Unleashing Minnesota’s Job Creating Potential

Updated November 20, 2014

To read this chapter as it appeared in the 2014 book, click here.

EXECUTIVE SUMMARY

The Problem

Minnesota has long been a fertile state for growing successful businesses. The roster of Fortune 500 companies headquartered in Minnesota in the 1970s testifies to the vital role the state’s agricultural, forestry, and mining resources played in setting the foundation for a strong economy. Minnesota’s history of successful business enterprises now extends well beyond the companies that sprouted from the state’s prairies and forests, proving that the people of Minnesota are the state’s most valuable resource. The diversity and success of Minnesota’s businesses now form the foundation of an enviable economy.

The biggest risk facing Minnesota’s economy: Complacency. Minnesota’s past performance does not guarantee future results. Data on the state’s workforce and economy demonstrate Minnesota cannot afford to be complacent.

Despite Minnesota’s low unemployment rate, there are weak spots in the labor market. Though Minnesota regained jobs lost during the recession more quickly than many states, job growth has fallen behind the national average in the past two years. The state’s low unemployment rate masks the number of discouraged workers who have left the workforce and people working part time because they can’t find full-time jobs. In addition, Minnesota’s labor force participation rate is declining among young people and people in the prime of their working lives.

Long-term economic trends also reveal cause for concern. Since the 1970s, Minnesota’s ten-year employment growth rates regularly beat the U.S. and Midwest averages. Yet beginning in 2005, Minnesota dropped below the U.S. average. GDP growth since 2000 has been just average. In addition, startup activity is down, IRS data show income leaving the state, and Minnesota’s workforce productivity is showing signs of weakness.

The troubling economic trends outlined above show the state must pay close attention to anything that might be undermining Minnesota’s job-creating capacity. These factors include high taxes, burdensome regulations, weak business clusters, declining capital investment, ongoing skills gaps in education, and inefficient distribution of economic development funds.

Globalization also presents a challenge. In a general sense, globalization heightens the importance of every factor just listed. In particular, having competitive tax and regulatory environments and making sound investments in the state’s labor force and infrastructure gain increasingly more importance as Minnesota tries to compete globally.

The Solution

The trends and challenges outlined above demonstrate that Minnesotans should not be satisfied with the performance of the state’s economy and job market. Many policies must be changed and new policies adopted for the state to reach its full potential. To improve Minnesota’s jobs environment, the state should focus on two strategies. First, reduce regulatory burdens on Minnesota businesses. Second, provide broad-based support for economic development that avoids picking winners and losers.

Reduce Regulatory Burdens

- Establish an Office of Regulatory Oversight in the legislature to evaluate state and local regulations.

- Require state agencies to evaluate all regulations for adverse effects on small businesses.

- Sunset state occupational regulations.

- Create an Office of Regulatory Assistance.

- Guarantee workers the freedom to choose whether to join a union.

Provide broad-based support to businesses; stop picking winners and losers

- Reduce corporate taxes.

- Create an advisory council to recommend ways to expand and improve Minnesota’s incentives for business investments.

- Change DEED’s focus from investment to support.

- Provide a tax credit to businesses for preparing workers in an apprenticeship program.

- Create an Internet-based databank to provide more detailed and objective economic and demographic analysis for Minnesota policymakers and businesses.

- Narrow the information gap between youth and employers.

THE PROBLEM

Minnesota has long been a fertile state for growing successful businesses. The roster of Fortune 500 companies headquartered in Minnesota in the 1970s—including Green Giant, General Mills, Pillsbury, Hormel, International Multifoods, Hoerner Waldorf, and 3M—testifies to the vital role the state’s natural resources played in setting the foundation for a strong economy. Still, these businesses did not succeed spectacularly by simply extracting the state’s resources. They grew by turning these raw materials into higher- value products for American consumers. This took entrepreneurial vision and a capable workforce.

Minnesota’s history of successful business enterprise now extends well beyond the companies that sprouted from the state’s prairies and forests, proving that the people of Minnesota are the state’s most valuable resource. Minnesotans’ innovative spirit and work ethic have led to remarkable business successes across nearly every sector of the economy, from food processing to financial services to retail to manufacturing to transportation. The diversity and success of Minnesota’s businesses now form the foundation of an enviable economy. As a result, economic growth in Minnesota has historically outpaced other states and served both to drive higher standards of living and to position Minnesota as a desirable place to locate a business. Currently, Minnesota’s 4.3 percent unemployment rate is the sixth lowest in the nation. Per-capita personal income is the thirteenth highest in the nation and—excluding North Dakota, which is in the midst of an energy boom—the highest in the Midwest. Minnesota also regularly appears at the top of national lists of best states for business.

The biggest risk facing Minnesota’s economy is complacency. Successful companies always pay close attention to competitors and adjust their business strategies to new realities. To thrive, the state of Minnesota must do the same. Yet many people seem too satisfied with the direction of the state. The fact is, Minnesota’s past performance does not guarantee future results. Despite Minnesota’s low unemployment rate, there are a number of weak spots in the labor market. Furthermore, several economic indicators point to long-term problems for the state’s workforce. A number of factors are converging to lessen or even eliminate many of the advantages that have long supported Minnesota’s economy. The state is slipping under current policy, but the full impact will not be felt for years. The solutions offered in this report aim to address this.

Past Performance does not Guarantee Future Results

Minnesota is home to many great companies that have been a driving force behind the state’s success. However, that strength was established years ago, and Minnesota cannot rely on those companies for tomorrow’s jobs. The state’s future economic performance depends on new companies. Recent research demonstrates the job-creating prowess of small businesses is generally limited to young startups.1 Economists Edward Prescott (a Nobel laureate who formerly taught at the University of Minnesota) and Lee Ohanian explained the importance of startups in a Wall Street Journal editorial last June:

New businesses are critical for the U.S. economy to grow because a small fraction of today’s startups will become tomorrow’s economic heavyweights. Most of today’s workers are employed at older, established businesses, but the country cannot rely on existing companies to boost the economy. Businesses have a life cycle in which even the largest and most successful reach a stage at which they stop expanding.2

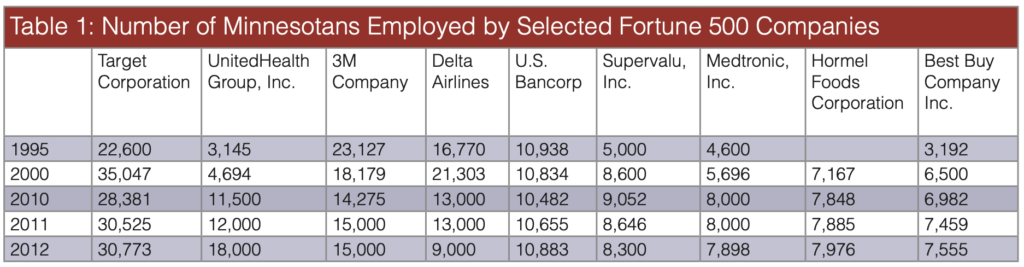

Many Fortune 500 companies in Minnesota appear to have hit this stage, at least in terms of expansion in the state. Table 1 shows the number of Minnesotans employed by the largest Fortune 500 firms with substantial business operations in Minnesota. Target, 3M, Delta Airlines, and Supervalu all report fewer Minnesota employees in 2012 compared to 2000. Most other companies report only modest gains. The state rightly takes pride in these companies, but this pride risks making Minnesotans complacent about what new businesses need to succeed. The following data on the state’s workforce and economy demonstrate Minnesota cannot afford to be complacent.

