$1 billion paid family and medical leave payroll tax would hit lowest earners hardest

When Minnesota’s state Senate passed a bipartisan bill last year to cut the lowest rate of state income tax, a DFL complaint was that it was “titled (sic) toward the rich and leaves working Minnesotans behind.”

The reasoning behind this was that higher earners would see a greater decrease in their tax burden than lower earners in dollar terms. By contrast, when you looked at the impact of the tax cut in percentage terms, lower earners saw a greater cut in their income tax burden than higher earners. As I wrote at the time:

…while the income tax burden of an individual in the $150,000 to $249,999 income range would fall by $1,161, that is only a 12 percent reduction in their effective income tax burden. The burden falls by 100 percent for households in the $20,000 to $29,000 range, eliminating it completely, and by 56 percent for those in the $30,000 to $49,000 range.

The DFL’s proposed payroll tax of 0.7% to fund its scheme for paid family and medical leave (PFML) works in exactly the same way, but in the opposite direction.

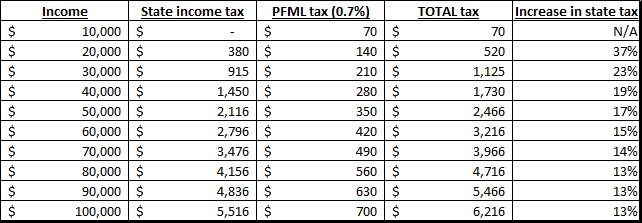

Table 1 shows the state income tax, PFML payroll tax, and total tax payable at different incomes. At an income of $30,000, for example, you owe $915 in state income tax. Under the proposed PFML scheme, you would pay a payroll tax of 0.7%, which works out at $210. Your total tax payable would, then, increase from $915 to $1,125, an increase of 23%. For someone earning $100,000, by contrast, their total tax burden would go up by a greater dollar amount — $700 — but the percentage increase would be lower — 13%.*

Table 1: Increase in state tax burdens resulting from paid family and medical leave payroll tax

By the logic employed by the DFL last year, the PFML tax is “titled (sic) toward the rich and leaves working Minnesotans behind.”

*The result is the same if we split the payroll tax between employer and employee and calculate using 0.35%. Evidence finds, however, that the incidence of payroll taxes — who actually bears the burden — falls on the worker in the form of lower wages.