Minnesota’s economic growth is lagging

In our new report, The State of Minnesota’s Economy: 2017, we take a thorough look at our state’s economic health and the prospects for the future.

Minnesota’s economic growth since 2000

The first point we make is that Minnesota’s economic growth rate has lagged that of the nation generally since 2000.

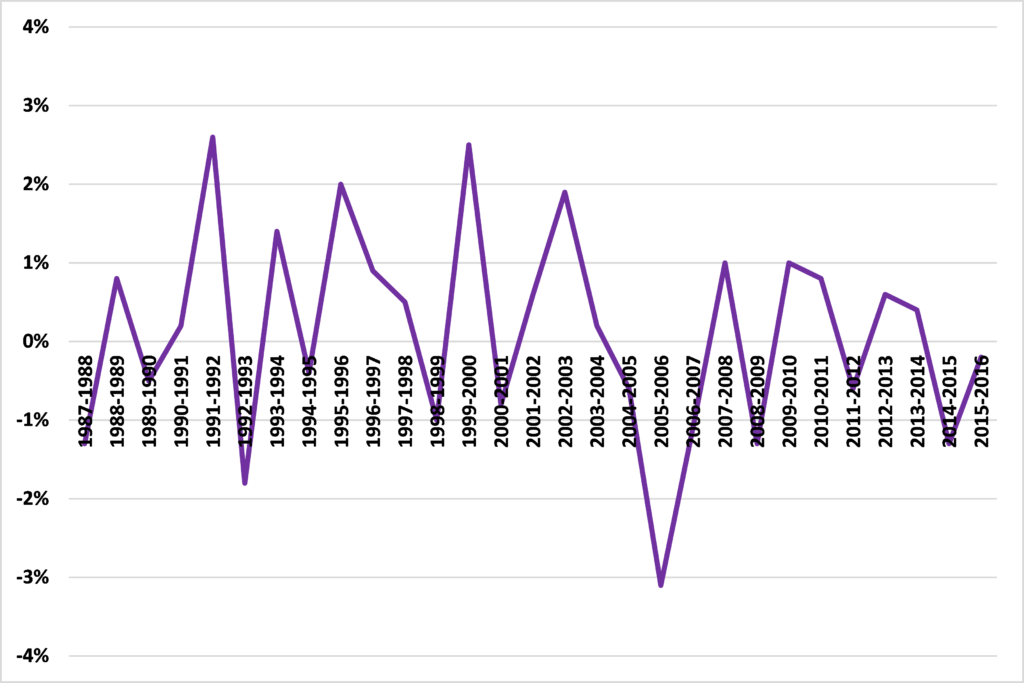

Figure 1 illustrates this. It subtracts the national GDP growth rate from that of Minnesota. So, if Minnesota’s economy grows by 4% and that of the US grows by 5.3%, that shows up as -1.3%. As Figure 1 shows, in eight of the sixteen years since 2000-2001, Minnesota’s growth rate of GDP has been lower than that of the US.

Figure 1: Minnesota’s GDP growth rate relative to the United States’ GDP growth rate, 1987-1988 to 2015-2016, %

