MN Senate votes to extend Premium Security Plan

In 2017, the Minnesota Legislature established the Minnesota Premium Security Plan (MPSP), a reinsurance program that lowered premiums in the individual health insurance market by over 20 percent. Set to expire at the end of 2022, the Minnesota Senate voted on a bipartisan basis to extend the program for another five years.

The original legislation to establish the MPSP was led by Republicans and passed largely on party lines. Gov. Dayton refused to sign the bill, but still allowed it to become law. This reflected Dayton’s acceptance that something needed to be done to help the market and, at the same time, reflected his persistent refusal to reach across party lines for solutions.

Looking forward, the extension is critical to avoiding an immediate, market-destabilizing spike in premiums that would occur if the program abruptly ends. Fortunately, unlike 2017, the Senate bill to extend the program attracted broader bipartisan support, with two Independents and five DFLers voting yes. In addition, the Walz administration has been taking the necessary steps to apply for an extension from the federal government.

MPSP operates under a state innovation waiver

The MPSP is a reinsurance program that funds a portion of high-cost claims in the individual market. Funding these claims reduces claims costs for the entire market and, as result, lowers premiums for everyone in the market. A report from the Centers for Medicare & Medicaid Services shows this program lowered premiums by nearly 17 percent in the first year of operations and premium savings grew to over 21 percent in 2021.

The program operates as a partnership with the federal government under a State Innovation Waiver. Reinsurance payments are funded by the state and federal governments. By lowering premiums, the program also reduces federal premium tax credits because the credits are linked to the price of the premium. The federal portion of the funding is provided as “pass-through” funding to replace the value of the premium tax credits that would have otherwise gone to state residents.

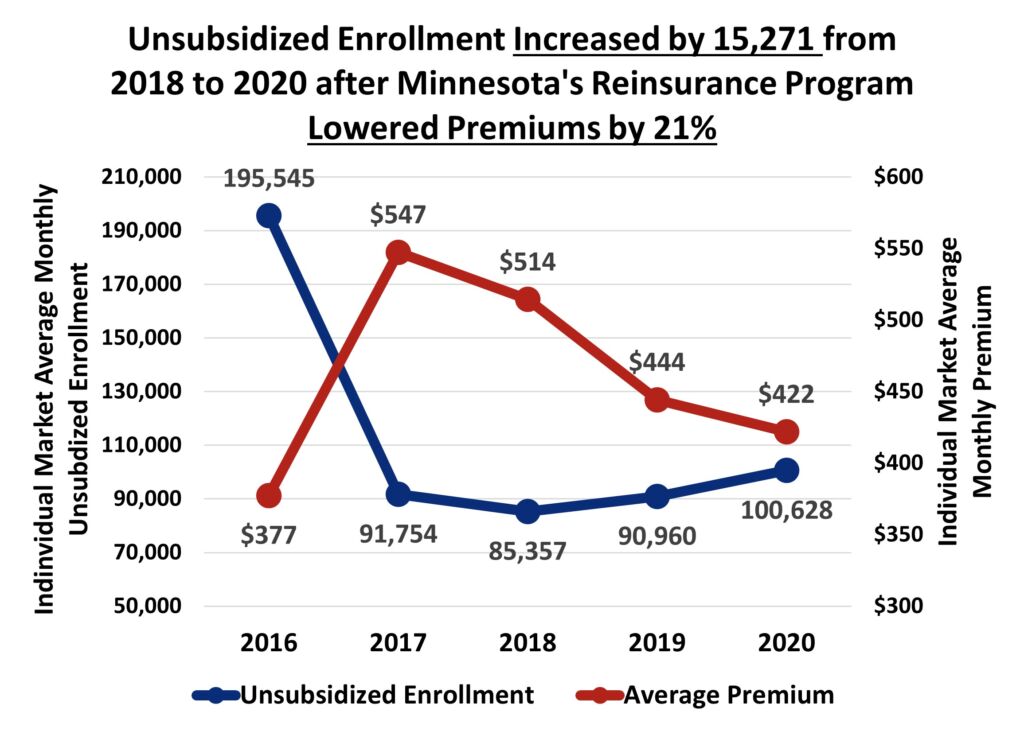

Reinsurance addressed a serious affordability problem

The following chart shows the problem the reinsurance aimed to solve back in 2017. The chart compares premium trends to enrollment trends for unsubsidized people and shows how enrollment plummeted at the same time premiums spiked. After the ACA’s main regulations went into effect in 2014, individual market health insurance premiums began to rise across the country. In Minnesota, however, health plans kept premiums artificially low in the first couple of years, which was not sustainable. Average monthly premiums then spiked from $377 in 2016 to $547 in 2017 — a 45 percent jump in just one year. At the same time, enrollment in the unsubsidized portion of the market plummeted from 195,545 to 91,754 — a 53 percent drop.

Among the more than 100,000 Minnesotans who lost individual market coverage, many of them likely went uninsured. It’s no coincidence that the Minnesota Health Access Survey shows the uninsured rate among non-elderly adults in Minnesota increased from 5.4 percent in 2015 to 8.7 percent in 2017.

Reinsurance stabilized and increased enrollment

The previous chart also shows the success reinsurance achieved. The program quickly stabilized and increased enrollment among the unsubsidized. As premiums declined due to the reinsurance program, unsubsidized enrollment increased from 85,357 in the first year of the program to 100,628 in 2020 — an 18 percent increase. At the same time, the uninsured rate for non-elderly adults also improved, dropping from 8.7 percent in 2017 to 6.4 percent in 2019.

While an 18 percent enrollment increase is great, it underrepresents the success of the reinsurance program. Without the program, unsubsidized enrollment in Minnesota would likely have continued to drop in step with enrollment losses across the country. Unsubsidized enrollment nationally continued to drop by 27 percent in 2018 and another 9 percent in 2019. By avoiding a similar drop, reinsurance kept thousands more Minnesotans covered through the individual market on top of the 15,000 who gained market coverage after the program began.

Legislation helps complete the waiver application

Last December, the Department of Commerce submitted an application to the federal government to extend the waiver, but the application was deemed incomplete. This was due, in part, to the lack of sufficient legislative authority that the ACA requires. The Senate bill provides this authority and brings the extension application a big step closer to completion.