Understanding incentives

Fiscal policymakers have accepted for centuries that taxes act as a negative incentive on whatever is being taxed. That doesn’t always keep them from taxing.

“Incentives do make a difference.” So said Minnesota Governor Mark Dayton, recently. They do, and much public policy depends on that. Governments tax things like cigarettes and alcohol because they want people to smoke and drink less. If they want people to do more of something, like building solar power plants, they subsidize it (taxation in reverse). Indeed, the governor is currently protesting a freeze on cigarette tax rates because he thinks higher rates will discourage smoking.

The study of incentives and people’s reactions to them is a key part of modern economics. As catalogued in the bestselling book Freakonomics, people respond to incentives whether they are schoolteachers, realtors, crack dealers, sumo wrestlers, or bagel sellers.

There is nothing new in the economics of this or its application to public policy. In 1698, Tsar Peter the Great wanted to bring Russia into line with western European mores, which he deemed more progressive. This included facial hair. Beards were in style in Russia, while the British and French preferred to be clean shaven. So, Peter introduced a tax on beards to incentivize people to shave. The tax levied depended upon the status of the bearded man. Those associated with the Imperial Court, military, or government were charged 60 rubles annually. Wealthy merchants were charged 100 rubles annually, while other merchants and townsfolk were charged 60 rubles. Muscovites were charged 30 rubles annually. Even peasants were charged two half-kopeks every time they entered a city. To enforce the tax, the police were authorized to forcibly and publicly shave those who didn’t pay.

In 1696, to fund its wars with Louis XIV, the British Parliament passed the Window Tax. As a proxy for wealth, the tax was levied based on the number of a property’s windows. Besides a flat-rate house tax of 2 shillings per house (equivalent to $19.25 in 2015), there was a variable tax for the number of windows above ten. Properties with between ten and twenty windows paid an extra four shillings (equivalent to $38.52 in 2015), and those above twenty windows paid an extra eight shillings (equivalent to $77.04 in 2015). As a result, windows were bricked up in properties around Britain. Look up when walking past a Georgian house in London today and you can still see the effects of Window Tax avoidance in brick and mortar. “Incentives do make a difference.”

Changing incentives, changing behavior

The effect of a tax on behavior will vary depending on the rate of the tax. It will change as these rates change.

A small tax on tobacco will have little effect on your consumption. But as the tax rises you will alter your consumption accordingly. You may cut back (which is what policymakers want). You might bring your purchases forward to avoid the tax. You might buy illegally. You may buy from a jurisdiction with lower tax rates.

As MPR reported recently, with lower cigar prices online and in neighboring states, tobacco retailers in Minnesota are excited about the upcoming tax cut. One vendor, Chuck Peterson of Maplewood Tobacco and E-Cig Center, told MPR that “People wouldn’t be more inclined to go to, say, Wisconsin or North Dakota or another state to buy their cigars… They can just come up the street here, a five or 10-minute drive, and get a nice stick for a fair price.”

With a high tax rate on tobacco, Minnesotans buy their smokes out of state, paying tobacco tax there. Minnesota gets no tobacco tax revenue. But, by reducing the tax rate, Chuck Peterson argues, Minnesotans will be more likely to buy their smokes in-state and pay tobacco tax here.

By reducing the disincentive effect, a cut in the rate of tax might lead to an increase in the revenue it generates.