Minnesota’s Economy is Leaving Many Workers Behind

Reporters on Minnesota’s relatively low unemployment rate generally acknowledge the “the signs of strength in the job market mask a lot of economic pain that remains.”3 The fact is, today’s 4.3 percent unemployment rate exists in a much weaker job market than in November 2006, the last time the rate was as low. Lower employment growth, continued under-employment, and declines in labor force participation all point to a job market that leaves much to be desired.

Recent Job Growth is Low

During the past ten years, employment growth in Minnesota has been just average. As shown in Table 2, Minnesota’s 4.12 percent employment growth between 2004 and 2013 exactly matched the U.S. growth rate and underperformed 21 other states. Although Minnesota’s job market pulled out of the Great Recession faster than most states, annual job growth in the state has been below the national average for the past two years.

Source: Corporate Report and Twin Cities Business Corporate Lists, various years.

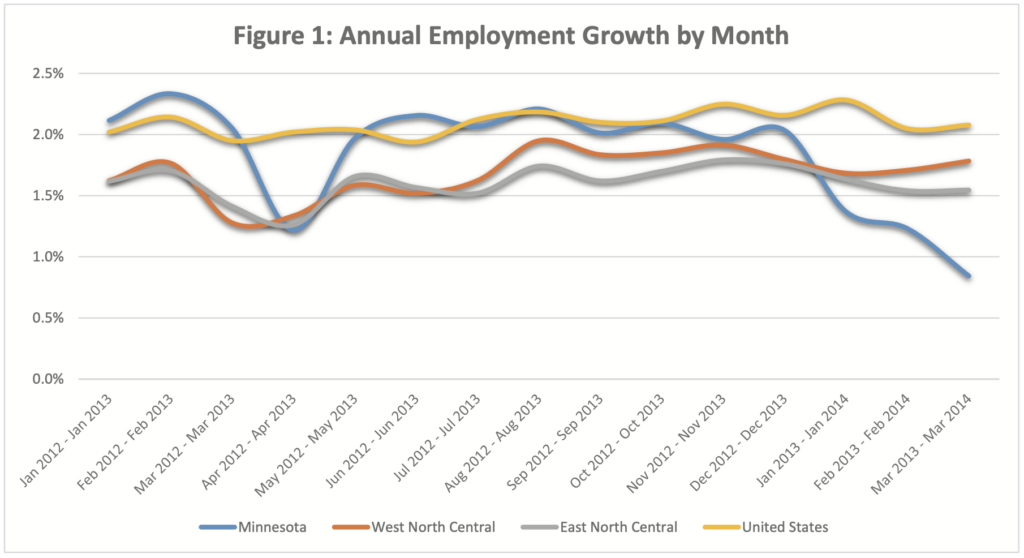

Newly released employment data suggest employment growth in Minnesota is slowing well below the national average. Annual employment growth in Minnesota, measured on a monthly basis by the Bureau of Labor Statistics Quarterly Census of Employment and Wages, began dropping below the national average in January 2014. Figure 1 shows the annual employment growth preceding each month between January 2013 and March 2014. Between March 2013 and March 2014, Minnesota dropped well below the U.S. average and ranked last among Midwestern states. Data show that less hiring is the primary issue in flagging job numbers today, not layoffs or firings.4

Employment Gains have not Made Up for Lost Growth

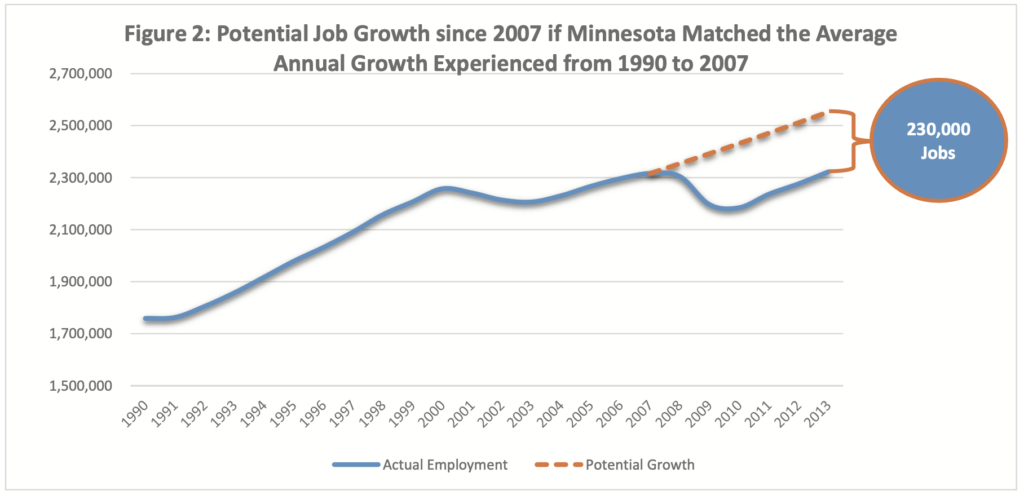

Minnesota has now recovered the jobs “lost” in the recession, but this does not account for the job growth missed during those years. If job growth had continued after 2007 at the 1.6 percent average annual rate experienced between 1990 and 2007, Figure 2 shows Minnesota would have 230,000 more jobs in 2013. This is not to say that the job losses were avoidable or even that another 230,000 jobs represents an ideal size for the job market. The point is that substantially more growth is needed for the job market to recover fully.

