Inflation is widespread because lots of central banks did the same thing

In an article summarizing the economic policies of Tim Walz and Scott Jensen — candidates in tomorrow’s gubernatorial election — Dave Orrick writes for the Pioneer Press:

The Federal Reserve — America’s central bank — has more control over inflation in the United States than any other body. The current inflation — the highest sustained inflation in 40 years — isn’t just a Minnesota thing. Nor an American thing. It’s global — a function of the rocky emergence from the coronavirus pandemic, Russia’s invasion of Ukraine, and a host of other dynamics of the economy. Too many dollars are chasing too few goods is how economists often put it.

It is true, as I’ve argued before, that the Federal Reserve is responsible for the inflation the United States is currently experiencing. But it is also true that lots of other countries are experiencing similar difficulties as the United States, indeed, for some it is worse.

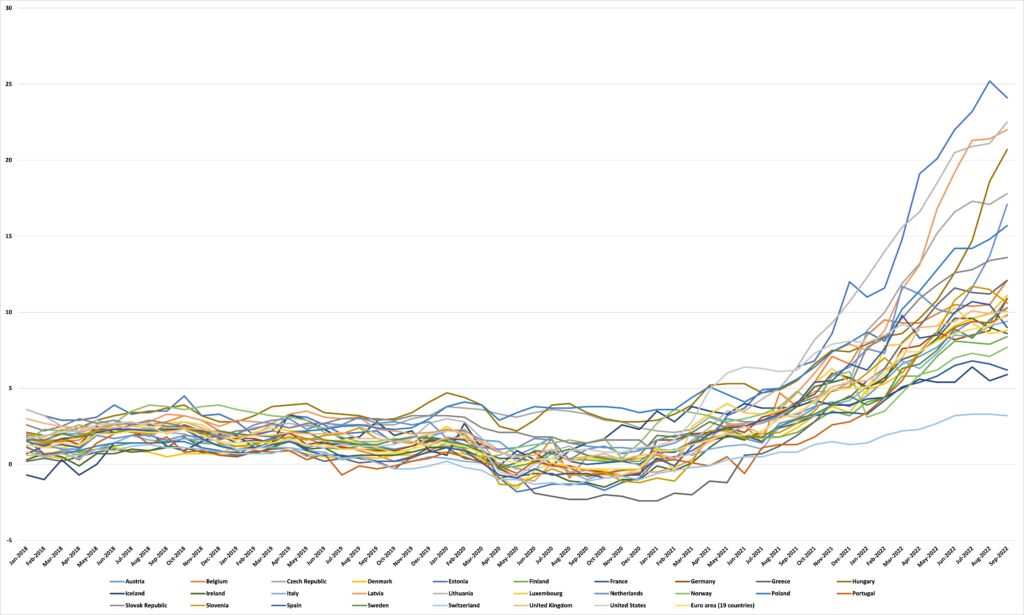

But, as with the United States, this inflation isn’t caused by Russia’s invasion of Ukraine. Figure 1 (using data from the Organization for Economic Co-operation and Development (OECD) to allow for cross-country comparisons*) shows the annual rate of change in the Consumer Price Index (CPI) for a number of countries since January 2018. We see two things: the first is that inflation is, indeed, a widespread phenomenon and the second is that it took off in early 2021, nearly a year before Russia’s invasion of Ukraine.

Figure 1: Annual inflation rate, %

If this shows that Russia’s invasion of Ukraine didn’t cause this widespread inflation, what did? As in the United States, the surge in inflation in all of the countries for which we have data was preceded by a surge in the quantity of money in the economy.

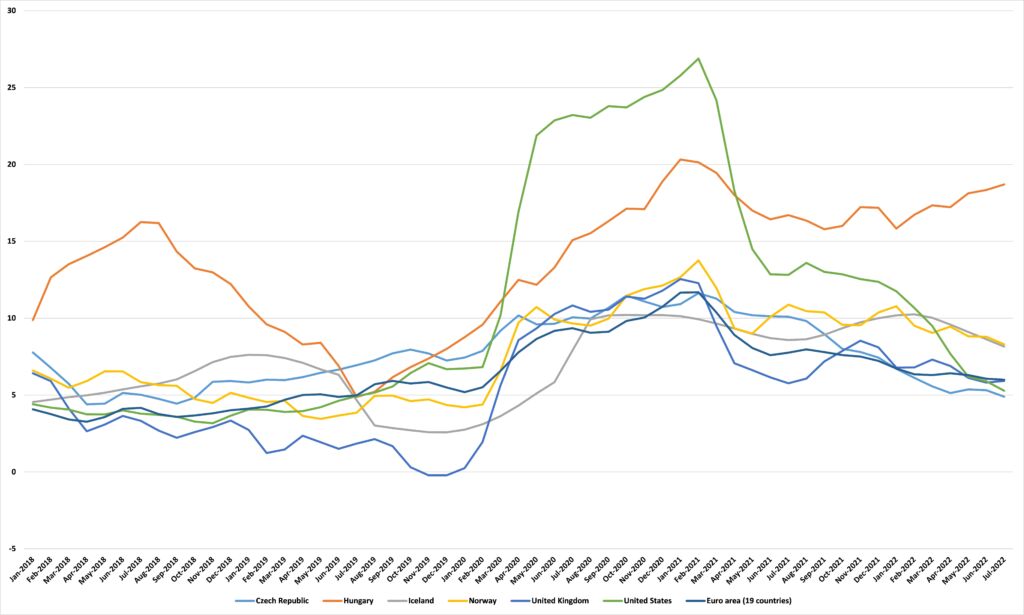

Figure 2 shows the annual rate of change in the quantity of money on the broad M3 measure. Included are only those monetary authorities from Figure 1 for which the OECD has seasonally adjusted data for ‘Growth rate same period previous year’ which, sadly, doesn’t include Switzerland, a low inflation country that might offer an interesting counter-example. In each — with the exception of Hungary — we see a steep increase in the quantity of money on the M3 measure starting in early 2020 with the United States leading the way.

Figure 2: Annual change in the quantity of money, M3, %

In each case, this was driven by central banks printing money and using it to buy government debt in order to keep borrowing costs down as those governments ran up vast bills to combat COVID-19. Everything that has happened since — the ensuing inflation, interest rate rises, and looming recession — stems from those actions. You can argue that the benefits outweigh the costs, but you must acknowledge that those costs exist and continue to grow.

*Turkey and the European Union are excluded from the jurisdictions the OECD has this data for, Turkey because its persistently high inflation is a separate phenomenon and the EU because it overlaps to a large degree with the Eurozone.