Inflation: What happens next?

This week I’ve debunked some popular explanations for America’s current bout of inflation and explained what the real cause is: the Federal Reserve’s massive expansion of the money relative to the goods and services available in the economy to spend it on. What might happen next?

If we accept that the inflation is driven by a more rapid increase in the quantity of money than in the quantity of goods and services available to spend it on, the key questions are:

- What is going to happen to money supply growth?

- What is going to happen to Real GDP growth?

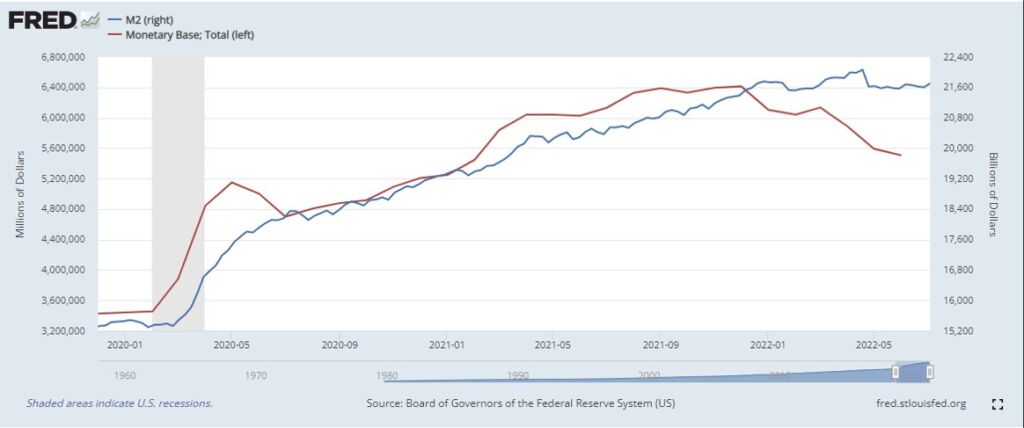

Figure 1 shows that the Monetary Base – the growth of which has driven the expansion of M2 and inflation – has been steadily falling now since December. M2 growth has been more or less flat since April. Taken together, this indicates that inflation will slow.

Figure 1

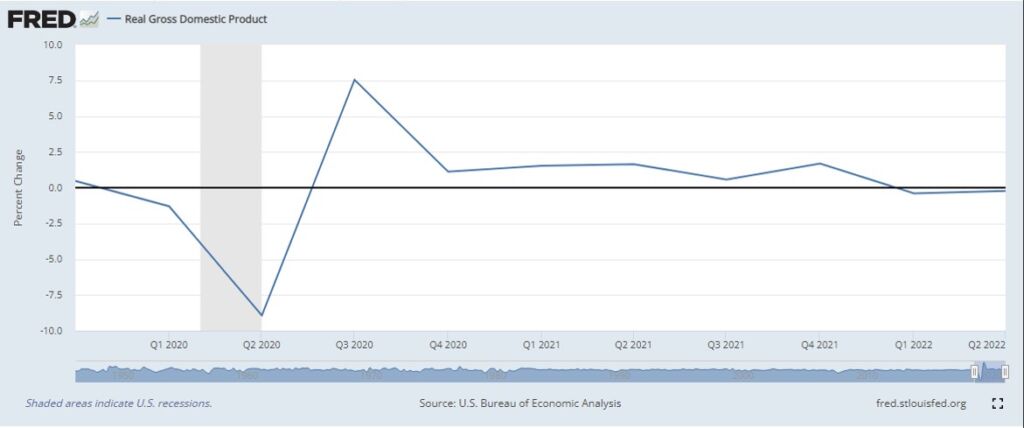

This is just as well because, as Figure 2 shows, Real GDP growth has been sluggish since its initial bounce back from COVID-19 and there is no reason to expect the economy to suddenly shift to a higher growth path.

Figure 2

Much of the heavy anti-inflationary lifting is going to have to be done, then, by monetary restraint.

If monetary growth stops than, all else being equal, inflation should stop at some point too. This only means that prices will stop increasing, not that they will fall. Higher prices will be a fact of life for Americans for some time yet.