Unemployment Rate Undercounts the Number of Unemployed and Under-Employed

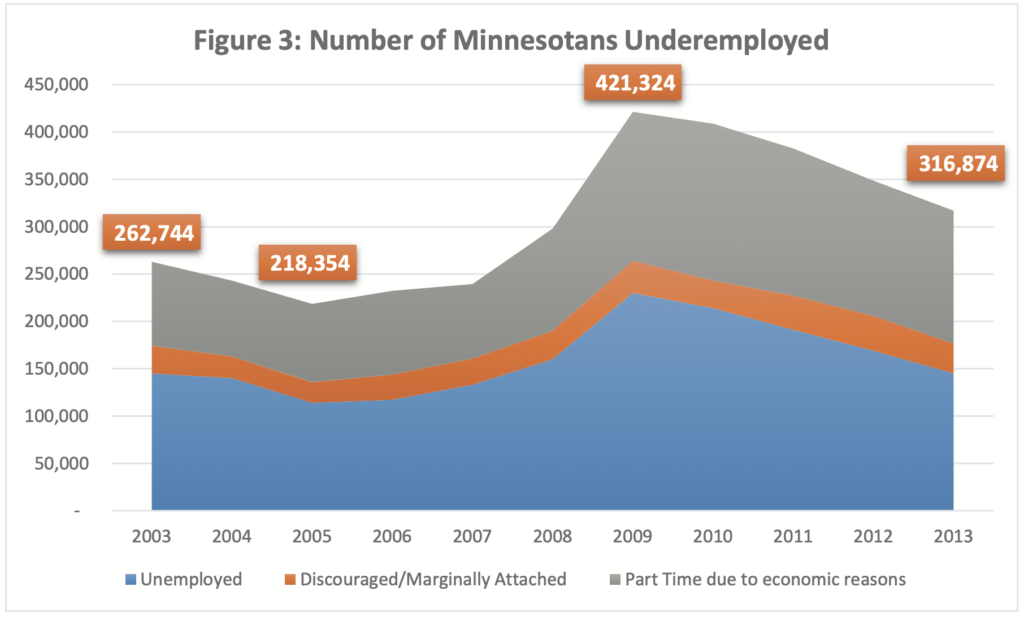

Though Minnesota’s unemployment rate is relatively low, digging a little deeper reveals a large number of people still left behind. The nominal unemployment rate does not include discouraged and marginally attached workers who have stopped looking for work, nor does it include people working part time because they can’t find full-time work. If included, these people would represent more than a doubling of the standard unemployment rate.5 Figure 3 shows there were still nearly 100,000 more people not fully employed in 2013 compared to 2005.

Source: Bureau of Labor Statistics, Quarterly Census of Employment and Wages.

Source: Bureau of Labor Statistics, Quarterly Census of Employment and Wages.

Source: Bureau of Labor Statistics, Quarterly Census of Employment and Wages.

More hallmarks of today’s job market are individuals who can’t find work for six months or more, degree-holders working at jobs where no degree is required, a dramatic upswing in part-time work, disproportionate numbers of government hires,6 and a boom in temporary labor with no benefits.7 Because the unemployment rate doesn’t account for these factors, it overstates the health of the job market. These are not “questionable and tangential factoid[s],” as Minnesota’s current governor recently argued.8 Concerns about the value of using the standard unemployment rate to describe the health of the state’s economy are shared broadly among economists.9

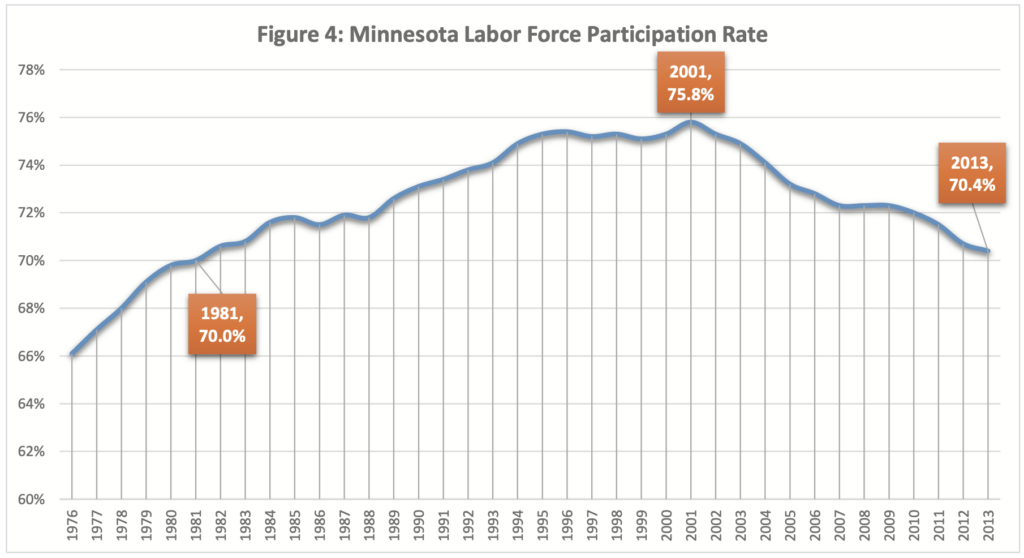

The Labor Force Participation Rate Continues to Decline

Minnesota’s falling labor force participation rate offers further evidence of weakness in the job market. In fact, workforce departure is a big factor behind the state’s declining unemployment rate. When an unemployed person leaves the market, there is one less person in the numerator of the unemployment rate, which leads to a lower rate. The state economic forecast confirms that Minnesota’s favorable unemployment rate benefits from a “sharp decline in labor force participation.”10

Source: Bureau of Labor Statistics, Local Area Unemployment Statistics.

Labor force participation, defined as the population either working or actively seeking work, is at its lowest level since 1980 in Minnesota, as shown in Figure 4. Minnesota labor force participation has declined from a high of 75.8 percent in 2001 to 70.4 percent in 2013. If today’s workforce matched the participation rate in 2000, there would be another 176,000 Minnesotans in the labor market. That’s not too far from the 230,000 jobs Minnesota would have had if the job market had maintained average annual growth through the recession.

