81% of economists agree that rent controls are bad policy

President Harry Truman is supposed to have asked for a one-armed economist to be brought to him. That way they wouldn’t be able to say “But, on the other hand…”

If you laid all the economists in the world end to end, they wouldn’t reach a conclusion.

According to Winston Churchill, if “you put two economists in a room, you get two opinions, unless one of them is Lord Keynes, in which case you get three opinions.”

Which flavor of economics today?

These three witticisms probably sum up what most people think of economists. Should taxes be higher be higher or lower? Should spending be raised or cut? What should the Federal Reserve do with interest rates? You could find respectable enough economists to give you conflicting answers on each of these questions. In comparison to ‘hard’ sciences such as physics, where knowledge does seem to advance, you often find that economists are stuck having the same debates as they were when Keynes faced Hayek or when Say faced Malthus. In the last ten years, in the wake of the financial crisis and during the slow recovery, these debates have been especially – and publicly – bitter.

This lack of consensus provides ample excuse for those who deny that there is any validity to economics at all. With so many views on offer, you can just pick which one suits you best. By contrast, the law of gravity gives you little choice over whether you fall down the steps or up them.

Looking back over the history of science, even hard sciences, it is strange to take ‘consensus’ as a litmus test for the scientific validity of a discipline. But assuming that it is, there are, in fact, areas where the economists’ cacophony dies down and they speak with more or less one voice.

The economics of price ceilings – Rent controls are bad policy. Everyone says so.

One such area is rent control. This proposal – to cap the price landlords can charge tenants – crops up perennially as a solution to high rents. This is mistaking the symptom for the illness. When prices are high they are sending you information. They are telling you that demand is high relative to supply. If you want to do something about this, act to either reduce demand or increase supply. Either way, trying to fiddle with the signal makes no more sense then trying to slow down your car by breaking the speedometer.

Economists recognize this. They also recognize, in this area at least, that if you cap the price below the market rate all you do is increase demand relative to supply, exactly the situation you wanted to avoid.

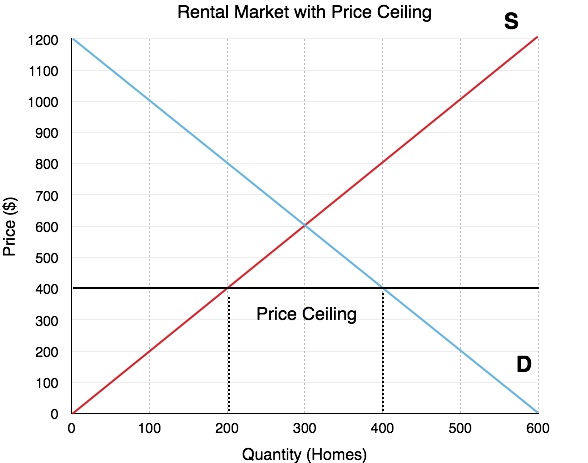

Figure 1 illustrates this. The market clearing price – where supply meets demand – is $600. At that price, 300 homes are both supplied and demanded. But when the price is capped at $400, more buyers come into the market and demand rises to 400 homes. At the same time, suppliers find it less worthwhile to supply housing and so supply falls to 200 homes. Sure, prices are lower (excepting all the additional fees), but there are fewer units to buy. There is no solution to ‘unaffordable housing’ that doesn’t involve either shifting the supply curve to the right or the demand curve to the left.

Figure 1

This isn’t just theory. In the post-war period rent controls were in operation in many American cities. By reducing the return to landlords it made sense for them to let their properties go to rack and ruin. This was a major source of ‘urban blight’. As the economist Assar Lindbeck put it, “In many cases rent control appears to be the most efficient technique presently known to destroy a city—except for bombing.”

So strong is the evidence for this that we have that rarest of things – a consensus among economists. In 2012, economists were polled with the following question;

Local ordinances that limit rent increases for some rental housing units, such as in New York and San Francisco, have had a positive impact over the past three decades on the amount and quality of broadly affordable rental housing in cities that have used them.

81% of them disagreed.

If consensus is how you do your science, ‘rent control’ is a dead duck.

John Phelan is an economist at the Center of the American Experiment.