Cut Minnesota’s corporate income tax to boost fading entrepreneurship

At a rountable last Friday, Minnesota’s Department of Employment and Economic Development (DEED) announced its aim of marketing the state as the premier hub to launch a new business.

“We know that people that start businesses in this state are going to have a better chance than any other state in the country, making sure those businesses are around in five years and thriving. But we need more people to start those businesses and take that risk,” said DEED Commissioner Steve Grove. To help towards that end, DEED reports that $2.8 million in grants have been awarded.

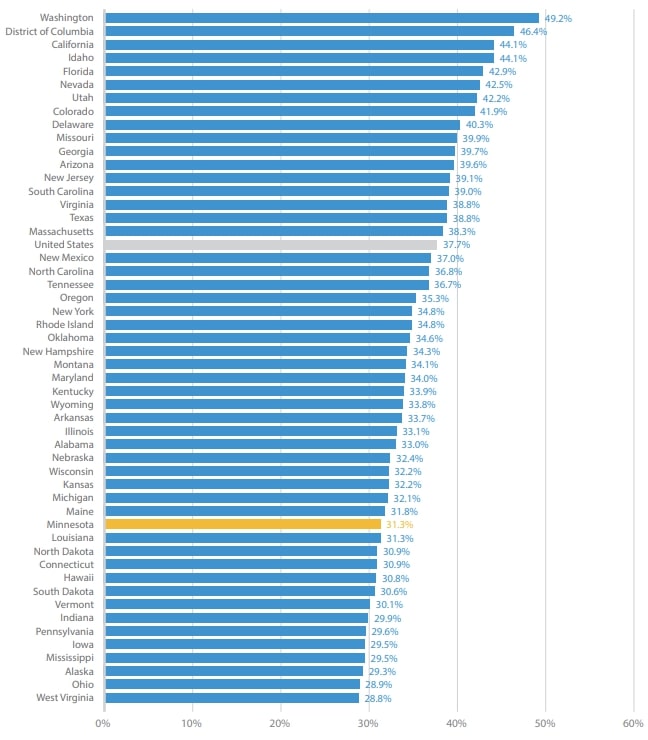

Action to improve Minnesota’s environment for start ups and small businesses is much needed. As we write in our new report, ‘The State of Minnesota’s Economy: 2020,’ New and Young Businesses accounted for 31.3% of all businesses in Minnesota in 2020. For the United States generally, the figure was 37.7% and our state’s number ranked us 38th among the fifty states and District of Columbia, as Figure 1 shows.

Figure 1: New and Young Businesses as a share of all businesses, 2020

Source: Bureau of Labor Statistics

Fortunately, there are policy tools available to the state government to boost entrepreneurship besides throwing taxpayer’s money around, but the state government seems reluctant to make use of them.

In a paper looking at the effect of corporate taxes on investment and entrepreneurship, economists Simeon Djankov, Tim Ganser, Caralee McLiesh, Rita Ramalho, and Andrei Shleifer found that:

“…the effective corporate tax rate [has] a large adverse impact on aggregate investment, FDI, and entrepreneurial activity.”

In a paper looking at tax structure and entrepreneurship, economists Mina Baliamoune-Lutz and Pierre Garello found:

“…that tax progressivity at higher-than-average incomes has a robust negative effect on nascent entrepreneurship.”

And in a paper investigating how corporate taxation affects firm’s incorporation decisions, economists MarcoDa Rin, MarinaDi Giacomo, and AlessandroSembenelli found:

“…a significant negative effect of corporate income taxation on entry rates.”

In the light of this research, Minnesota’s poor performance in new business formation isn’t too surprising. Our state imposes a flat rate of corporate income tax of 9.80%: it applies to the the first and last dollar of taxable income. So, while New Jersey has a higher top rate than Minnesota – 11.25% – that only applies to income over $1 million: the first dollar of taxable corporate income in the Garden State is taxed at the lower rate of 6.5%. Indeed, Minnesota’s starting rate of corporate income taxation ranks second highest in the United States.

Sadly, current proposals will only exacerbate this self-inflicted handicap. Gov. Walz proposes to increase the corporate income tax still further, to 10.8%, which would give us the highest starting rate in the United States. Commissioner Grove’s boss is trying to make his job even harder.

John Phelan is an economist at the Center of the American Experiment.