Report shows Minnesota’s estate tax burden is among the highest in the country

Minnesota is one of 18 states and the District of Columbia that levy either an estate or inheritance tax, often called death taxes. Among these states, a new report by the Tax Foundation shows Minnesota imposes the sixth most burdensome death tax in the country, making Minnesota a real outlier.

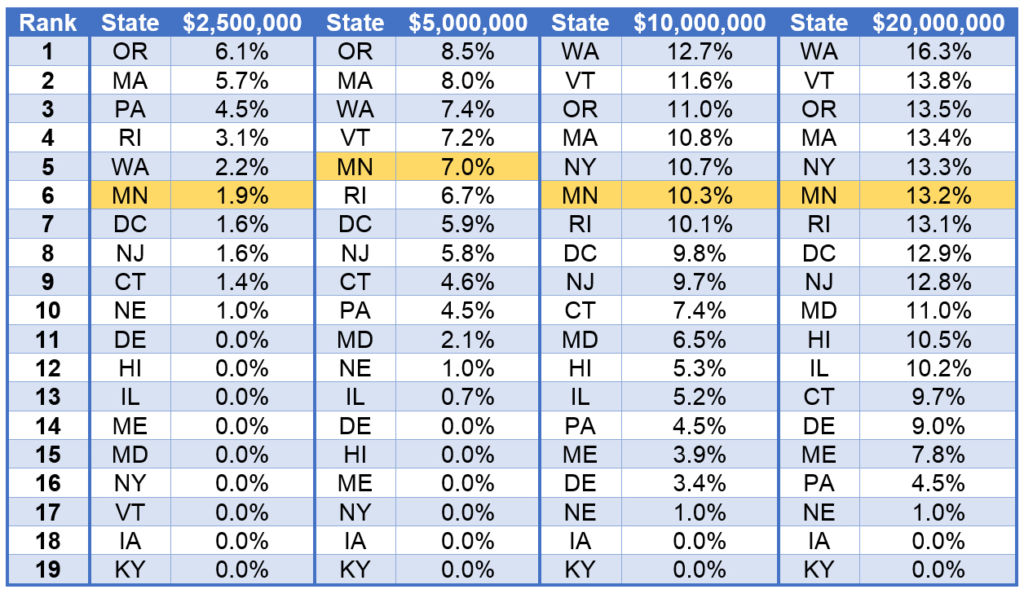

Comparing state estate and inheritance taxes is complicated because there are so many variations in how these taxes are levied. To help compare states, the Tax Foundation calculated the effective estate tax rate each state applies to four different values of estates—$2.5 million, $5 million, $10 million, and $20 million. The report also calculated effective inheritance tax rates states apply to bequests of $100,000, $500,000, and $1 million.

The table below combines the Tax Foundation information on both effective estate and inheritance tax rates and ranks states from the highest rate to the lowest rate. As the table shows, Minnesota imposes the sixth highest effective death tax rate in the country for three of the four estate/bequest values and ranks fifth for estates/bequests valued at $5 million.