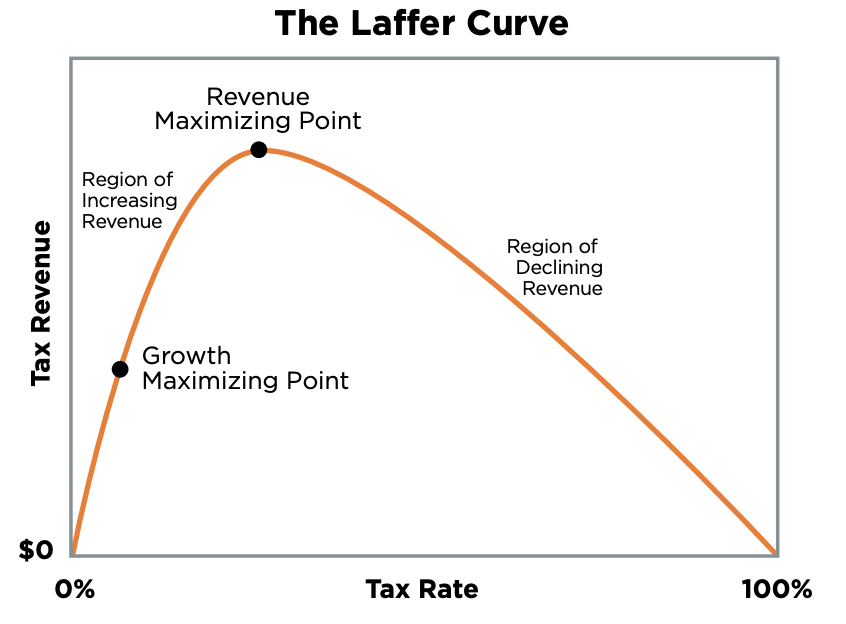

Tobacco taxes and the Laffer Curve

This insight was modeled as the Laffer Curve (see graph), named after the economist Arthur Laffer.

You can see Chuck Peterson’s point illustrated. Minnesota’s tobacco tax rates were to the right of the Revenue Maximizing Point. By lowering rates and reducing the disincentive effect, Minnesota’s state government might encourage those smokers buying illegally or out of state, where they pay no tobacco tax, to buy their smokes legally in Minnesota and pay tax here. This would increase the tax revenue while reducing the tax rate.

Income taxes and the Laffer Curve

So it is widely accepted among fiscal policymakers, and has been for centuries, that taxes act as a negative incentive on whatever it is that is being taxed. Policymakers have used this insight to pursue given policy ends and they continue to do so. Yet, in other situations, they discard this logic and assume that there is no negative incentive attached to taxation. They suddenly claim that they can raise tax rates with no adverse effect on the thing being taxed.

The most notable example is income tax. If rates are to the right of the Revenue Maximizing Point of the Laffer Curve, reducing those rates should increase revenues.

This happened in the U.S. in the 1920s. During the First World War, the Wilson administration raised tax rates to fund military spending. As the economist Thomas Sowell explains in his book “Trickle Down” Theory and “Tax Cuts For the Rich,” the number of people reporting taxable incomes of more than $300,000 fell from well over a thousand in 1916 to less than three hundred in 1921. The total amount of taxable income earned by people making over $300,000 declined by more than four fifths. The number of people reporting incomes of over $1 million fell from 206 in 1916 to just 21 in 1921.

And this was during a period of rising prosperity. It was not that their incomes collapsed but that they were incentivized to put their money into tax-exempt securities that did not have to be reported under the laws of the time.

The Treasury Department estimated that the money invested in tax-exempt securities had nearly tripled in a decade. The total estimated value of these securities was almost three times the size of the federal government’s annual budget, and more than half the size of the national debt. Treasury Secretary Andrew Mellon noticed that the amount of tax top earners paid had fallen as their tax rates had risen. He drew a causal link from one to the other. As he put it, “Just as labor cannot be forced to work against its will, so it can be taken for granted that capital will not work unless the return is worthwhile. It will continue to retire into the shelter of tax-exempt bonds, which offer both security and immunity from the tax collector.” He claimed that “the man of large income has tended more and more to invest his capital in such a way that the tax collector cannot reach it.” The value of tax-exempt securities, he said, “will be greatest in the case of the wealthiest taxpayer” and “relatively worthless” to a small investor. As a result, the cost of making up such tax revenue losses must fall on other, non-wealthy taxpayers “who do not or cannot take refuge in tax-exempt securities.” Mellon called this an “almost grotesque” result with “higher taxes on all the rest in order to make up the resulting deficiency in the revenues.” Mellon attempted to persuade Congress to end tax exemptions for municipal bonds and other securities. Congress refused. They continued what Mellon called the “gesture of taxing the rich,” while in fact, he claimed, high tax rates were “producing less and less revenue each year and at the same time discouraging industry and threatening the country’s future prosperity.”

His solution was to reduce the incentives for investors to divert their money from productive investments in the economy to putting it into safe havens in these tax shelters. So, Mellon cut the top rate of income tax.

