High interest on credit cards? Blame strict regulations for that

Generally, no collateral debt, like credit card debt, is associated with high risk to lenders. Therefore, this kind of debt is associated with high borrowing costs, usually manifested through high interest rates.

However, starting in 2010, that risk climbed dramatically. According to new research, this trend can be explained by the new regulations lawmakers enacted following the 2008 financial crisis.

The 2008 financial crisis

To lawmakers, the crisis represented one thing: a lack of regulation in the financial sector. This led to the adoption of new laws to prevent a similar crisis. But while well-intended, these new rules have resulted in a myriad of negative results.

According to a new study by Matthias Fleckenstein and Francis A. Longstaff, new regulations raised costs for institutions issuing credit card debt. These institutions potentially reacted by passing on those costs to consumers.

As explained by the authors,

The results suggest that much of this increase may be due to the additional balance-sheet costs and capital constraints that intermediaries now face in the post-financial-crisis period. In particular, recent capital regulation may have added hundreds of basis points to the overall cost of obtaining unsecured consumer credit in the credit card market. Finally, these results can provide useful historical perspective about the pricing of unsecured household credit risk.

Bank consolidation

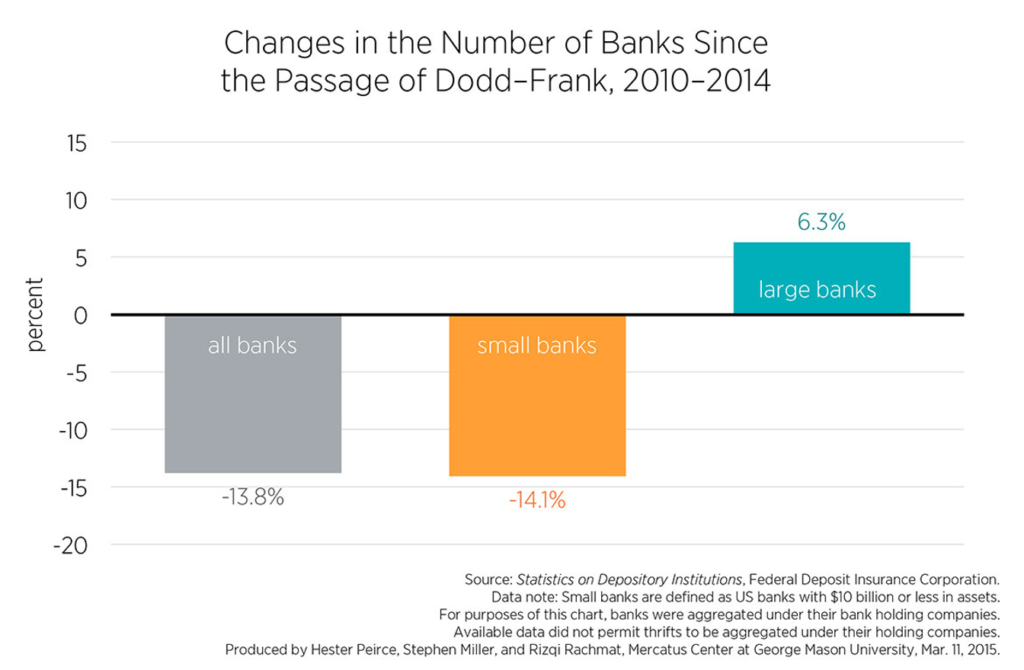

High interest on credit cards has not been the only result of the regulation that followed the financial crisis. High compliance costs that were imposed also hurt small banks, leading to the consolidation of banking institutions. Small banks have virtually disappeared in the financial sector, taking away one of the major sources of credit for small businesses.

The data shows, for example, that between 2010 and 2014, the number of small banks has declined by over 14 percent, while the number of large banks has gone up by over 6 percent. On net, the number of all banks has gone down by nearly 14 percent.

A lesson for policymakers

When it comes to policy, results matter more than intention. While well intended, regulations enacted after the great recession have hurt banks and imposed costs on consumers. This should be a lesson to policymakers.