It will be a bumpy ride but just maybe the uncertainty of 2016 will bring reform to many institutions, including public pensions.