If Wind Energy Saves Ratepayers Money, Why Does Xcel Brag About How Wind Investments Increase Profits for Shareholders?

Wind energy is supposed to be the cheapest energy source available, providing energy savings to Minnesota businesses and families.

Just read this opening paragraph of a StarTribune article, which claims that “The cost of wind energy in Minnesota, even without tax subsidies, now appears lower than that of electricity produced from both natural gas and coal.”

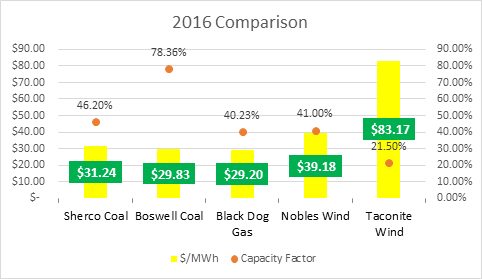

The validity of this statement can be proven false simply by using public data provided by the Federal Energy Regulatory Commission (FERC). As you can see from the graph below, the cost of electricity from wind farms is more expensive than both coal and natural gas plants.

Figure 1 The capacity factor of a power plant can also be thought of as a utilization rate. Because wind and solar depend on the weather to operate, their capacity factors are largely limited to what you see above. Coal and natural gas plants, on the other hand, can increase their capacity factors being simply burning more fuel.

Furthermore, as I laid out in a previous blog post, wind energy investments in Minnesota are the primary reason behind increasing electricity rates.

And it isn’t a surprise that Xcel Energy is bragging about those investments to shareholders.

Due to an incentive structure built into electricity rate formulas, electric utility companies desire to build more power plants whenever they are allowed to by the Minnesota Public Utility Commission (PUC) because this is how they earn profits. This is because building power plants requires capital investments, and utility companies are allowed to earn a return on these investments.

How nice is it for Xcel and its shareholders, then, that they are currently required by law to build more wind farms, thus increasing their profits?

Nice for them, but incredibly expensive for ratepayers who are forced to pay for these investments.

Xcel isn’t wasting any time taking advantage of regulatory approval to increase their profits, either. The utility company recently announced its “Steel for Fuel” plan, which is the utility company’s goal to replace fuel-based power plants with energy sources that require no fuel but only “steel,” like wind. As part of this plan, Xcel proposed the largest multi-state wind investment in the country.

Unfortunately, Xcel misinforms their customers by saying “the cost to build the wind farms is more than offset by billions of dollars in fuel savings.” The calculations made to justify claims like these are highly misleading because they do not account for the many hidden costs of incorporating wind energy onto the energy grid, including the billions of dollars spent on natural gas facilities that are needed to cover for the intermittency of wind energy, and the high cost of transmission lines to transport electricity from distant wind farms to populations centers.

Here are several instances where Xcel promotes their “Steel for Fuel” plan and other renewable energy investments to shareholders, primarily because shareholders are well aware of the profit they are going to make off of these investments.

October 2017 –

Xcel Energy delivered strong financial results in the third quarter and made good progress on our steel-for-fuel strategy that will deliver tremendous value to our customers and shareholders over the long term. We have updated our five-year capital forecast to $19 billion and refined our long-term earnings per share target to 5 to 6 percent annual growth, up from 4 to 6 percent. The confidence in our financial outlook is rooted in our track record of delivering outstanding shareholder returns, and our compelling steel-for-fuel growth strategy, where we are advancing 13 new wind farms across our service territory.

July 2018 –

As the result of excellent first-half earnings and a strong performance outlook, we have raised our 2018 full-year earnings guidance range to $2.41 to $2.51 per share, up from $2.37 to $2.47 per share. By year end, we expect to meet or exceed our earnings guidance for the 14th consecutive year. Meanwhile, we achieved important regulatory approvals for our wind projects that will bring tremendous value to our customers and shareholders over the longer term.

October 2018 –

We recently updated our base capital forecast to $19.3 billion, which reflects rate-base growth of approximately 6.2 percent. As a result of this capital investment plan and additional upside investment opportunities, we increased our long-term earnings per share growth objective to 5 to 7 percent.

Advancing our Steel for Fuel strategy, the Colorado Public Utilities Commission in September approved our Colorado Energy Plan to add 1,100 megawatts of wind, 700 megawatts of solar and 275 megawatts of battery storage. This combination of carbon-free energy would largely replace 660 megawatts of coal-fired generation at Comanche units 1 and 2… for an incremental investment of $1 billion, which has been rolled into our new base capital plan

Notice that any mentioning about increasing profit shares and capital increases are followed by laying out Xcel’s investments in wind farms.

The truth is this: utility companies are increasing their investments in renewable energy, electricity rates are rising at substantial rates, and Xcel’s earnings per share are becoming more profitable.

These are not just coincidences. Wind energy investments need to be seen for what they are, and that’s anything but beneficial to Minnesota businesses and families.