A new bill would permanently cut income tax rates for most Minnesotans

The 2022 legislative session only started two days ago, and a myriad of bills have already been introduced. Among those introduced are two bills that deal with permanently cutting individual income tax rates.

Representative Erik Mortensen introduced bill HF2850, which would gradually phase out the corporate and individual income taxes by December 2026. Currently, only eight states impose zero income tax rates, and only five impose neither a corporate nor an individual income tax. To say the least, given our high tax rates, such a bill is unlikely to garner much traction.

Fortunately, other representatives –– Jerry Hertaus, Greg Davids, Bob Dettmer, John Petersburg, Dale Lueck, Pat Garofalo, and Josh Heintzeman –– have introduced bill HF2968, a more reasonable bill which would make the following changes:

- Reduce the tax rate for the first income bracket from 5.34 percent to 4 percent

- Reduce the tax rate for the second income tax bracket from 6.8 percent to 6 percent

- Reduce the tax rate for the third income tax bracket from 7.85 percent to 7 percent

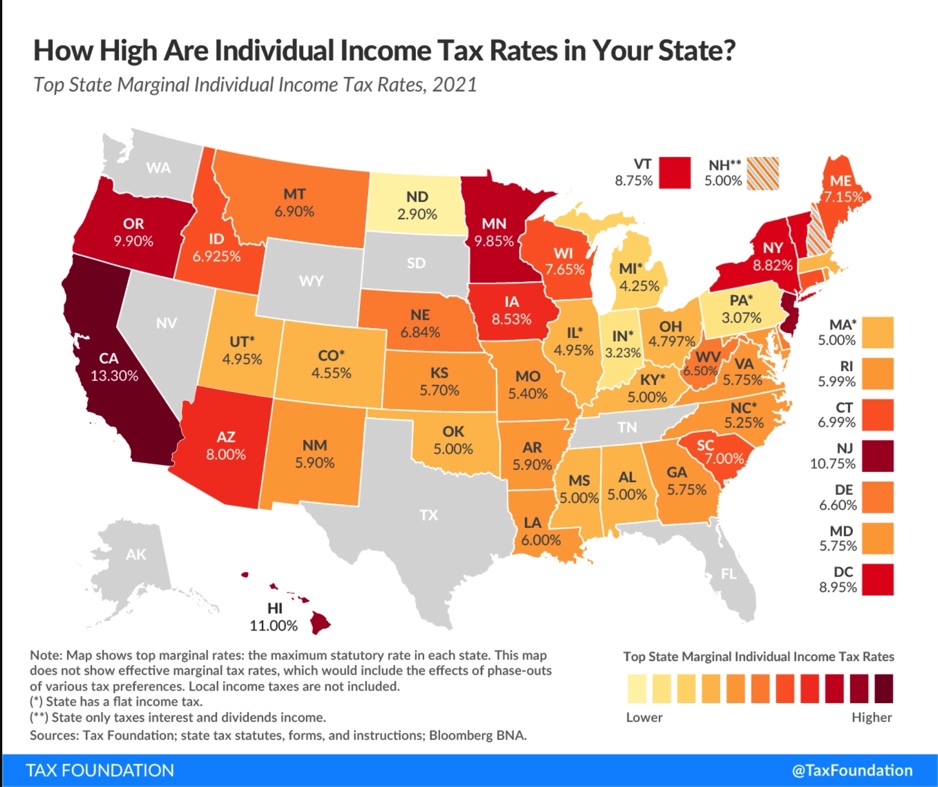

- No changes to the top income tax bracket, which has a rate of 9.85 percent.

Minnesota is one of the most heavily taxed states in the nation. So permanently cutting tax rates, especially in light of a large surplus, is a no-brainer. Lower tax rates would go a long way in making our state more competitive in attracting highly skilled workers as well as investments.

The bill, however, does not go far enough, especially when we compare Minnesota to other states. Minnesota taxes everyone heavily, including low-income earners. In our report, we noted that as of 2020, Minnesota’s lowest tax bracket was higher than the top rate in 25 states –– eight of which did not levy any income tax. There is a lot of room for legislators to cut tax rates further before we can get in line with other states.

Additionally, in 2019, the top income bracket in Minnesota was the 4th highest in the nation, only surpassed by California, New Jersey and Oregon. Considering that high-income taxpayers pay the majority of state income taxes, legislators also need to address the states’ top income tax rate.

Reducing the state’s high top rate would further incentivize more investments in the state, and thereby improve economic growth.