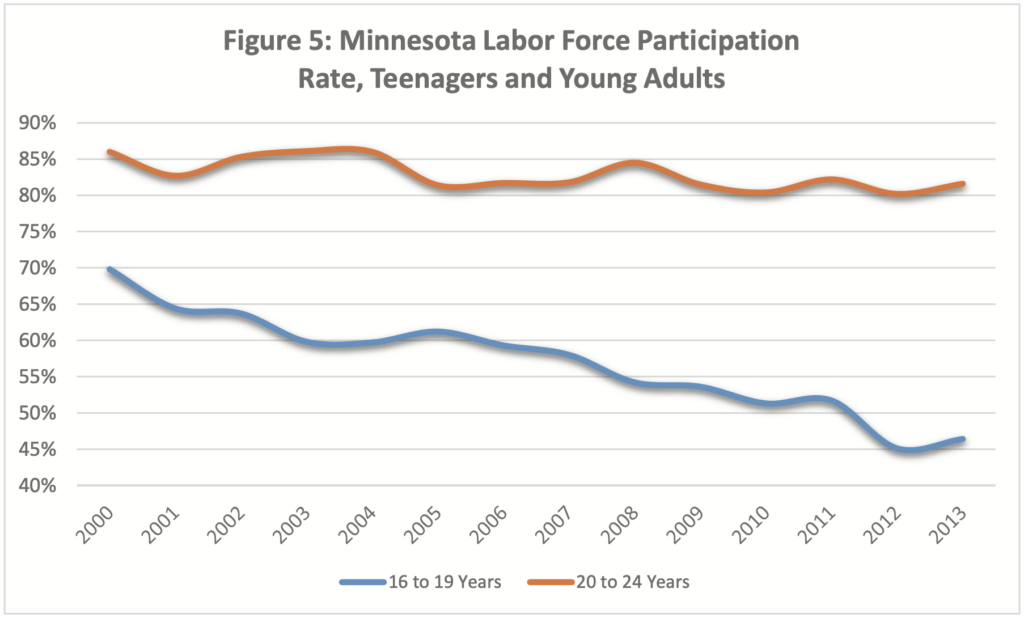

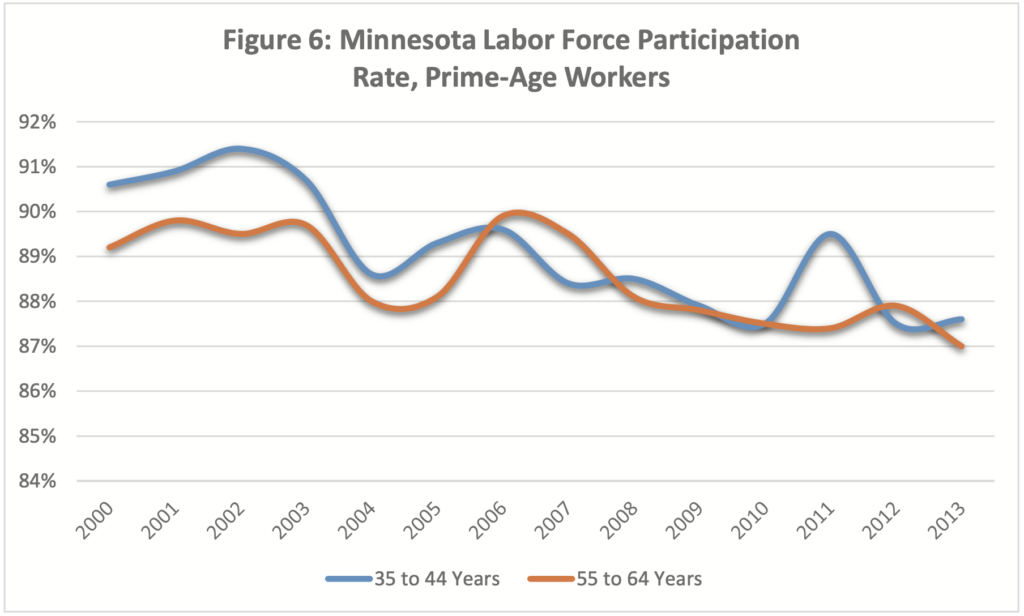

State officials blame retiring baby boomers for the much of the decline, suggesting there’s not much the state can do about it.11 Retirements account for part of the decline, but Figure 5 reveals a dramatic drop in the rate of young people participating in the labor force, and Figure 6 shows a worrisome drop among people in the prime of their working lives. The weight of evidence in the economic literature confirms economic weakness is the primary factor behind declining labor force participation rates since the start of the Great Recession.12

Source: Bureau of Labor Statistics, Local Area Unemployment Statistics.

Economic trends reveal cause for long-term concern

A number of additional economic trends are perhaps more worrisome than the current job situation.

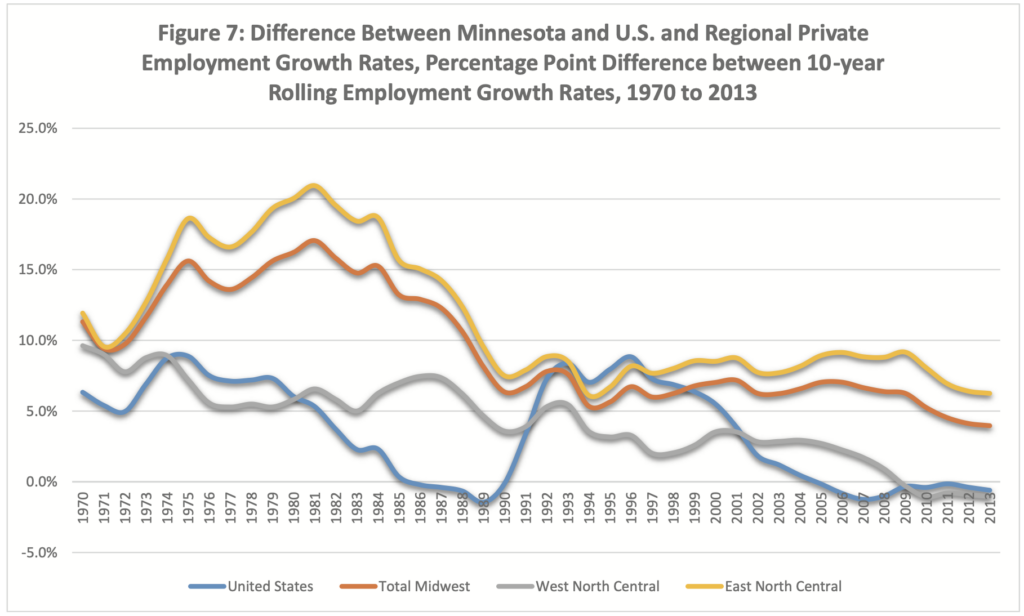

Long-Term Employment Growth Waning

To understand long-term trends in the stock market, analysts often look to ten-year “rolling returns,” which track the ten-year stock growth preceding each year. The same can be done for employment growth. Figure 7 charts the difference between Minnesota’s ten-year rolling employment growth rates and rates for the United States and the Midwest. It specifically shows whether Minnesota’s employment growth rate was higher or lower over any ten-year period ending in 1970 to 2013.

