Census Bureau survey shows individuals increasingly saved their stimulus payments

When the federal government passed three stimulus bills and sent stimulus checks, concerns were raised about the necessity of continuing such payments. This was largely because by mid-2020, it had become reasonably clear that job losses were concentrated in low-wage jobs. Universal stimulus checks were, therefore, poorly targeted.

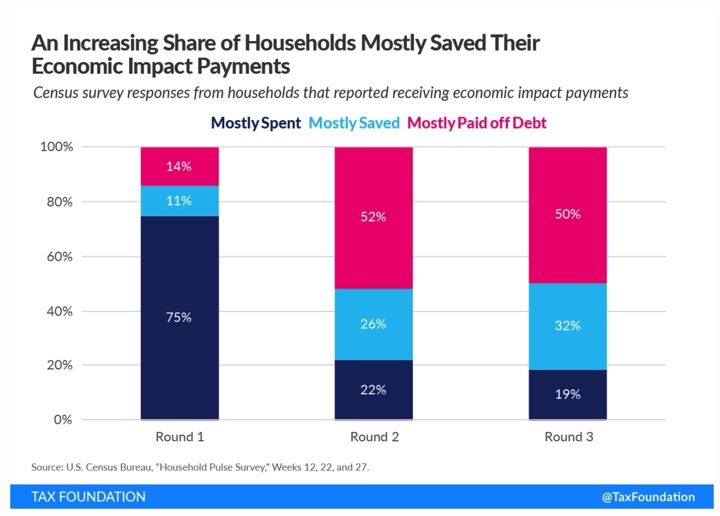

Data from the U.S. Census Bureau showing how people spent these checks proves that this concern was well-founded.

According to an analysis done by the Tax Foundation, “while the largest share of households reported using their payments for necessities like food or other living expenses”, as the pandemic went on, “households increasingly saved their EIPs or used them to pay down debt.”

Indeed, 75 percent of respondents reported using their first payment for consumption — potentially a sign that the checks alleviated some hardship.

However, by the third check, only 19 percent of recipients used the check for consumption. Instead, half used the money to pay off debt. Close to a third saved their income.

Stimulus payments, especially the later ones, had little to do with helping distressed individuals deal with pandemic-related job losses. Looking at how high-income individuals used their payments helps illustrate this point.

In the first round of payments, 84 percent of households with less than $50,000 in household income said they spent their payment, compared to 56 percent of households reporting more than $200,000 of income. By round three, 18 percent of lower-income households mostly spent their payments, compared to 20 percent of higher-income households. In the second and third rounds, using the payments to pay off debt was the most common reported use for households making under $200,000.