Source: Bureau of Economic Analysis

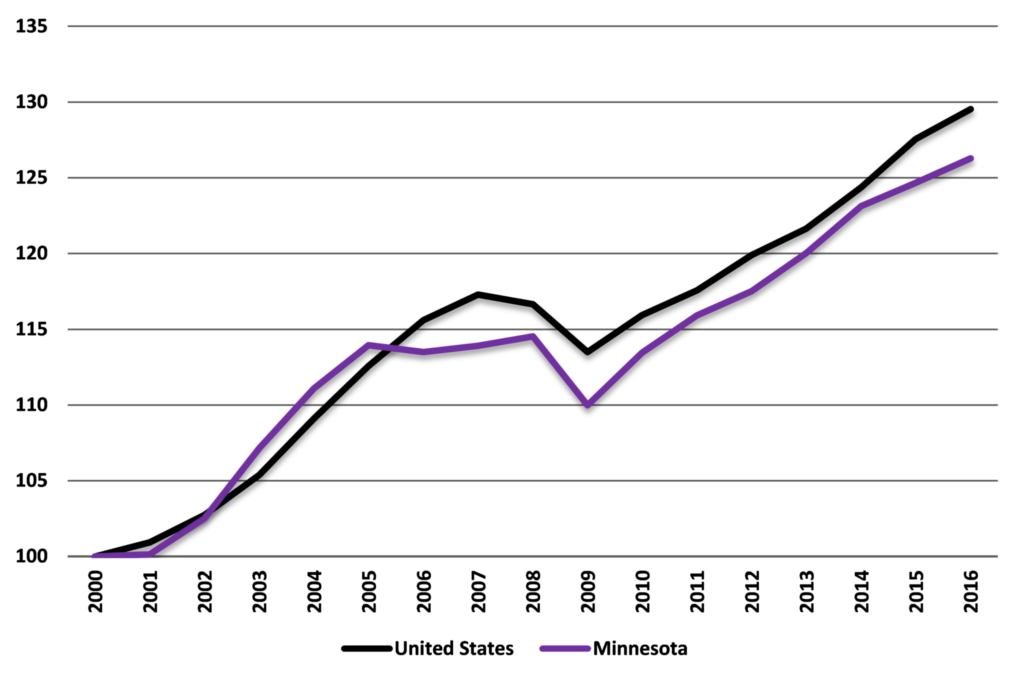

The result of this is shown in Figure 2 (which is Figure 1 in our report). This sets the GDP levels of Minnesota and the US for 2000 at 100 so we can compare growth rates. We see our state’s lag on this measure. Indeed, Minnesota’s economy is 2.5% smaller than it would have been if it had grown at the same rate as the US generally since 2000.

Figure 2: GDP growth in Minnesota and the US, 2000 to 2016 (2000=100)

Source: Bureau of Economic Analysis

Isn’t this just convergence?

But isn’t this just because Minnesota already had a high level of GDP per capita (GDP divided by the state’s population)?

This was a point made in response to our report last year. The economic theory of convergence holds that, all else being equal, poorer economies’ per capita incomes will tend to grow at faster rates than in richer economies. They will catch up, in other words. The economist Robert Barro’s 1990 paper, Economic Growth and Convergence across the United States, found evidence to support this theory. During much of the 20th century, poor states and regions in the US caught up with rich ones at a rate of about 2% per year, a figure sometimes called the “iron law of convergence”. In 1930, for example, workers in Mississippi earned just 20% of the wages of workers in New York. By 1980, the proportion had increased to 65%. In 1991, the economist Olivier Blanchard wrote that “The convergence of income across regions in the United States is a robust fact”. And, back then, it was.

Well, no

More recent research casts doubt on this.* As The Economist noted last month,

“…in the years since Mr Blanchard’s pronouncement, such convergence has slowed. A paper by Peter Ganong of the University of Chicago and Daniel Shoag of Harvard finds that incomes across states converged at a rate of 1.8% per year from 1880 to 1980. Since then, however, there has been hardly any convergence at all. A study by Elisa Giannone of Princeton finds that convergence has declined in cities too. Between 1940 and 1980, poor cities caught up with rich ones at a rate of 1.4% a year. Since then, they have lagged behind.”

Specifically, Ganong and Shoag find that “The convergence rate from 1990 to 2010 was less than half the historical norm, and in the period leading up to the Great Recession there was virtually no convergence at all”. In other words, the ‘convergence’ which is supposed to explain Minnesota’s slow rate of economic growth relative to the US average, has not been happening over the period covered in our report. Our economic growth is lagging, but ‘convergence’ doesn’t explain it.

*This is not a first for the unfortunate Mr. Blanchard. In 2008, he wrote that “a largely shared vision both of fluctuations and of methodology has emerged” among economists. No sooner was the ink dry than the economy tanked and economists were at each other throats over diagnoses and remedies.

John Phelan is an economist at Center of the American Experiment.