Source: Bureau of Labor Statistics, Local Area Unemployment Statistics.

Until 2005, Minnesota growth rates were consistently higher than both the United States and the Midwest, save for a five-year period between 1986 and 1990. The state’s higher than average growth in the 1990s began declining in 2000. Since 2005, Minnesota ten-year employment growth has been slightly lower than the national average. Minnesota employment growth dipped below its West North Central neighbors beginning in 2009. It would be tempting to assume the North Dakota gas and oil boom accounts for this change. However, with North Dakota removed from the region, Minnesota employment growth still would fall short in 2010, 2011, and 2013.

GDP Growth Revised Down

A little more than a year ago, local media reported Minnesota had the fifth-fastest- growing economy in the nation in 2012, according to the Bureau of Economic Analysis (BEA). Minnesota politicians understandably trumpeted this news. In June 2014, however, the BEA revised its GDP estimates, which dropped Minnesota’s 2012 GDP growth below the national average and dropped the state’s rank to 25.13 This change did not make headlines.

Source: Bureau of Labor Statistics, Local Area Unemployment Statistics.

The state’s GDP growth did accelerate in 2013, moving the state to the 13th-fastest- growing economy for the year. Still, the past two years actually reflect a longer trend of Minnesota growth swinging above and below the national average. Since 2000, Minnesota has posted seven years of GDP growth above the national average and seven years below the national average. The long-term trend shows Minnesota’s economy growing at just an average rate.

New Startup Activity is Down

Much of Minnesota’s economic strength draws from major Fortune 500 companies that are maturing. As noted previously, while they still contribute significantly to the state’s economic health, future job growth depends on new startups. Unfortunately, national data show the startup of new firms has declined from highs around 12 to 13 percent in the early 1980s to eight percent in 2010.14 The nonprofit Center for Enterprise Development rates Minnesota exactly average among the states in per-capita business creation.15 Also, Minnesota ranked 48th of all 50 states plus D.C. for entrepreneurial activity in the Kauffman Foundation’s Index of Entrepreneurial Activity for 2013, down from a rank of 10th in 1998.

Source: Bureau of Labor Statistics, Current Employment Statistics. West North Central includes IA, KS, MN, MO, NE, ND, and SD. East North Central includes IL, IN, MI, OH, and WI.

Wealth is Flowing out of the State

According to Internal Revenue Service data, over $5 billion in income moved from Minnesota to other states between 1995 and 2010.16 This has reduced the funds available for business investment, for tax collection, and for wages. Much of this is income moved to more tax-friendly states like Texas, Colorado, and Washington. For many retirees, especially wealthy ones who maintain homes in two states, the decision about where to declare “tax residency” is driven by tax policy. Given the right policy, “snowbirds” could leave wealth in Minnesota as they retire to Florida for part of the year. Populist sentiment against “the rich” notwithstanding, this wealth is needed to fund business investments, and, in turn, jobs.

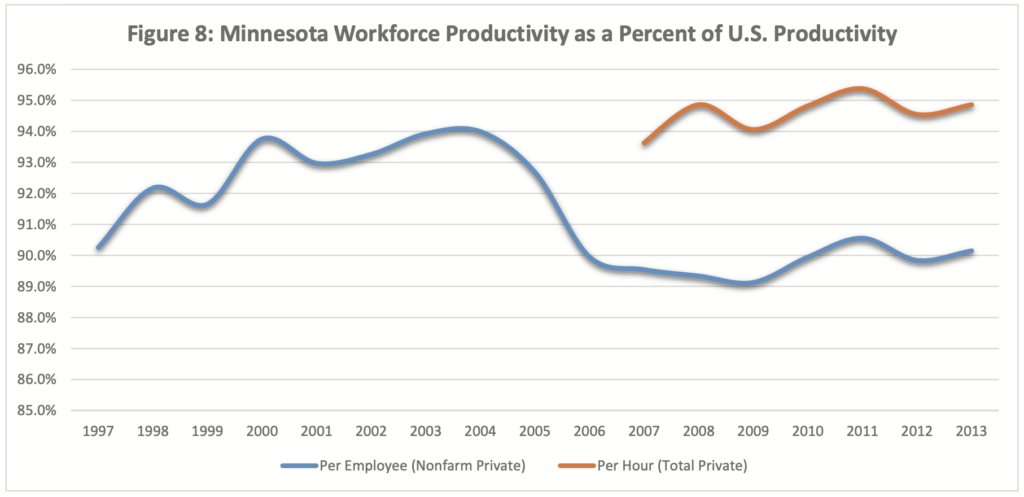

Workforce Productivity Concerns

Most people assume Minnesota workers are more productive than the average U.S. worker. After all, Minnesota’s per-capita GDP and per-capita personal income are substantially higher than the national average. Yet looking at GDP per worker, Minnesotans appear to be less productive than average U.S. workers. In 2013, GDP per Minnesota employee equaled $113,096 compared to $125,457 for the nation–about ten percent less.17

Figure 8 tracks Minnesota’s labor productivity as a percent of U.S. productivity. It shows a relative bump in Minnesota productivity between 1998 and 2005, but since 2006 productivity has held close to 90 percent of the national average. Federal data became available in 2007 to create a more accurate state-level measure of productivity based on economic output per hour worked. Minnesota’s productivity is 95 percent of the national measure. There is one bright spot. Minnesota made strong gains in manufacturing productivity between 2007 and 2013, which is what accounts for the uptick seen in Figure 8. Nonetheless, the relative decline in per-employee productivity after 2004 is still a concern.

Factors undermining Minnesota’s workforce

Faster growth is needed to offer Minnesotans opportunities similar to decades past. The troubling economic trends outlined above show the state must pay close attention to anything that might be undermining Minnesota’s job-creating capacity. Here is a short list of factors undermining the future growth of Minnesota’s workforce.

High Taxes

Minnesota is a high-tax state, and in the last two years, taxes have become considerably higher. In 2013, the Minnesota Legislature approved and the governor signed $2.1 billion in tax increases. They raised the top personal income tax rate from 7.85 percent to 9.85 percent—the third highest in the United States. A large proportion of Minnesota corporations are S-corporations that pay their taxes through the personal income tax. Minnesota is in the top ten for individual capital gains taxes and, at 9.8 percent, the state’s corporate tax rate is also third highest in the country. Adding in the federal corporate tax rate of 35 percent—the third highest in the industrialized world—makes Minnesota one of the least attractive places for business investment.

