A closer look at the nickel supply chain

On Monday, American Experiment described how the rising demand for nickel is resulting in expanded mining for the essential metal in a rainforest in the Philippines. Today, we will take a deeper look at the nickel supply chain, and how it will be affected by policies that mandate the use of electric vehicles and grid-scale battery storage for electricity.

According to an article by McKinsey, global nickel consumption is projected to increase from 2.2 million metric tons today, to 3.5 to 4 million metric tons by 2030. A recent study from the International Energy Agency states that EV and battery storage will consume more nickel than the stainless steel industry by 2040, meaning these applications will be responsible for much of the rise in nickel demand.

The main challenges for obtaining this nickel outlined in the McKinsey article are the ability to provide nickel that is of a high-quality Class 1 designation, and is easily accessible.

The quest for Class 1 nickel

The McKinsey article discusses two types of nickel: Class 1, which has few impurities, and Class 2, which has more of them. The “cleanliness” of the metal has important implications for how it is used:

Class 1 nickel production sees about 70 percent originating from sulfide ores, which are concentrated, smelted, and refined, and approximately 30 percent from limonite ores, which are leached commonly using high-pressure acid leaching (HPAL). Class 2 nickel is produced from saprolites and limonites, which are popular for their use in the stainless-steel industry due to their iron content and potentially low production costs.

For the emerging EV-battery industry, however, the type of nickel—whether it is Class 1 or Class 2—is of the utmost importance. The quality of the nickel used defines the quality and performance of the batteries. While the stainless-steel industry can, to a certain extent, use a mix of Class 1 and Class 2, the battery industry can only use Class 1. Furthermore, following concerns about the origins of another battery raw material, cobalt, EV manufacturers and their clients are seeking to ensure that the raw materials used in their products are mined and refined in an environmentally friendly manner, with positive impacts on local communities, and with a limited carbon footprint.

The main concern with regard to the quality of the nickel that ends up in nickel-rich cathodes is the presence of iron, though other contaminants such as copper also need to be separated. Class 2 nickel and low-quality mixed hydroxide precipitates are accordingly ruled out—at least with today’s technology. Consequently, at best only 46 percent of the world’s nickel production—Class 1 nickel—can be used in batteries

Providing enough Class 1 nickel that is mined in an environmentally responsible way is challenging because the vast majority of the nickel mined globally is conducted in developing countries that tend to have fewer protections for workers or the environment.

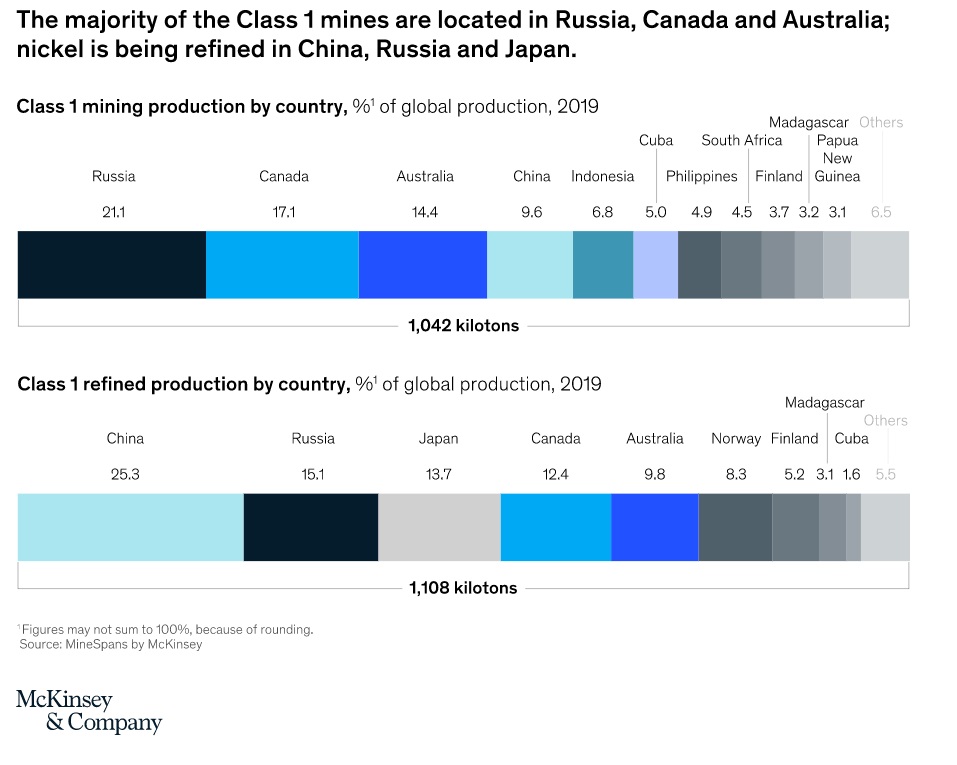

Russia is the leading producer of Class 1 nickel, with Australia, Canada, and Finland supplying about 35 percent of the market. This leaves little oversight of the rest of the Class 1 nickel supplies coming from mines in other nations.

Environmental oversight for nickel refining is also challenging because China and Russia constitute about 40 percent of global Class 1 refined nickel production. Fortunately, Japan, Canada, Australia, Norway, and Finland are also major refiners of this metal that will be increasingly short of supply as governments unwisely ban the sale of new internal combustion engines.

Such a forced transition to electric vehicles and grid-scale battery storage would require an enormous amount of new nickel mining, and based on how long Minnesota’s proposed copper-nickel mines have been in the permitting process, it is unlikely that the United States will do its fair share to make sure the nickel is produced in an environmentally responsible way.