Gov. Walz’s corporate income tax hike would give MN highest starting rate of corporate income tax — faced by smaller businesses — in the U.S.

One of the measures proposed by Gov. Walz in his budget is a hike in Minnesota’s corporate income tax rate from 9.80 percent on the first dollar of taxable revenue to 11.25 percent. We have written that this would bump us up from having the fourth highest top rate of corporate income tax in the United States to having the second highest.

Minnesota has the joint third highest rate of corporate income tax in the United States

That number comes from our recent report ‘Closing Minnesota’s Budget Deficit: Why we should make spending cuts and not raise taxes‘ and was based on analysis using numbers for 2020, then the most recent available. Our state’s top rate of corporate income tax was lower than only Iowa’s, New Jersey’s and Pennsylvania’s.

Now we have the numbers for 2021, shown in Figure 1. As of Jan. 1st, 2021, Minnesota’s top rate of corporate income tax is lower than only New Jersey’s and Pennsylvania’s. We have risen to joint third in the rankings before enacting Gov. Walz’ proposed hike. Minnesota’s ranking has risen because Iowa’s has fallen, thanks to a cut in their top rate from 12.00 percent to 9.80 percent – why did they pick that rate, I wonder?

Figure 1:

Iowa’s move is part of a broader trend towards lower rates of state corporate income tax. The Tax Foundation notes several notable changes for 2021:

-

Arkansas saw its rate drop to 6.2 percent on January 1, 2021 as a third phase of tax reforms started in 2019 kicked in. This rate is scheduled to decrease even further, to 5.9 percent in 2022.

-

Colorado voters approved Proposition 116 in November, retroactively lowering the corporate income tax from 4.63 to 4.55 percent as of January 1, 2020.

-

Indiana’s rate decreased to 5.25 percent on July 1, 2020, and a final reduction to 4.9 percent is scheduled to kick in July 1, 2021.

-

Iowa has lowered its rate from 12 to 9.8 percent through a tax reform package adopted in 2018 and the repeal of federal deductibility.

-

Mississippi continues phasing out its 3 percent corporate income tax bracket by increasing the exemption by $1,000 a year, exempting the first $4,000 of income in 2021. The 3 percent bracket will be completely eliminated by the start of 2022, but the 4 and 5 percent brackets remain in place.

-

New Jersey Gov. Phil Murphy (D) retroactively increased and extended the state’s temporary surcharge on corporate taxable income exceeding $1 million. The surtax had decreased to 1.5 percent in 2020 and was scheduled to sunset by 2022. Instead, Assembly bill 4721 retroactively restored the surtax to 2.5 percent for tax years 2020 through 2023. As a result, New Jersey’s top corporate income tax rate, which would have been 10.5 percent for 2020 and 2021, and 9 percent with the expiration of the temporary surtax, is now 11.5 percent through 2023.

Only New Jersey is moving in the same direction as Minnesota. Given these trends towards lower rates across the United States, Gov Walz’ proposed hike will put Minnesota’s businesses at an even greater disadvantage.