Governor Dayton and other proponents of high taxes argue that taxes are just one of many factors businesses evaluate.18 While that is true, for many businesses taxes are a substantial factor. The Dayton administration’s promotion of tax incentives to lure new businesses to Minnesota underscores the fact that taxes do matter. It is widely accepted (and covered in the Blueprint report on taxation) that higher taxes reduce the amount of taxed activity; therefore taxes are clearly a barrier to creating more jobs.

Former state economist Tom Stinson recently suggested high taxes are “not a problem” as long as Minnesota has a competitive advantage in worker productivity.19 Yet Minnesota may not have this advantage. The labor productivity data reported above place Minnesota’s productivity below the national average. Minnesota still does well on most education outcomes, but the gap between Minnesota and low-performing states is narrowing. If Minnesota is indeed losing its worker productivity advantage, then high taxes are a problem.

Sources: Author calculations based on data from the Bureau of Economic Analysis, Regional Economic Accounts and Bureau of Labor Statistics, Current Employment Statistics.

Burdensome State Regulations

A state’s regulatory environment may be the most important factor contributing to job growth within the state’s control. When asked what makes Texas such an attractive place for business, Dale Craymar, the president of the Texas Taxpayers and Research Association, highlighted the state’s regulatory environment, not the state’s low tax rates.20 While government has an obligation to protect the public, over-regulation is costly and often places heavy burdens on job producers while providing little or no social benefit. Here’s how Edward Glaeser and Cass Sunstein recently summarized the problem:

Sensible regulatory requirements can reduce illnesses and accidents, protect the environment, and maintain quality of life. But when regulations are onerous and poorly designed, they can cause serious harm—overwhelming small businesses, reducing economic growth, eliminating jobs, squelching innovation, and causing serious hardship. Many studies have found that entrepreneurship is the lifeblood of urban regeneration, meaning that business regulations that stymie entrepreneurship… can have particularly large costs, especially during times of economic difficulty. While regulation is an important tool for governments, it is vital that the authors of such rules strike the right balance, giving careful consideration to the track records of old rules and the likely consequences of any new requirements.21

Minnesota has a mixed record on regulation. The latest Thumbtack.com/Kauffman Foundation Small Business Friendliness Survey gives Minnesota high marks for the ease of starting a small business; however, Minnesota receives C grades when it comes to the general regulatory environment, employment regulations, ease of hiring, and licensing.22 By comparison, Texas garnered As and A-pluses across every indicator. Forbes ranks Minnesota’s regulatory environment as average, at 22nd.23

These rankings suggest there are ample opportunities to improve Minnesota’s regulatory climate. The processes for gaining approval to mine nonferrous metals in northern Minnesota and build the Sandpiper Pipeline from North Dakota to Superior, Wisconsin, provide concrete examples of the difficulties the state’s regulatory process can impose on businesses that would create good-paying jobs.

Weak Business Clusters

As the Minnesota Center for Fiscal Excellence noted in a recent report, “Minnesota may have a lower margin for error in being a significant outlier on business taxes and costs than other ‘high tax, high service’ peer states.”24 This is because Minnesota does not have the strong business “clusters” found in other high-tax, high-service states like New Jersey, New York, Maryland, Massachusetts, and Connecticut. Minnesota’s traded cluster strength ranks 39th nationally; these other states rank 16th or better. According to Harvard Professor Michael Porter, clusters of concentrated business activity in related industries deliver tremendous advantages to a region. Porter recently visited the Twin Cities to launch a website highlighting their importance.25

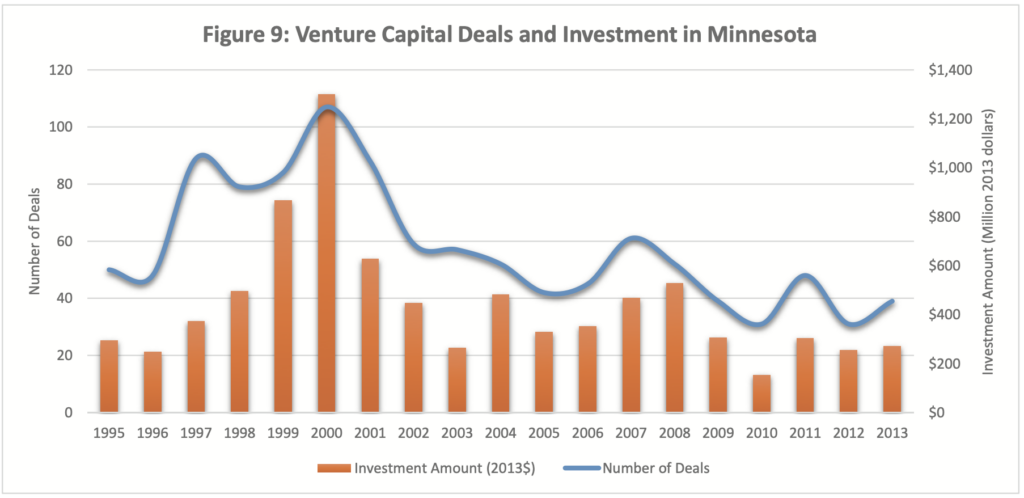

Declining Capital Investment

One reason for a lower rate of startups is a lower rate of funding. Capital investment is fundamental to business startups, and a lack of adequate capital is one of the primary reasons for business failure. A study commissioned by the Department of Employment and Economic Development (DEED) in 2013 indicated that between 2008 and 2012 venture capital investments in total dollars in Minnesota decreased 45 percent, compared to a decrease of only 17 percent for the country as a whole.26 The number and total value of venture capital deals in Minnesota since 1995 are shown in Figure 9. These data are not trending in the right direction. Investing capital in startups often involves a high degree of risk for the investor, especially for cutting-edge technologies or untried business models.27 Minnesota needs those startups and therefore must be or become an attractive place to take those risks.

Skills Gap in Education

The so-called “skills gap” is another indicator of long-term economic weakness. Though another Blueprint report addresses the topic of education, the seriousness of the issue to the long-term prospects of job growth cannot be overstated. Even though Minnesota fares better than the nation on graduation rates as a whole, there are still serious problems in education. A significant portion of graduates from the nation’s high schools lack the basic skills28 to obtain work in advanced manufacturing,29 to attend college, or to fill entry-level jobs.30

Future job growth and education are linked, and the data indicate problems in matching employees with employers. Many Minnesota firms struggle to fill positions, and students are leaving school unable to find meaningful work. The Governor’s Workforce Development Council in 2011 found that nearly half of manufacturers had positions that were unfilled due to a lack of qualified applicants, and one in eight reported having at least ten percent of jobs unfilled.31

Inefficient Distribution of Economic Development Funds

The Department of Employment and Economic Development (DEED) is empowered to offer incentives selectively for business. This is a very inefficient way to achieve growth. The engines of prosperity have rarely been fueled by government management. DEED’s economic development programs are classic examples of corporate welfare:

- They are discretionary, so they put government in the position of choosing winners and losers.

