Studies have found that Biden’s tax plan will destroy the economy – here’s why

People who tout high taxes on the rich have praised President Biden’s tax plan as fair, saying it will only impact the rich and corporations. However, numerous analyses of the tax plan show this is not so true. The plan does not just soak the rich. It affects the whole economy and all workers.

The Tax Foundation, for instance, found that Biden’s plan could do the following:

1. Decrease GDP by 1.47 percent in the long run

2. Decrease after-tax income by 1.7 percent for all taxpayers by 2030

3. Decrease the country’s capital stock

4. Reduce full-time jobs by over half a million

5. Lower the average wage rate by over 1 percent.

Similar results were uncovered by economists from the Hoover Institution.

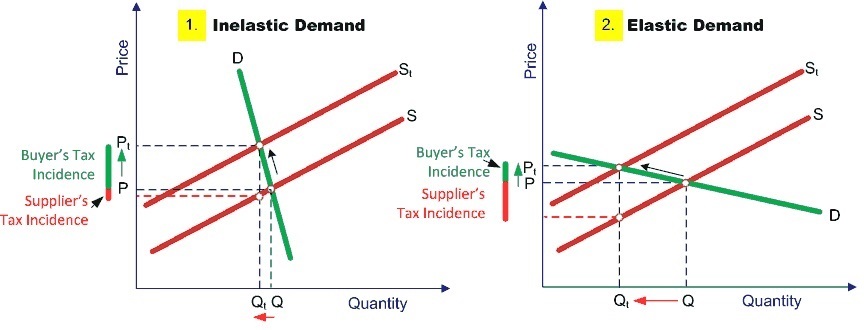

Tax incidence

If Biden’s plan is intended for the rich and corporations to pay their fair share, why is it affecting regular Americans? Consider how a sales tax hike is distributed among sellers and buyers in the market.

When the demand for a good is inelastic (graph 1), a unit increase (decrease) in price results in less than a unit decrease (increase) in quantity demanded. In this case, when the sales tax increases, sellers have a lot of wiggle room to raise prices before they start to see demand go down. Sellers end up passing the majority of the entire burden of the tax hike to consumers through higher prices.

On the other hand, if demand is elastic (graph 2), a unit increase (decrease) in price results in more than a unit decrease (increase) in quantity demanded. Sellers, therefore, are warier of raising prices. So, they tend to leave prices the same or raise them only slightly. Sellers in this case will bear the majority or entire burden of the tax increase.

The corporate tax

Capital is generally more mobile than labor (therefore, more elastic as represented by graph 2 above). So, tax increases on the rich or corporations will lead to a disproportionate response from capital owners than workers. This often minimizes the burden that investors or corporations will bear.

Workers, on the other hand, face higher costs of relocating, as they’d have to uproot their entire livelihoods to escape a slowing economy. So, even when investors pull out capital due to high taxes, workers are forced to stay in a declining economy, incurring the majority of the cost of the tax increase. This is why some research suggests that labor, not capital, bears the majority of the corporate tax burden.

Some research has also shown evidence that corporate taxes can be passed on to consumers through higher retail prices. This is particularly true for goods that have an inelastic demand.

What this means

What is fair is subjective and should never drive tax policy.

Whether Biden’s tax plan will hurt or help regular Americans, however, is something that can be objectively studied. By and by, the research evidence that progressive taxes and high taxes on corporations are not entirely beneficial for workers, even if touted so.

Progressive income taxes distort behavior, reduce investment, slow the economy, reducing income and job growth.