About that $18 billion surplus…

Late last night details began emerging of the budget deal struck between House and Senate negotiators. If you were wondering where that forecast $18 billion budget surplus is going to go, it looks like very little of it will be staying with the taxpayers it is forecast to be taken from.

“Not everyone will see a tax cut under the bill,” the Star Tribune reports somewhat coyly. Indeed, the only people who will see a tax cut are seniors, with couples earning up to $100,000 in annual income exempted from state tax on their Social Security income.

Indeed, even with an $18 billion surplus, the state government plans to raise taxes. The Pioneer Press reports that:

The legislation, which still needs to be reapproved by the House and Senate, includes more than $500 million a year in new revenue from corporations, dividends and investment income.

As MPR News explains:

Members of the tax conference committee said they’d agreed to implement a global intangible low-taxed income (or GILTI), a tax that would pull in more money from businesses with global earnings.

People who make money on investment earnings such as stocks would also see a tax hike under the plan. Overall, the changes are expected to bring in an additional $1 billion over four years.

There is reason to doubt that these tax hikes will, in fact, bring in the promised revenue. As Timothy Vermeer of the Tax Foundation notes of GILTI:

The addition of GILTI to the corporate tax base would make it more expensive for corporations to operate in Minnesota. To date, Minnesota has been able to retain a relatively large number of Fortune 500 companies despite having the second highest corporate income tax rate in the country, because that rate is only applicable to the profit the company generated from in-state sales. Taxation of GILTI income would undermine that advantage and incentivize these corporations to reduce their exposure to Minnesota’s tax system, favoring the 27 states that do not tax GILTI or do not impose a corporate income tax. And even compared to peers that also tax some portion of GILTI income, Minnesota’s unusually high corporate income tax rate makes the burden more substantial than it would be elsewhere.

And as he notes of the new tax on net investment income:

…the revenue estimate is based on static scoring—as if the present economic conditions and population composition over the coming biennium were to remain unchanged. We know from data and research, however, that people respond behaviorally to tax changes. If taxes on capital go up, people tend to invest less or relocate to jurisdictions where the return on investment is higher. If taxes on capital go down, people tend to invest more and move into that jurisdiction since the return on investment is higher. Not everyone makes these decisions at the same point or all at once, but eventually they do make them.

Perhaps that misses the point. As House Tax Committee chair Aisha Gomez (DFL) said during hearings on a previous proposal to hike Minnesota’s corporate taxes, “Whether [it] raised $1 or $1 billion dollars, it is the right thing to do.” It is dismaying, however, to see Sen. Rest (DFL), one of the most knowledgeable legislators on tax, go along with these fantasies.

Some dare call it a “tax cut”

No doubt you will be hearing much about how this bill “cuts taxes.” The Pioneer Press reported on “…other tax reductions [which] are designed to help families and lower-income residents. They include a larger tax credit for families with children and a new tax credit for renters.”

As I’ve noted before, handing out a bunch of cash is not a “tax cut” in any meaningful sense.

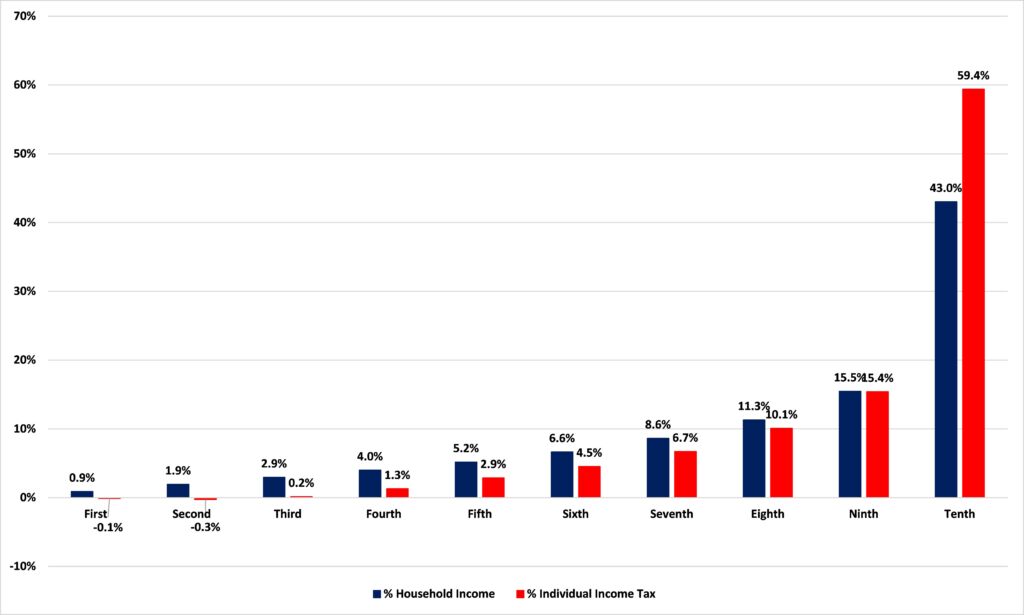

The measures in question include a new child tax credit that will give families $1,750 per dependent, which will start phasing out at $35,000 in annual income for couples. But, as the Department of Revenue’s most recent Tax Incidence Study shows, in 2018 the bottom 20% of Minnesota households by income, those earning up to $21,235 annually, actually had negative state income tax liabilities — they took out more than they paid in — thanks to the existing system of credits (See Figure 1). It is certainly possible to give these households more money, which is what this measure does, but it isn’t possible to ‘cut’ someone’s taxes if they aren’t paying taxes in the first place.

Figure 1: Share of state’s income earned and share of state’s individual income taxes paid by income decile, 2018

This isn’t a tax cut, it is a vast new welfare program. Whether that is a good or a bad thing, let us at least be honest about exactly what it is.