A plan for all Minnesotans

Reinsurance keeps Minnesota’s individual health premiums among the lowest in the country and keeps 82,000 more Minnesotans enrolled.

On November 1, the annual open enrollment period to buy individual health insurance for 2023 begins and Minnesotans will once again shop from among the lowest premiums in the country. These lower premiums are in large measure due to a reinsurance program Republican state legislators passed in 2017 in response to the dramatic premium spikes that followed from the full launch of the Affordable Care Act (ACA) in 2014.

Minnesota market descends into a death spiral

The main programs and regulations of the ACA — also known as Obamacare — which passed in 2010, did not begin until 2014. At that time, premiums were kept relatively low in Minnesota and, in fact, ended up being the lowest in the country in that first year.

At the time, however, American Experiment exposed how former Gov. Mark Dayton’s staff at the Department of Commerce pressured health insurers to keep premiums artificially low leading into the 2014 election year. Commerce “asked” insurers to change the actuarial assumptions underlying their premium rates. Most complied, which led to lower premiums. Most dramatically, PreferredOne lowered premiums by 37 percent from its initial rate filing.

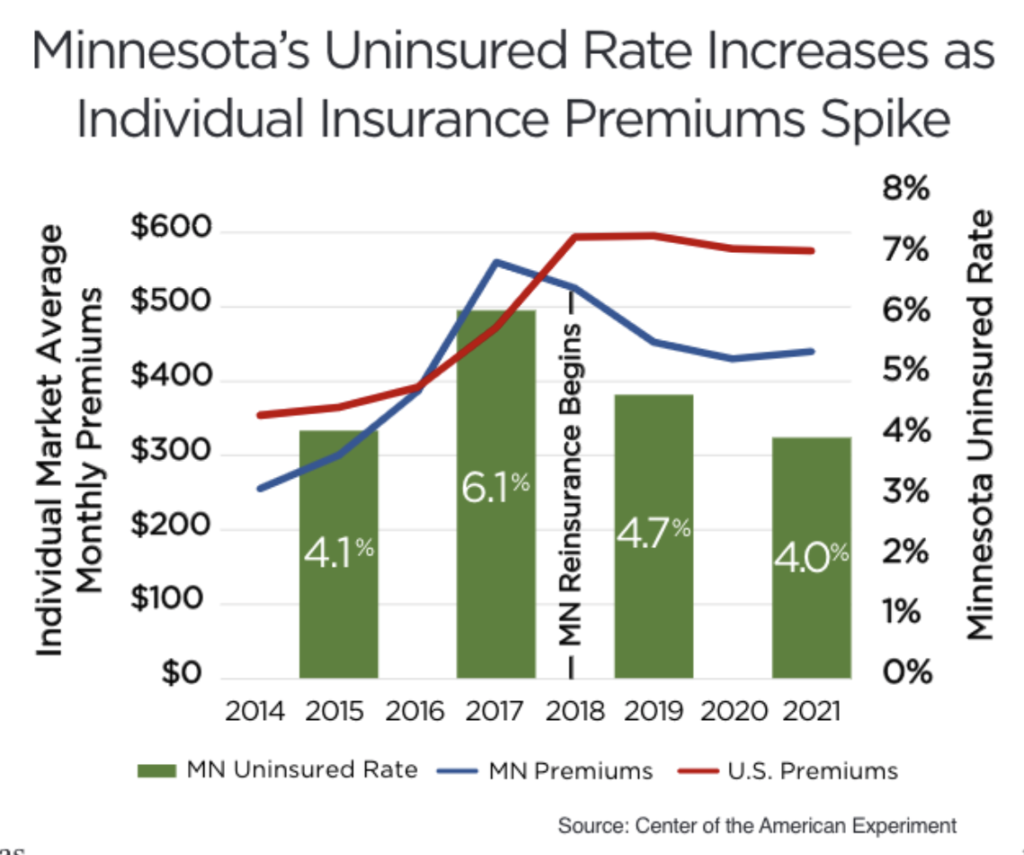

Artificially low premiums inevitably led to premium spikes in later years after insurers began losing millions upon millions of dollars. From 2014 to 2017, average monthly premiums across the individual health insurance market increased from $256 to $560. This 119 percent increase was the largest in the nation and, as the figure shows, pushed premiums well above the national average.

