Bipartisan MN Senate tax bill isn’t a ‘tax cut for the rich’

The State Senate passed a tax bill on Thursday that, among other things, would cut Minnesota’s bottom rate of state income tax from 5.35 percent to 2.80 percent. Refreshingly in these fractured times, the bill received cross-party backing: it got the votes of all the Republican Senators, six from the DFL, and both independents.

Some of the reactions were utterly predictable, this being a good example:

But this leaves out some pretty crucial information.

Cutting income tax rates doesn’t directly benefit people who don’t pay income tax

Obviously, cutting income tax rates won’t directly benefit people who don’t pay income tax.

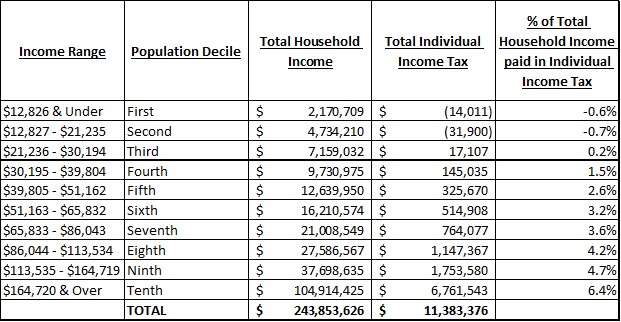

As the Department of Revenue’s most recent Tax Incidence Study shows, taken together, the bottom 20 percent of Minnesota households by income paid no income tax in 2018. Indeed, as Table 1 shows, once tax credits are factored in, those households are net beneficiaries from the state income tax system.

Table 1: Household Income and state Individual Income Tax by population decile, 2018, $ thousands

The lowest-earning households in Minnesota are already paying no state income tax. It isn’t possible to cut their state income taxes any further.

Cutting income tax rates directly benefits people who do pay income tax

If that tells you who doesn’t directly benefit from a cut in income tax rates, then who does? Well, just as obviously, it is those people who do pay income tax.

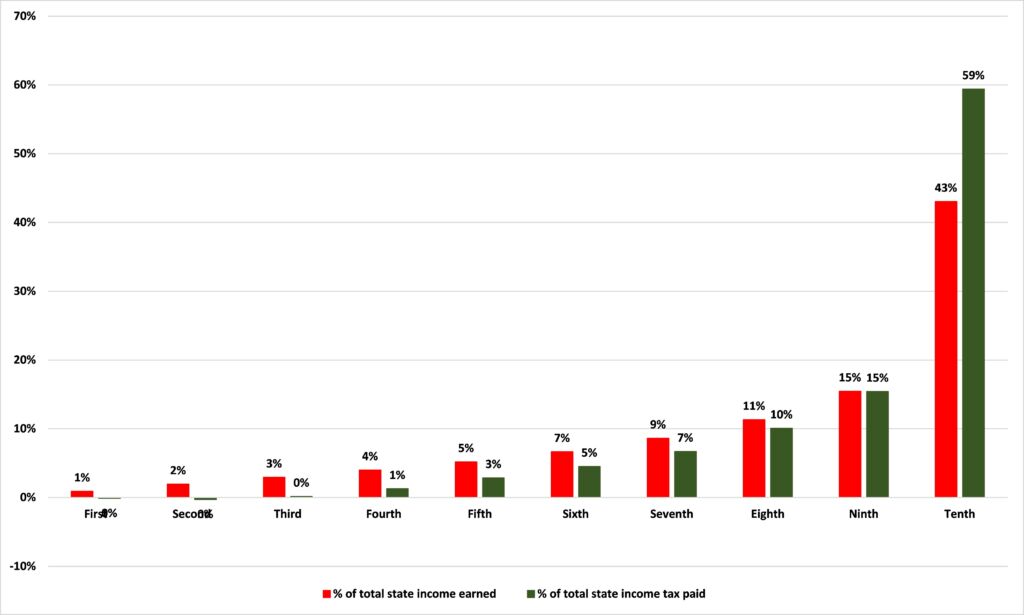

In Minnesota that is disproportionately ‘the rich.’ As Figure 1 shows (again from the most recent Tax Incidence Study) in 2018, every income decile of Minnesota households up to the eighth — that’s the bottom 80 percent of households by income — earned a share of total state Household Income larger than the share it contributed to total state Individual Income Tax receipts. The ninth decile broke even, but the highest-earning 10 percent of Minnesota households earned 43 percent of the state’s total Household Income, but contributed 59 percent of its total Individual Income Tax revenues (these numbers have held pretty steady over time).

Figure 1: Percentage of total income earned in Minnesota and total income tax paid by population decile, 2018

In short, ‘the rich’ in Minnesota pay an amount of state income tax that is disproportionate both to their numbers and their incomes.

This bill cuts effective income tax rates more for people on lower incomes than those on higher incomes

This is the result of having a progressive tax system. Minnesota’s tax system is one of the most progressive in the country and has been for decades. But if you create a situation where A) the lowest-earning 20 percent of households pay no income tax and B) the highest-earning 10 percent pay 59 percent of the income tax, you have created a situation where it becomes very hard to cut income tax rates without the benefits flowing disproportionately to ‘the rich.’

But only in dollar terms. By focusing the tax cut on the lowest bracket, as the Senate bill does, it applies to a larger share of income for individuals at the bottom of the income scale than those at the top; as a result, effective tax rates (income tax payments/income) fall by more for individuals at the bottom of the income scale than the top.

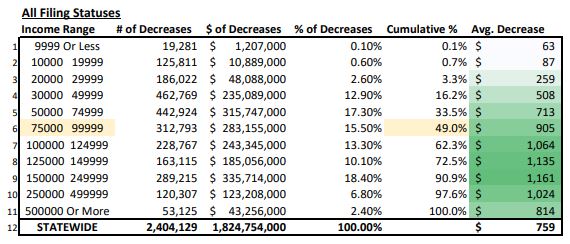

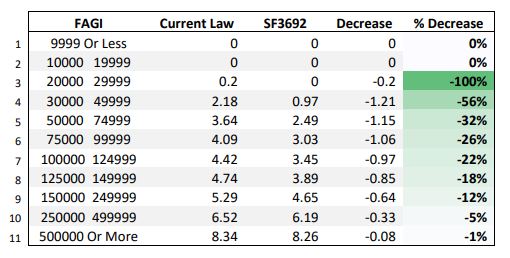

That is how you can have a table such as Table 2, where the average decrease in the income tax burden in dollar terms is greatest for individuals in the $150,000 to $249,999 income range, alongside Table 3, where the effective tax rate falls most for individuals in the $20,000 to $29,999 income range and where that fall decreases as the individual’s income increases.

Table 2: Distributional effects of a bracket rate reduction to 2.8 percent, FY 2022

Source: Minnesota Senate Counsel, Research and Fiscal Analysis

Table 3: Effective tax rate by income level

Source: Minnesota Senate Counsel, Research and Fiscal Analysis

So, while the income tax burden of an individual in the $150,000 to $249,999 income range would fall by $1,161, that is only a 12 percent reduction in their effective income tax burden. The burden falls by 100 percent for households in the $20,000 to $29,000 range, eliminating it completely, and by 56 percent for those in the $30,000 to $49,000 range.

This bill’s reductions in effective tax rates are heavily skewed towards those further down the income scale. It is not a ‘tax cut for the rich.’ That probably won’t stop people from saying that it is, but the facts say otherwise.