If you didn’t get a pay rise of at least 3.2% in the last year, you got a pay cut

The Bureau of Labor Statistics (BLS) released its numbers for inflation in October today and they showed inflation slowing from September’s rate of 0.4% to 0.0%, or no change in the Consumer Price Index. The inflation rate over the last 12 months fell too, from September’s reading of 3.7% to 3.2%.

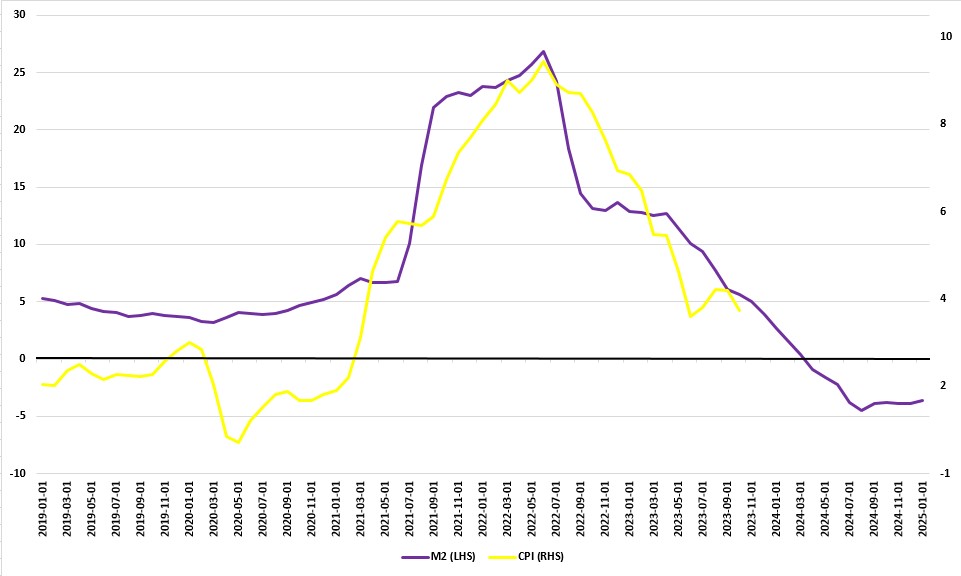

I’ve been writing for a while about how the primary driver of our recent surge of inflation was the massive infusion of new money and credit created by the Federal Reserve to keep down the costs of Federal government borrowing during COVID-19. As that money and credit growth has slowed — indeed, the broad measure of money, M2, has actually declined in every single month since December last year — so has inflation as Figure 1 shows. It takes a little time for expansions in the money supply to work their way through to higher consumer prices, so I lagged the CPI by 16 months. It isn’t a perfect fit and it isn’t smooth, but that is a pretty good match. This shows, I think, that we can expect inflation to go on slowing for a little while just yet.

Figure 2: M2 and CPI, % change from a year ago, M2 leading by 16 months

Source: Board of Governors of the Federal Reserve System and Bureau of Labor Statistics

Where do you fit into this? As we’ve noted, the rate of inflation, or the increase in consumer prices, over the last 12 months was 3.2%. So, what you paid $100 for in October 2022 will cost you $103.20 now. Or, to put it another way, $100 has lost 3.2% of its purchasing power over the last year.

If your income is the same in nominal terms, you are, then, worse off in real terms. The same applies if your nominal income increased but by less than 3.2%. The only way you came out ahead is if your nominal income increased at a rate greater than the Consumer Price Index: 3.2%. Simply put, if you didn’t get a rise in your nominal pay since last October of at least 3.2%, in real terms you got a pay cut.