- They frequently discriminate against Minnesota businesses trying to grow organically in favor of outsiders coming with promises of jobs.

- They evaluate a small number of private sector business plans–a far larger number are never considered.

- They are the focus of endless debate and tinkering.

Government has a poor record of success in determining which businesses deserve capital; therefore, it does not make sense to put the government in the role of business investor.

Source: PricewaterhouseCoopers, The MoneyTree Report.

Globalization

As the Minnesota Department of Revenue explains, “Minnesota must compete for new jobs, business investments, and economic growth in today’s global economy, driven by rapid advances in technology, transportation, and communications.”32 To the extent other states and countries across the globe can offer higher returns on investments in capital and labor, economic growth and job growth in Minnesota will slow. In a general sense, globalization heightens the importance of every factor just listed. In particular, having competitive tax and regulatory environments and making sound investments in the state’s labor force and infrastructure become increasingly important as Minnesota tries to compete globally.

THE SOLUTION

The trends and challenges outlined above demonstrate that Minnesotans should not be satisfied with the performance of the state’s economy and job market. Many policies must be changed and new policies adopted for the state to reach its full potential. The entire Minnesota Policy Blueprint is in a real sense a blueprint of state policy reforms focused on maximizing the number and quality of jobs available to the people of Minnesota. From transportation to education to energy to taxes to families, every blueprint recommendation centers on promoting prosperity for all Minnesotans, which ultimately means connecting people to good jobs. The following recommendations provide more specific steps the state should take to maximize the job opportunities for the people of Minnesota.

To improve Minnesota’s jobs environment, the state should focus on two strategies. First, reduce regulatory burdens on Minnesota businesses. Second, provide broad-based support for economic development that avoids picking winners and losers.

Reduce Regulatory Burdens

The best opportunities to improve the business climate and grow jobs center on strategies to streamline and reduce regulatory burdens. This offers the potential for high impact at relatively low cost. Furthermore, some of these strategies are attainable in a divided political environment. Efforts to streamline state regulations have received bipartisan support over the past few years and have most recently led to a new goal to issue environmental permits within 90 days.

Recommendation 1: Establish an Office of Regulatory Oversight in the legislature to evaluate state and local regulations.

The state should establish an Office of Regulatory Oversight modeled after the federal Office of Information and Regulatory Affairs (OIRA) with one important difference: The office should be housed in the legislative branch to provide credible and effective oversight of executive agency activities. As recommended by Glaeser and Sunstein, the office should focus on “finding creative ways to institutionalize regulatory simplification and freeing up the private sector without jeopardizing public safety, health, or the environment.”33 At a minimum, the office should provide the following services:

- Periodically review the impact of state and local regulations on businesses.

- Assess the cost and benefit of legislative proposals to add new regulations.

Like the OIRA, it would likely be necessary to limit reviews to regulations with substantial economic impact or raising novel questions of policy. The office could be combined or coordinated with the Legislative Budget Office proposed in a previous Blueprint report on the state budget.

Recommendation 2: Require state agencies to evaluate all regulations for adverse effects on small businesses.

State agencies should be required to evaluate every state regulation for its impact on small business. Rhode Island enacted a law in 2012 requiring each agency to review every state regulation within four years. The agencies accomplished this task in under 17 months and identified over 250 changes to improve the state’s regulatory system.34 Minnesota should follow Rhode Island’s example.

Recommendation 3: Sunset state occupational regulations.

State law recognizes the harm state occupational regulations can impose on the workforce by requiring the proponents of any “bill proposing new or expanded regulation of an occupation” to provide a report documenting the need for the new regulation.35 This is called a sunrise law, and it aims to protect people from unnecessary and possibly anticompetitive regulations. Occupational regulations often serve only to boost incomes and provide job security for people working in regulated occupations. It is not clear whether this law is actually followed or whether it has had meaningful effect. To protect people more effectively from anticompetitive occupational regulations, the state should also implement a sunset provision that periodically would repeal occupational regulations, unless the legislature acted to reinstate them.

Recommendation 4: Create an Office of Regulatory Assistance.

Businesses could benefit greatly from more support navigating state and local regulatory processes. Instead of being an adversary, the state should be a partner and work with businesses toward a shared goal of creating a safer and healthier state. In 2002, Washington state established the Governor’s Office for Regulatory Innovation and Assistance to offer a more collaborative and supportive permitting process to businesses.36 Minnesota should create a similar office within DEED or the Department of Administration. The office should collect and report feedback from businesses to inform lawmakers on whether regulations must be improved or repealed.

Recommendation 5: Guarantee workers the freedom to choose whether to join a union.

One of the most onerous regulations the state imposes on workers is the requirement to join a union under certain circumstances. There is tremendous merit to allowing citizens the freedom to choose whether to join a union. Evidence shows that right-to-work states have fared better in job growth. One of the most highly regarded studies related to this topic was done by University of Minnesota Economist Thomas Holmes. Holmes’s study tested the effect of a state’s business climate on industry location and employment growth. While the study centered on business climate, Holmes used the existence or absence of a right-to-work law as a proxy for a state being pro-business or anti-business. Holmes compared growth in manufacturing employment between border counties, including differences along Minnesota’s border. The differences in the growth in manufacturing employment between Minnesota and its neighbors were among the most dramatic in the country. Between 1947 and 1992, border counties in North Dakota grew by 137 percent compared to 20 percent in Minnesota, in South Dakota by 138 percent compared to 27 percent in Minnesota, and in Iowa by 130 percent compared to 85 percent in Minnesota.

Provide broad-based support to businesses; stop picking winners and losers

Current state economic development policy relies heavily on tax credits, loans, and grants to specific businesses and industries. As a result, the state is heavily involved in picking winners and losers. The most notable programs include the Minnesota Investment Fund and the Minnesota Job Creation Fund. The following recommendations support shifting the state toward more broad-based approaches to economic development that would benefit all businesses equally. These recommendations focus on improving access to capital, information, and skilled workers.

Recommendation 6: Reduce corporate taxes.