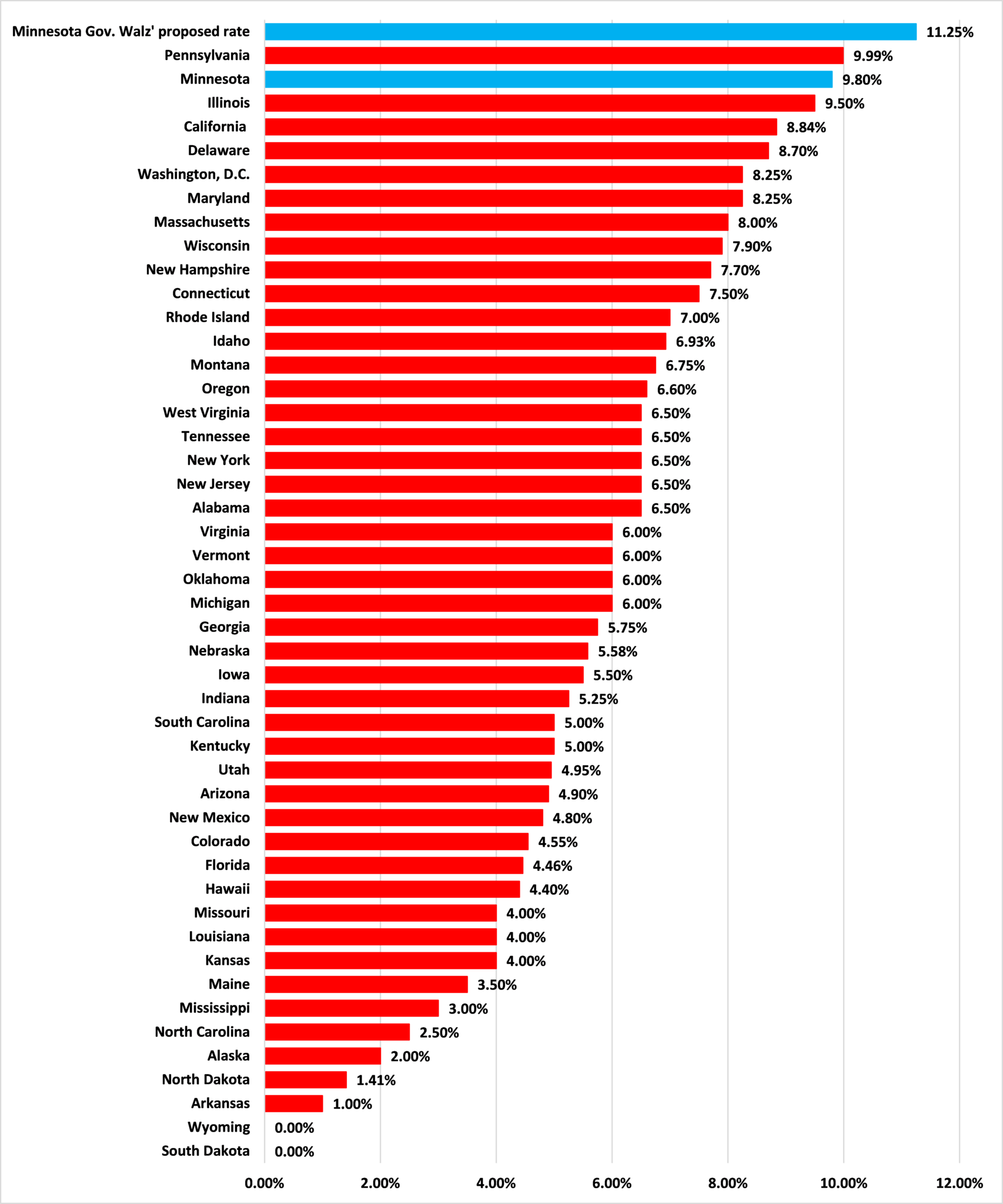

Minnesota has the second highest starting rate of corporate income tax in the United States

What do we see when we look at the bottom rates, the lowest tax rates that states impose on corporate incomes? For example, Minnesota imposes a rate of 9.80 percent on the first dollar of taxable income but in New Jersey that first dollar is taxed at only 6.50 percent; its top rate of 11.50 percent only applies to income over $1 million. In states with graduated rates, like New Jersey, companies with lower incomes can face a lower rate of corporate income tax.

Figure 2 shows that among 46 states and the District of Columbia, Minnesota’s lowest rate of corporate income tax — 9.80 percent remember — ranks second highest (the median rate is 6 percent). And, as Figure 2 also shows, Gov. Walz’ corporate income tax hike would give Minnesota the highest starting rate of corporate income tax — that faced by smaller businesses — in the United States.

Figure 2: Bottom rates of state corporate income tax, 2021

Source: The Tax Foundation. Nevada, Ohio, Texas, and Washington do not have a corporate income tax but do have a gross receipts tax with rates not strictly comparable to corporate income tax rates.

This is just one more reason why a hike in Minnesota’s corporate tax rate would be bad policy for our state.

John Phelan is an economist at the Center of the American Experiment.