During these premium spikes, PreferredOne and Blue Cross and Blue Shield of Minnesota abandoned the individual market. Furthermore, unsubsidized enrollees who earned too much to qualify for ACA premium subsidies also fled the market, causing it even more damage. Unsubsidized enrollment plummeted from 250,000 enrollees in 2015 to 92,000 in 2017.

Declining enrollment plunged the market into what’s called a death spiral. Healthier people left the market which left a sicker, more expensive pool of people behind. This required insurers to raise rates even more. These cycles of higher premiums pushing healthier people out was killing the market.

While federal taxpayers protected the subsidized portion of the market from this death spiral, rising premiums became out of reach for middle- and higher-income Minnesotans with incomes too high to qualify for subsidies. In 2017, these Minnesotans landed squarely in an affordability crisis. Minnesota went from a number one ranking in the country on premium affordability to 37th in just three years. As a result, many Minnesotans had nowhere to turn for health coverage and, as the accompanying figure shows, the state’s uninsured rate jumped from 4.1 percent in 2015 to 6.1 percent in 2017 as premiums spiked.

Republican state legislators deliver a solution

The people losing coverage were not Republicans or Democrats — they were Minnesotans. Yet somehow helping this group became a partisan issue.

At the time, Republicans held control of the Minnesota House and Senate. Knowing they had to address this crisis, they passed legislation to establish the Minnesota Premium Security Plan. This established a reinsurance program that funds a portion of high-cost claims in the individual market. Funding these claims reduces claims costs for the entire market and, as a result, lowers premiums for everyone in the market.

The program operates as a partnership with the federal government under a State Innovation Waiver. By reducing premiums, reinsurance also reduces the amount of federal tax credits coming to the state. The federal government pays a large portion of the reinsurance payment as “pass-through” funding to replace the value of the premium tax credits that would have otherwise gone to state residents.

Reinsurance passed largely on party lines. Dayton refused to sign the bill but still allowed it to become law.

This partisanship is in stark contrast to every other state that established similar reinsurance programs, such as in Oregon, where Republican Sen. Jackie Winters carried the reinsurance bill that was signed by Democratic Gov. Kate Brown. Since then, 12 more states passed reinsurance programs with bipartisan support.

Federal evaluation shows reinsurance saved the market

Minnesota’s reinsurance program led to an immediate premium reduction in 2018. The Centers for Medicare & Medicaid Services (CMS) reported that reinsurance lowered premiums by nearly 17 percent in that year, which rose to over 21 percent in 2021. This dropped the state’s average monthly premiums to the lowest in the country in 2019. While Minnesota gave up this top spot in 2021, premiums are still among the lowest in the country.

Lower premiums are a good indicator of success, but certainly not the only consideration. Maybe the more important question is how reinsurance impacted enrollment.

CMS commissioned the RAND corporation to evaluate Minnesota’s reinsurance program and, in particular, to quantify its impact on enrollment.

RAND estimates over 82,000 more people enrolled in unsubsidized coverage in 2020 than would have enrolled without the reinsurance program. They emphasize how this enrollment impact is a “large effect” considering the entire unsubsidized market the year before the waiver was just over 90,000.

This enrollment impact shows how reinsurance stopped the death spiral and saved Minnesota’s individual health insurance market for the unsubsidized. Without reinsurance, enrollment would have plummeted to under 20,000 according to the RAND estimates, which would have been an unsalvageable drop.

Reinsurance authorized for another five years

The reinsurance program was set to expire this year. Though there was inevitable partisan bickering over whether to keep the program going, the Senate and the House eventually passed legislation to extend it for another five years on a bipartisan basis. Every once in a while, even partisans can’t argue with results.

While saving the individual market from the throes of a death spiral is a good news story, the state’s relatively affordable premiums remain expensive. Last year individual market premiums were still 83 percent higher than in 2013, the year before the ACA took full effect.

Reinsurance is just one tool to help address the high cost of health care. America’s health care system suffers from a lack of competitive pressure on health plans, drug manufacturers, hospitals, and other providers to keep costs low. That’s why American Experiment develops and advances policies to promote competition across the entire health care system.