New businesses face higher taxes in Minnesota than older businesses

According to the Tax Foundation’s State Business Tax Climate Index, Minnesota has the 46th most favorable tax system for businesses in the country. This is mainly due to high individual and corporate income tax rates. However, other issues with the tax structure also make Minnesota hostile to businesses.

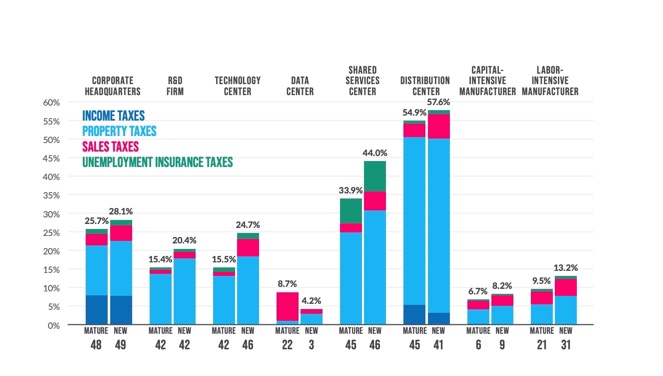

In Location Matters: The state tax costs of doing business, the Tax Foundation analyzes how Minnesota’s tax system applies to different businesses. Specifically, the report calculates effective tax rates for eight different businesses,

a corporate headquarters, a research, and development (R&D) facility, a technology center, a data center, a shared service center, a distribution center, a capital-intensive manufacturer, and a labor-intensive manufacturer

Analyzing both new and mature firms, the Tax Foundation concludes that Minnesota’s tax system applies significantly different tax rates to different businesses, creating a potentially distortive, not to mention unfair, taxation climate.

How do taxes differ among businesses?

Adding up Corporate income taxes, Gross receipts and franchise taxes, Property taxes, Unemployment Insurance Taxes, and Sales tax on business equipment or inputs, the Tax Foundation finds that the effective tax rate for new businesses ranges from 4.2 percent to 57.6 percent. However, for mature firms, the tax rates range from 6.7 percent to 54.9 percent.

This can be explained partly by the fact that

Minnesota offers few incentives, which, combined with high unemployment insurance and property taxes (and high income taxes for firms that sell in-state), yield substantially above-average tax burdens for most new operations

Indeed, seven of the eight new firms analysed face higher tax rates compared to mature firms. This is true except for data centers. New businesses in the Shared Services Center face a tax rate that is ten percentage points higher compared to mature businesses in the same industry.

Across both new and old firms, tax rates differ significantly across industries in general. Low tax rates for capital-intensive manufacturers, for instance, are due to Minnesota‘s single sales apportionment formula and the exclusion of manufacturing equipment from the sales tax.

Shared data services, on the other hand, face high tax rates due to

the state’s large taxable wage base and high maximum rate for unemployment insurance taxes.

And distribution centers face a high tax rate due to property taxes, which make up a huge majority of the overall tax burden for businesses in that industry.

Why this is concerning

Ideally, the tax code should treat all businesses equally. This creates a fair tax system and prevents distortion in business investments. Minnesota’s tax system not only places disproportionately higher taxe some industries compared to others, but it also taxes newer businesses at higher rates compared to mature businesses, discouraging entrepreneurship.