Minnesota’s decline in new business starts relative to the rest of the country strongly suggests the state would benefit by increasing access to capital for businesses. The most obvious and appropriate strategy to connect businesses with capital is to tax businesses less and thereby leave businesses with more of their own money to invest. In FY 2013, the state collected about $2.4 billion from Minnesota businesses through the corporate and individual income tax.37 A portion of any reduction in these taxes should be reinvested in Minnesota businesses. Another Blueprint report, Aligning Taxes with Economic Growth, recommends eliminating the corporate income tax by 2016, lowering the income tax rate on top earners—which includes S corporations—to five percent and eliminating the statewide general tax on business property. Repetition of these recommendations here underscores how these tax reductions would increase the capital available to Minnesota businesses to invest in future jobs. Furthermore, a trend of reducing taxes would show entrepreneurs they are valued in Minnesota and would encourage them to take the risk of starting or expanding businesses.

Recommendation 7: Create an advisory council to recommend ways to expand and improve Minnesota’s incentives for business investments.

Ideally, the state would not need to be directly involved in making investments in businesses. All a state must do is offer businesses a set of general policies that provide a fair playing field to build any type of business. However, with every state in the country engaged at some level in offering tax credits, grants, and loans, it would be practically impossible for a state—especially a high-tax state like Minnesota—to avoid giving any businesses incentives. State incentives for business investments are in many ways a necessary evil.

Despite this, state incentives run a high risk of promoting inefficiency and economic cronyism. Businesses often receive incentives when they would have invested in the state anyway, the benefits of the incentives often leak out of state, incentives for one company can displace investment in another company, and incentives leave fewer public dollars for public investments.38 Thus, any state incentive must be carefully administered to avoid these negatives.

Currently, Minnesota provides tax credits for research and development expenses and startup company investments. The tax credits provide a way to increase investment in Minnesota companies in a way that minimizes economic distortions because they are not targeted at any specific company or industry. They apply generally to research and startups. To the extent Minnesota provides investment incentives, these non-targeted incentives are the most appropriate avenues. The state may be able to improve and expand on these approaches. This includes the possibility of incentives to increase the capital available to community banks to invest in local businesses.39 To do so, the state should create an advisory council to recommend appropriate ways to expand broad- based incentives and eliminate targeted incentives. The first action of the council should be to catalog the state and local incentives available to businesses across the country.

Recommendation 8: Change DEED’s focus from investment to support.

DEED was created in 2003 by the merger of the Minnesota Department of Trade and Economic Development (DTED) and the Minnesota Department of Economic Security (MDES). DEED has a multi-billion dollar budget and has a multitude of programs aimed at administering benefits in addition to economic development. Because of the merger, only a minority of DEED’s resources are focused on stimulating job growth. DEED currently offers targeted “economic development” incentives to businesses, which in 2014 resulted in a couple hundred businesses being selected out of thousands that applied (or that could have applied).40 This puts the government in the place of betting on certain business plans and discriminating against current businesses, including those whose executives believe the effort of applying will not pay. The number of plans in play is constrained by government bureaucracy, limiting growth before it can start.

Business owners are willing to take risks if there is a reasonable chance of success, and the state should want them to take those risks, because success will bring jobs. The state should encourage every business to invest in its ideas by lowering the costs associated with starting or expanding. This would put thousands or tens of thousands of potential business plans in play, vastly increasing the chance of success and leaving the risk where it belongs, on the business owner and not on the state.

DEED should be focused on supporting businesses through access to information and access to external business opportunities—both domestic and international. Relative to education and in addition to supporting present STEM initiatives, DEED should expand and innovate to support engagement by business leaders with educational institutions and should be expand and enhance apprenticeships and other partnerships that lead youth to good careers.

Recommendation 9: Provide a tax credit to businesses for preparing workers in an apprenticeship program.

Apprenticeship programs could be an important tool to close the skills gap. Instead of requiring traditional coursework, apprenticeship programs provide students with opportunities to learn skills on the jobsite. These programs take on greater importance as traditional vocational training declines. The state should not discriminate between traditional coursework and training at a jobsite. To provide more opportunities for apprenticeships, the state should offer a tax credit to businesses to train workers through apprenticeship programs. DEED should survey apprenticeship tax credit programs in other states as well as successful apprenticeship programs in other countries.41

Recommendation 10: Create an Internet-based databank to provide more detailed and objective economic and demographic analysis for Minnesota policymakers and businesses.

Policymakers and businesses require economic information to make sound decisions. While large businesses can afford consultants, small businesses and policymakers are often left in the dark. To fill the information gap, the state economist’s office, under the direction of the Minnesota Council of Economic Advisers, should create a databank to provide objective data and analysis on the state’s economy and demographics. Too often, DEED reports statistics flattering its programs or showing progress toward political objectives. Similarly, business groups tend to highlight only the information that makes Minnesota look like an attractive place to locate and grow a business. Periodic objective analysis of the state’s economy is provided by the Secretary of State in collaboration with the St. Cloud State University School of Public Affairs Research Institute.42 This recommendation envisions a similar but more robust effort that takes a more detailed analysis of demographics, economic sectors, regions of the state, and peer states. The databank should coordinate data from multiple state and federal agencies, similar to the Federal Reserve Economic Data (FRED) online data tool provided by the St. Louis Federal Reserve.

Recommendation 11: Narrow the information gap between youth and employers. Too many students leave the education system without skills to fill high quality jobs. Minnesota has a world-class system of public colleges and technical schools. Courses in needed skills are available, but that does not mean students will opt to take them.

The skills gap is in many ways an information gap. There are good, high-paying jobs that do not require a four-year college degree; for example, a skilled machinist makes about $60,000 a year.43 The state should be working to narrow the information gap that exists between youth and businesses so students who elect not to pursue a traditional college education become aware of the alternatives available to them.44

The private sector should take the lead in closing the information gap. For instance, there is a broad move nationally to sponsor student tours of local manufacturing facilities, such as the Florida Advanced Technological Education Center “Made in Florida” student tours.45 Kentucky recently began the Tech Ready Apprentices for Careers program to provide pre-apprenticeship opportunities to secondary students. Ford recently started a program of two-day externships to bring high school teachers into their facilities to provide real-world examples they can bring back to their classrooms to demonstrate how math and science is applied in the workplace.46 Colleges are also collaborating with high schools to connect students to manufacturing careers.47 Similar initiatives are underway in Minnesota, and these programs should be expanded.

Ron Eibensteiner is President of Wyncrest Capital, Inc., an investment company for early-stage technology companies in the area of telecommunications, medical devices and software. He is a long- time board member of Center of the American Experiment and a former chair.

Ted Risdall is president and chairman of Risdall Marketing Group, one of the top three independent advertising agencies in the Twin Cities. He serves on the board of Center of the American Experiment.

John Gaylord is a consultant with extensive experience as a program manager and marketing director in the Twin Cities.

ENDNOTES

1 John Haltiwanger, