The Coronavirus crisis is highlighting a problem that existed well before the pandemic: promised pensions states can’t afford

As the coronavirus continues to unfold, so do questions about the extent of its impact on government, the economy, our every day lives, and even retirement.

There was a time when pensions were better funded, but unfortunately due to mismanagement, budget problems, not measuring assets and liabilities accurately, etc., public pensions have been severely underfunded for decades and face funding deficits nationwide.

Given the economic devastation COVID-19 has unleashed, the cost of underfunding pensions is now even more in the spotlight. We have promised pensions we cannot afford, and the fiscal state of public pension systems has reared its head as a financial tapeworm. According to the Tax Foundation, “Replenishing these funds will be extremely challenging now, as state revenues decline; states that failed to use more than a decade of economic growth to shore up their funds will be in particularly poor shape now.”

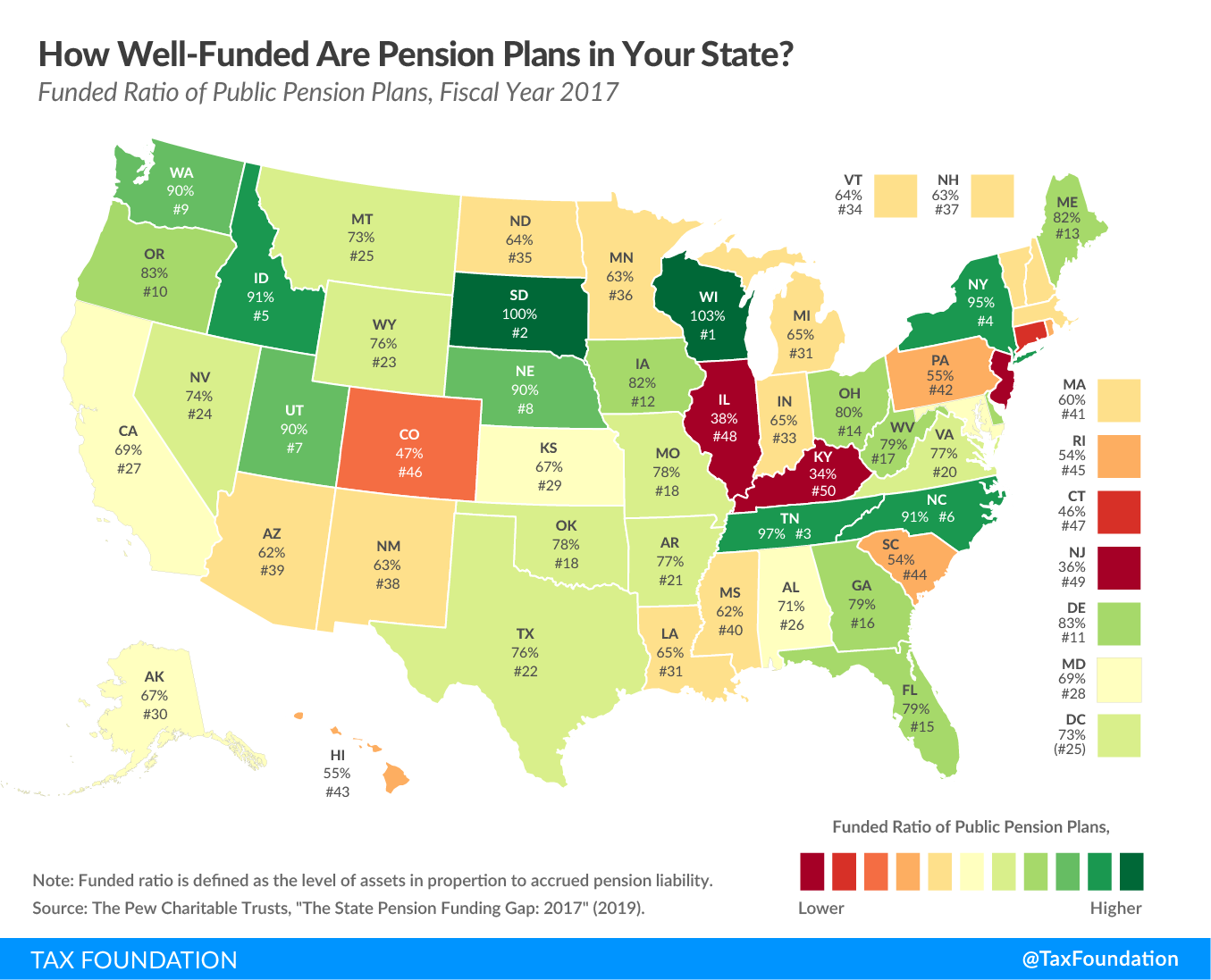

The map below shows the funded ratio of each state’s public pension plans using the most recent data available from FY 2017. Minnesota ranks #36, with 63 percent of its public pension plans funded. Our neighbors Wisconsin and South Dakota are doing the best, with funded ratios at 103 and 100 percent.

While pension plan structures vary from state to state, “historically, most states have provided some form of defined benefit plan that promises retirees a lifetime annuity,” continues the Tax Foundation.

The differences in the funding levels are largely driven by policy choices. The Center has long warned legislators about the trouble Minnesota’s public pension system is in. Our unfunded liabilities per capita are at $20,149 according to calculations by the ALEC Center for State Fiscal Reform. This means every resident in the state is on the hook for $20,149 and will most likely face future tax burdens to assist in fulfilling unfunded promises.

Once the coronavirus crisis passes, Minnesota needs to consider switching to more fiscally responsible pension plan structures, such as a defined contribution plan or even a hybrid pension plan that offers a small defined benefit pension plan in tandem with a defined contribution plan, similar to a 401(k). The pervasive pension underfunding not only affects current and retired public employees but taxpayers who provide the wages for government employees and help financially cover the promised benefits of defined benefit pension plans.