Effective State Death Tax Rates Across Estate Values and

Bequest Values to Lineal Heirs by State

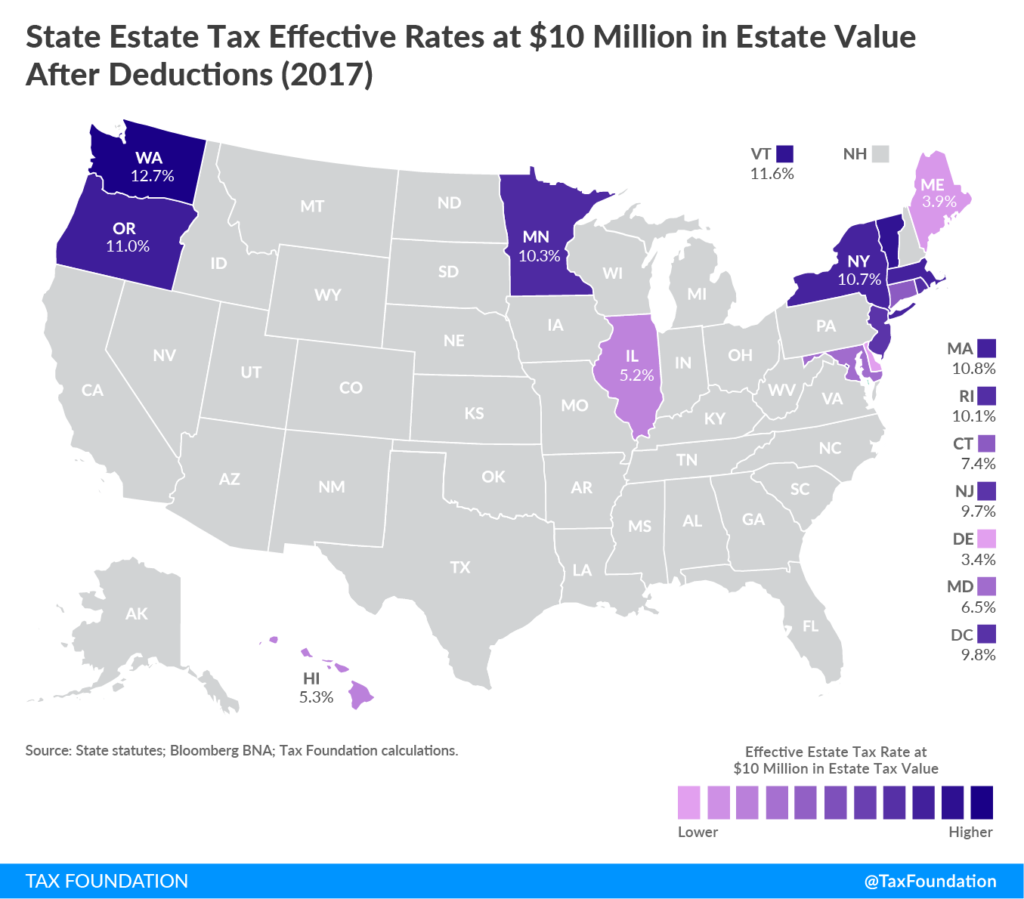

Minnesota’s estate tax burden is even more of an outlier when compared regionally. As the map below shows, Minnesota and Illinois are the only states that impose an estate tax outside the Northeast and the Northwest coasts. Minnesota is further isolated by the fact that Illinois imposes a tax on estates valued at $10 million at about half the effective rate as Minnesota.

There are economic consequences to Minnesota being such an outlier. As the Tax Foundation report explains, “Studies show that economic decision-making is, in fact, affected by inheritance and estate tax regimes.” The report then itemizes several economic ramifications, including reduced hiring, business divestiture, less entrepreneurism, less saving, less investment, lower GDP growth, and years of lost tax revenues from wealthy people moving to avoid the tax.

To this last point on people moving, wealthy people are clearly avoiding Minnesota. American Experiment’s 2016 report, Minnesotans on the Move, analyzed a new set of IRS migration data. These data irrefutably show Minnesota is losing high income earners. Looking at migration by income level between 2011 and 2014, the second largest net loss of people came from households earning $200,000 or more. The largest loss came from people earning $100,000 to $200,000. With few exceptions, this net of loss people go to lower tax states.

Pull all the evidence together—the economic studies, the economic theory, and the migration data—and it becomes clear Minnesota’s outlier status on the estate tax impacts the economy. From the perspective of many economists, the economic costs of the estate tax outweigh the modest revenue states collect. And the revenue is modest. In FY 2017, Minnesota’s estate tax brought in $130 million—just 0.6 percent of state revenues.

Many state lawmakers do understand the severe economic costs of Minnesota’s estate tax. This year legislators proposed a number of bills to eliminate or reduce the estate tax. The first tax bill vetoed by Governor Dayton would have raised the estate tax exemption amount to the federal level, which is currently set at $5.49 million compared to Minnesota’s $1.8 million exemption. As a compromise, lawmakers settled on raising the exemption amount to $3 million by 2020.

This is certainly a step in the right direction, but it’s only a small step. If other states maintained their current estate taxes, then Minnesota’s effective tax rate ranking might improve by four or five spots by 2020. However, several states ranked just below Minnesota are currently phasing in much larger reductions to their estate tax. New Jersey’s estate tax will be eliminated next year. Maryland’s exemption amount will match the federal amount by 2019 and the District of Columbia’s exemption amount is also set to reach the federal amount in 2018, so long as certain revenue conditions are met.

With New Jersey, Maryland, and the District of Columbia all reducing estate taxes by more than Minnesota, Minnesota’s effective tax rate will likely only improve relative to Rhode Island (and partially Connecticut) after the exemption amount rises to $3 million. Thus, Minnesota will undoubtedly remain an outlier without further action to reduce the estate tax.