He was proved right. In 1921, the tax rate on people making over $100,000 a year was 73% and the federal government collected just over $700 million in income taxes, 30 percent of which was paid by those making over $100,000. By 1929, after a series of tax rate reductions, the rate was down to 24% on those making over $100,000 and the federal government collected more than a billion dollars in income taxes, with 65 percent coming from those making over $100,000. The number of individuals reporting taxable incomes of over $1 million dollars rose to 207 by 1925. Even so, Mellon’s policies were denounced as “a device to relieve multimillionaires at the expense of other tax payers,” and “a master effort of the special privilege mind,” to “tax the poor and relieve the rich.”

The same thing happened again in the 1980s. In the U.S. in 1980, the top income tax rate went up to 70 percent and the share of income taxes paid by the top 1 percent of taxpayers was 19.3 percent. The following year Ronald Reagan’s tax cut reduced the top rate to 50 percent. By 1986, the top 1 percent of earners were paying 25.7 percent of all federal income taxes. That year saw the top statutory tax rate cut further, to 28 percent. By 1992, the top 1 percent of earners were paying 27.5 percent of all federal income taxes.

In the U.K. in 1979, the top rate of income tax was 83 percent and the top 1 percent of earners paid 11 percent of income tax revenues. Margaret Thatcher cut this rate to 60 percent and, by 1987, the share of income taxes paid by the top 1 percent of earners had risen to 14 percent. That year the top rate was lowered again, to 40 percent, and the share of income taxes paid by the top 1 percent was up to 21 percent by 2005. It happened again in Britain after the last Labour government left office in 2010. The coalition reduced Corporation Tax rates and the top rate of income tax and saw revenues from both rise subsequently.

‘Progressives’ learn to love the Laffer Curve

Despite embracing the logic of incentives for things such as cigarettes and alcohol, so-called “progressives,” for a long time, cried “snake oil” when the same logic was applied to incomes.

That is increasingly not the case. Nowadays, some on the political left seem not only to accept the logic of incentives, as applied to incomes by Laffer, but to embrace it. Indeed, the fact that high tax rates might reduce economic activity, as Laffer predicted, is now seen by some as an argument in their favor.

In his much bought, seldom read book Capital in the Twenty-First Century, economist Thomas Piketty explicitly acknowledges that high tax rates do not translate into high tax revenues. “A rate of 80 percent applied to incomes above $500,000 or $1 million a year would not bring government much in the way of revenue, because it would quickly fulfill its objective: to drastically reduce remuneration at this level,” he writes. “[T]hese high brackets never yield much,” he continues, the point is “to put an end to such incomes and large estates.”

This is an explicit embrace by Piketty of Laffer’s logic. He acknowledges that there is a downward slope; that the curve, in fact, curves. Piketty and Laffer agree that higher tax rates depress taxable activity. But Piketty is equally explicit about such disincentives being the whole point of introducing such high rates of taxation. Indeed, the only real difference between Laffer and Piketty is that Laffer sees the suppression of taxable activity as a negative outcome while Piketty views it as a positive.

Why do we tax?

There are several reasons given for taxation. One is to redistribute income and wealth. Another is to pay for things such as public goods or public services. The idea here was generally to maximize revenues. A third is to discourage certain activities through the disincentive effects of taxation. By contrast, success here would show itself in low revenues.

All three of these rationales have a long history, as we’ve seen. But the explicit application by the left of (dis)incentive theory to reduce economic activity is something newer. This is a penal approach to taxation which contrasts with an approach designed to maximize revenues. Louis XIV’s finance minister, Jean Baptiste-Colbert, is supposed to have said that “The art of taxation consists in so plucking the goose as to procure the largest quantity of feathers with the least possible amount of hissing.” Not so for penal taxers such as Piketty. The art is now to procure the largest quantity of hissing regardless of how many feathers you get.

But these left-wing economists ought to be careful what they wish for. They may be wedded to eliminating the rich. But they are also wedded to big government spending. And this can only be financed by tax revenues generated by the rich. Remember the wise words of Governor Dayton: “Incentives do make a difference.”