Tweet This: Police Pensions Ought to Be Fully Funded

There is an old saying: please don’t kill the messenger.

I was invited to testify at the Pension Commission this week. In response, a few tweets went out from the Teamsters Local 320 Public & Law Enforcement that made it clear that we have a communication problem. So, this post is written to the rank and file out there, the thin blue line that looked fierce sitting behind me Tuesday night.

The first tweet was “ Follow @mnlegTEAMSTER on tonight’s #mnleg Pension Com. Kim Crockett @MNThinkTank to testify against pensions – we will fight back!”

And the second tweet called us Chicken Little.

The Center is not making war on cops with the Pension Project. In fact, we have gone out of our way to have your back, calling out the real war on cops by Black Lives Matter and all the other politically correct and dangerous rhetoric coming from the liberal and progressive left.

Now we want to see pensions for the police fully funded.

The Center’s goal is to make sure that the promises politicians and union reps make to the rank and file can be kept, now and in the future.

Given what cops do for a living, and the fact that you are often asked to hand in the shield at a younger age than the rest of us, we must take special care to be sure that you are in good financial shape after you leave the force, whether you take another job or go fishing.

This is all underlined by the fact that the police in Minnesota do not participate in social security. For better or worse, right now your pension is it (along with whatever you save on top of your defined benefit).

If pensions are not fully funded two bad things happen: first, your retirement and that of your spouse is insecure. Second, as the pension fund has fallen behind over the years, the fund started borrowing from the future to make up for the past. That future is supposed to belong to the next generation of young police officers, not to mention our children.

There is another saying: don’t argue with math.

If you do not believe me, and want to see the numbers yourself, look at your fund here on the LCPR website.

According to the valuation reports from the actuary for PERA Police & Fire (PERA P&F) your fund is at least a billion dollars short (assets of $7.4 billion and liabilities of $8.4 billion).

The fund, however, uses unrealistic assumptions about how much the assets are going to grow (assumes about 8-8.5%), but it also has used the wrong assumptions to figure out the liability. If you used more realistic assumptions, the short fall is at least $2.6 billion, maybe more. If you read the GASB report here on page 1 (Executive Summary) you will see that the actuaries are reporting that the liability is much higher, leaving the fund short by over $4 billion.

How did this happen?

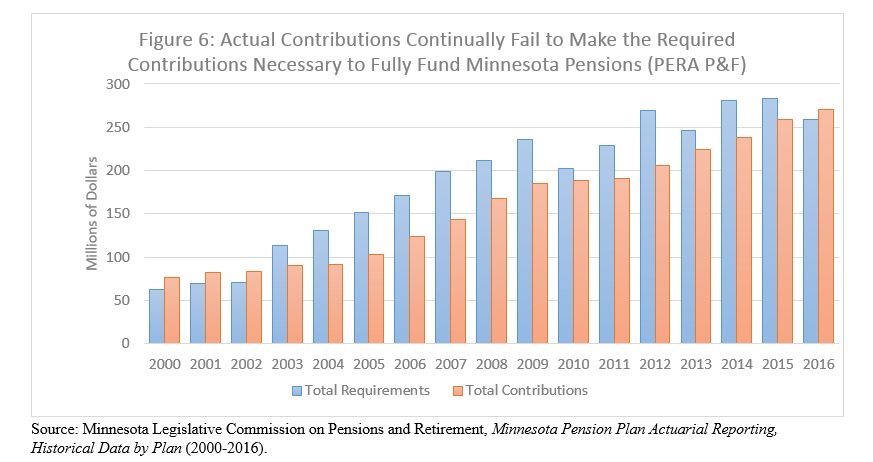

In simple terms, the contribution that you and your employer have been paying year after year fell short in two ways. First, the annual contributions were miscalculated—and not enough to cover the benefit promised. And then to make it worse, you and your employers have missed the required contribution every year since 2003 (see Figure 6 below).

Here is an imperfect analogy: your mortgage company miscalculated how much you owe and on top of that, you did not pay in full. So, it is a double whammy.

The state has also been paying out a compounding COLA to retirees, thereby depleting the assets. That is partly why you pay a chunk of your pay each month toward the unfunded liability. But that is another story for another day.

What is being done to fix this? PERA P&F has been doing better: in 2016 the contributions exceeded the annual requirement by $10 million. That is good. Keep doing that so you can ride whatever good news there is in the market. But you have a lot of ground to make up.

Here is good news for you but not great news for other taxpayers: state taxpayers have poured $9 million a year in cash into the fund since 2013 (total $36 million and counting). Also, your employers have paid “additional contributions” since 2012 totaling $62 million. That means that local taxpayers have less money to pay you more money, hire new cops, or handle other priorities.

Is this extra cash infusion working? Well, the fund is headed in the right direction, but that is not the same as being solid. You are paying 10.8 percent of your pay toward this defined benefit; your employer pays a total of 17.69 percent. Plus taxpayers are kicking in cash.

Bottom line? PERA P&F is underfunded by a big amount. The thirty-year projection is not pretty. When you are in a good mood you can read it here. Then give us a call. We can look at the numbers together.

The Chickens have come home to roost and they are not Little.