How does Minnesota tax its residents?

Yesterday I noted that in Minnesota the state government accounts for a much larger share of the total tax burden faced by citizens than in all but two other states. But how does our state government raise that revenue? How does that compare to other states? And how has that changed over time?

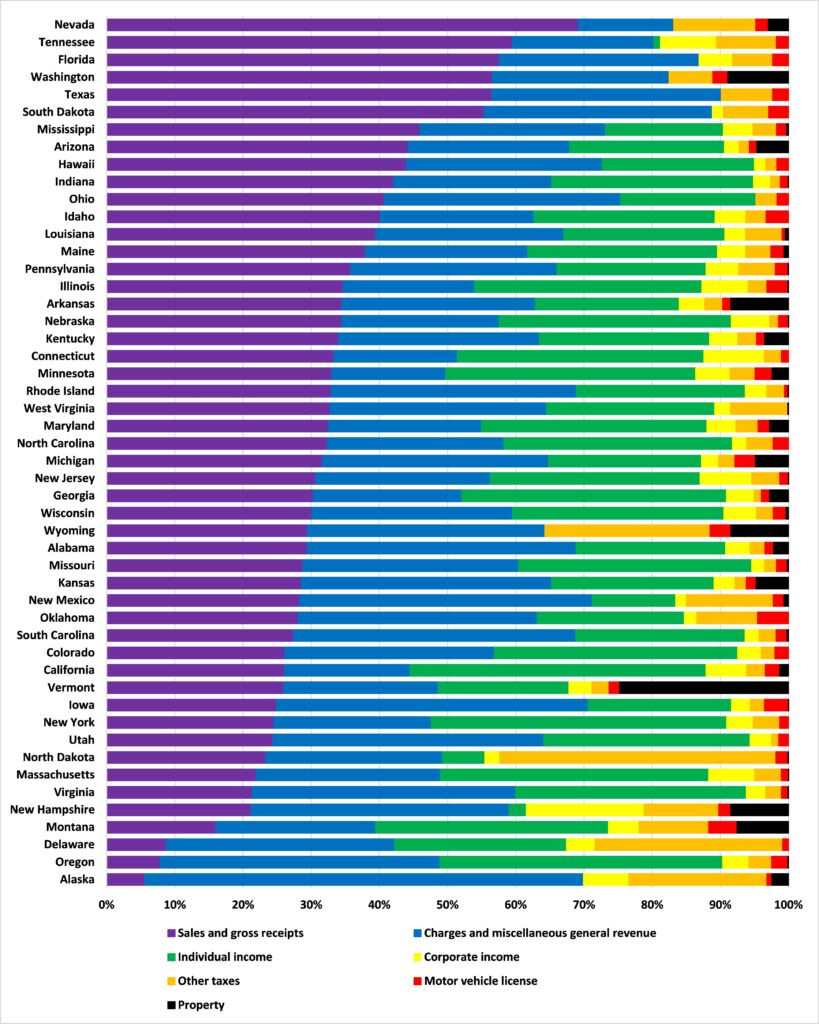

Figure 1 uses Census Bureau data to break down how much of each state’s ‘General revenue from own sources’ (General revenue) came from each of Property, Sales and gross receipts, Individual income, Corporate income, Motor vehicle license, and Other taxes as well as Charges and miscellaneous general revenue in 2019.*

Figure 1: State government revenues by source, 2019

We see that, on average, states primarily rely on Sales and gross receipts tax revenues: the median share of General revenue they account for is 32.0%. Minnesota tracks this pretty closely, with 33.0% of General revenue coming from these taxes.

Charges and miscellaneous general revenue is, on average, the next largest source of state government General revenues, accounting for a median share of 29.0%. Here Minnesota diverges quite significantly, deriving just 16.7% of General revenues from this source, ranking it 49th among the states.

The Individual income tax is, on average, the next largest source of state government General revenues, accounting for a median share of 24.7%. Here again Minnesota diverges significantly, but in the other direction: in this case the share of revenue derived from these taxes is 36.7%, the 6th highest among the states.

The other taxes are nowhere near as important for state government revenues. The Corporate income, Other, Motor vehicle license, and Property taxes account, on average, for just 3.5%, 3.3%, 1.7, and 0.1% of state revenues respectively. Minnesota is no great outlier in any of these categories; although it ranks 9th for revenue derived from Motor vehicle license taxes, the share of revenue its state government derives from this source is only 0.8 percentage points above the median.

How has this changed over time?

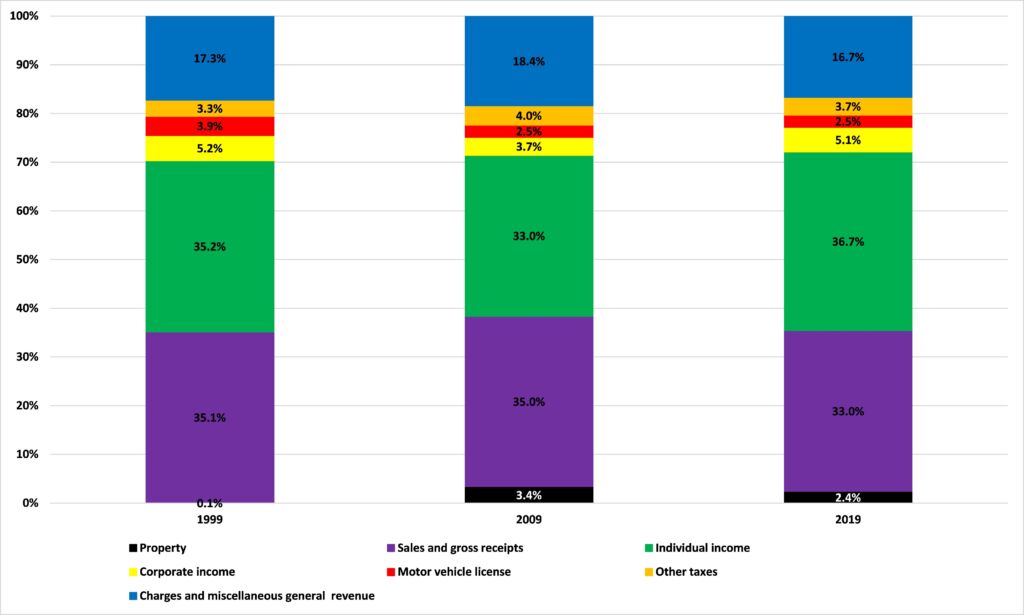

Figure 2 shows how the Minnesota state government’s sources of General revenue have changed over time. As we can see, the reliance on Individual income tax receipts is nothing new. Indeed, the only notable change over the last two decades has been an increase in the share derived from Property taxes.

Figure 2: Minnesota state government revenues by source

Source: Census Bureau and Center of the American Experiment

Over the last two days we have discovered three things about Minnesota’s state finances: One, the state government imposes a much heavier burden of taxation on its residents than is the case in most other states. Two, a much larger share of that revenue comes from state income taxes than is the case in other states. Three, this is nothing new.

It follows from this that if you believe that taxes should be cut in Minnesota – as we do – you need to reduce income taxes. It also follows that you will have to explain how you will pay for it, especially given its importance in funding the state government. We will look at that next week.

*The COVID-19 pandemic makes numbers for 2020 somewhat unrepresentative