Minnesota ranks 44th out of 50 on State Business Tax Climate Index

These were some of the headlines in local media in July, when CNBC released its annual “America’s Top States for Business” ranking:

- Minnesota ranks No. 5 among ‘America’s Top States for Business’ by CNBC — Minneapolis/St. Paul Business Journal

- Minnesota knocks Texas out of Top 5 in CNBC’s ‘Top States for Business’ ranking — Bring Me the News

- Minnesota ranked as a top state for businesses, surpasses Texas — WCCO

- CNBC Ranks Minnesota 5th Best State for Business — KNSI

- Minnesota ranked as a top state for businesses — KTTC

- Minnesota named a Top 5 state for business — Southern Minnesota News

On closer investigation it turned out that these rankings were a complete waste of time. Nevertheless, they received wide coverage and were eagerly touted by an administration desperately looking for something positive to point to, however fictitious it may be.

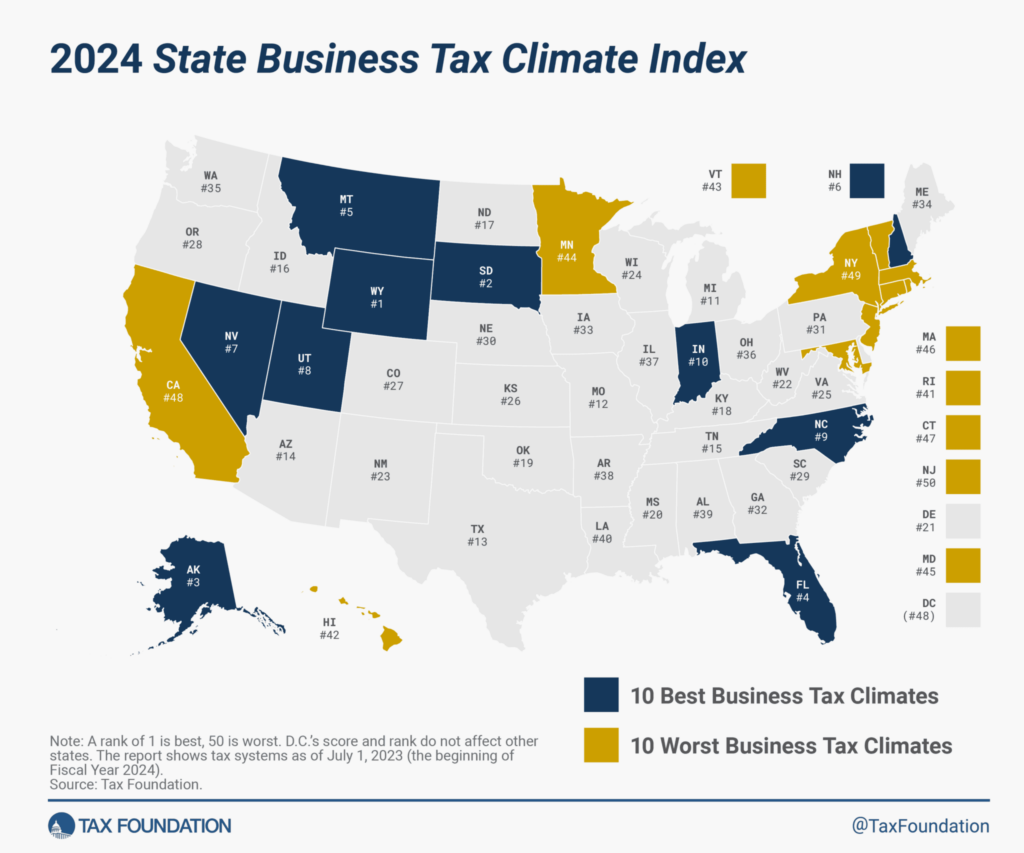

You’d never know it from the local media’s uncharacteristic, monastic silence, but yesterday saw the release of another ranking of the states. The Tax Foundation’s State Business Tax Climate Index for 2024 ranked Minnesota a lowly 44th out of 50 states, with particularly low rankings for our individual (42nd) and corporate (47th) taxes.

Because of measures passed in the last legislative session, Minnesota actually makes the list for “Notable Ranking Changes”:

Minnesota ranks in the bottom half of states on each component of the Index. The state’s corporate income tax score is, in part, weighed down by the new election to add Global Intangible Low-Taxed Income (GILTI) to the corporate tax base. Generally, states should avoid taxing GILTI, as state taxation should stop at the water’s edge, and taxing GILTI makes it more expensive for corporations to operate in a state for reasons having nothing to do with their activities in that state. Now, Minnesota ranks 47th on the corporate tax component, a loss of four positions compared to last year, and 44th overall.

Minnesota has, then, made itself even less business friendly, which might explain why – contra CNBC – business don’t seem overly keen on the place.

Three of our neighbors, by contrast, also made the list but for good reasons:

Iowa

Iowa witnessed significant changes in its tax landscape this year. Notably, the state reduced its top marginal individual income tax rate from 8.53 to 6.0 percent and simplified its rate schedule by consolidating nine brackets into four. The state is on its way to further reduce individual income tax rates and transition to a flat rate of 3.9 percent by 2026. Additionally, Iowa eliminated the marriage penalty in its individual income tax brackets by doubling the bracket widths for married couples filing jointly. On the corporate side, Iowa’s three-bracket corporate income tax was consolidated into a two-bracket tax, with the top rate decreasing from 9.8 to 8.4 percent. Subject to revenue availability, future reforms target a flat corporate income tax rate of 5.5 percent. These reforms signify a concerted effort by Iowa lawmakers to provide tax relief to residents and enhance the overall competitiveness of the tax system. As a result, Iowa’s overall ranking improved from 38th to 33rd.

…

North Dakota

North Dakota reduced its top marginal individual income tax rate from 2.9 to 2.5 percent and established a wide zero-tax bracket. The state now has the lowest top marginal rate among those states that tax wage and salary income. As a result, North Dakota became more competitive on the individual income tax component and improved seven places, from 28th to 21st.

…

South Dakota

South Dakota, which does not have an individual or corporate income tax, enacted H.B. 1137 in March 2023, trimming its sales tax rate from 4.5 to 4.2 percent, effective July 1, 2023. This change improved South Dakota’s sales tax component ranking by seven places, from 34th to 27th, but this change was not enough to improve the state’s overall ranking, which is already 2nd in the country.

A few years ago, I wrote a report on how state government policy in Minnesota was negatively impacting the economy of the state relative to its neighbors. I might have to update that in the new year. Watch this space, because you may not see it in the local media.