Positive GDP numbers don’t tell the full story

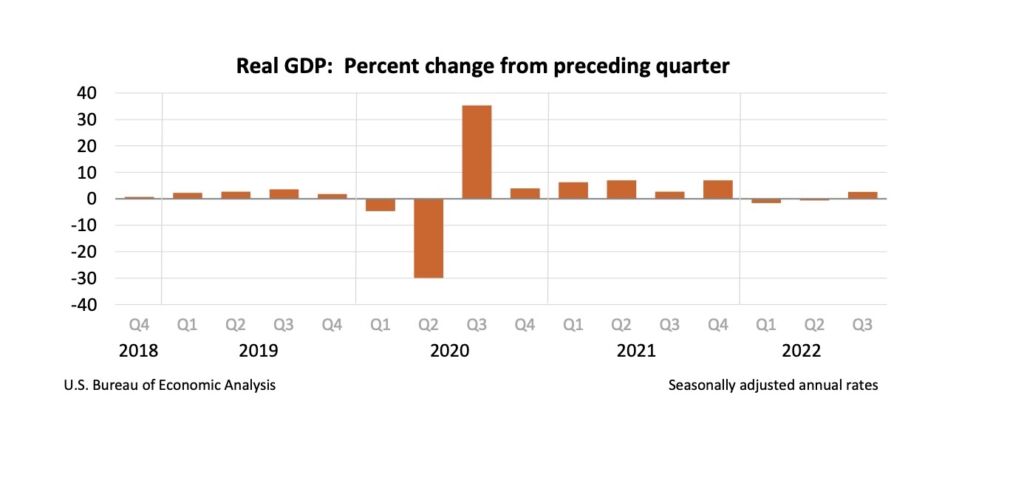

According to the Bureau of Economic Analysis (BEA), in the third quarter of this year — July to September — the economy grew at a rate of 2.6 percent compared to the second quarter. This seems like quite the rebound compared to when the economy contracted two quarters in a row prompting a discussion about a recession.

With the first two quarters of the year showing a GDP decline, positive GDP growth is certainly welcome news. But such news also poses some questions — and probably some confusion — regarding the future of the US economy.

For some, strong GDP growth might present a reason for celebration. However, much like how recessions are not solely defined by GDP decline, positive GDP also does not give us a complete picture of the economy and where it is headed. For that, we have to dig deeper.

Where the growth came from

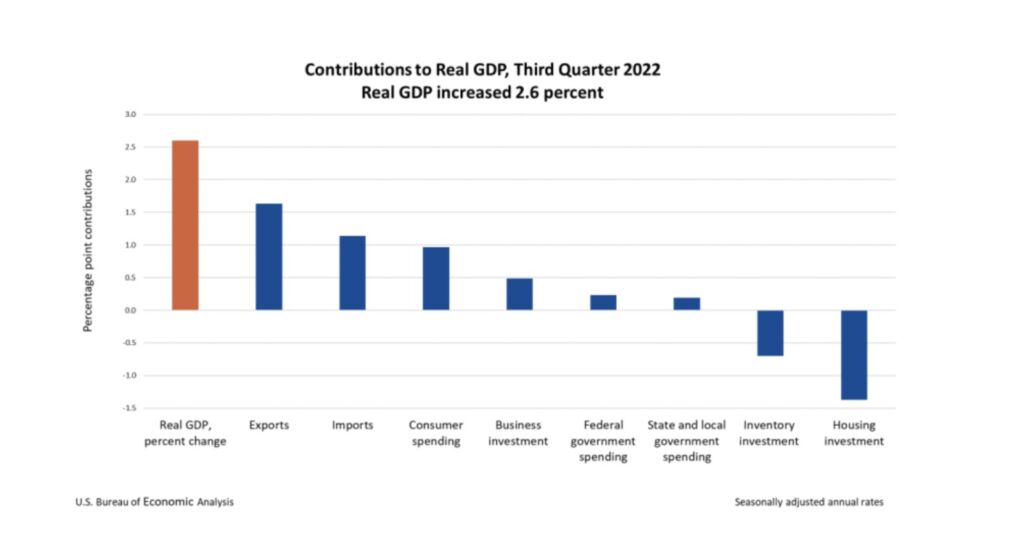

Four main things are counted in Gross Domestic Product (GDP). These are government spending (both state and local, consumer spending, net exports (exports minus imports), and gross private domestic investment — which includes business, inventory, and housing investment.

According to the data provided by the BEA, growth in GDP primarily reflected positive growth in next exports, consumer spending, government spending, and nonresidential fixed investment — a subcomponent of gross domestic investment.

Out of the four main components, net exports contributed the most to the positive trend, followed by consumer spending, then government spending. The positive contributions from these three sectors were offset by a net decrease in gross private domestic investment.

Can this growth be sustained?

Whether the two-quarters of negative GDP growth at the beginning of this year constitutes a recession probably depends on who is defining what a recession is. But there are a couple of concerning trends with the current positive GDP numbers that signal a weakening economy.

For one, consumer spending — which constitutes nearly three-quarters of all economic activity — has been decelerating in recent months. High prices are discouraging spending. And with the Fed tightening interest rates to fight inflation, it is likely that consumer spending, as well as investment spending — which is already down —, will fall or decelerate even further in months to come.

Growth in net exports, which contributed more than half the growth in GDP, is likely to be tempered by tight monetary policy and a weakening global economy. With the dollar appreciating as the Fed hikes interest rates, US exports will prove pricier, which would dampen demand for US products. But even without these factors, net exports are generally volatile and make up a small component of GDP so they cannot be relied on too heavily for long-term GDP growth.

And while the labor market remains strong, job growth has also eased up in recent months pointing to a labor market that is getting weaker.

Conclusion

Certainly, the economy is complex, so the list of possibilities for the future is endless. But with consumer spending and job growth moderating, and the global economic outlook weakening, sustaining positive GDP growth is likely to be an uphill battle, especially since the Fed is hiking interest rates, which will further discourage both consumption and investment spending.

Were we in a recession when GDP declined in the first two quarters of this year? Some researchers will say yes, and others no. One thing researchers seem to agree on, however, is that the released positive GDP numbers are masking deep pockets of weakness.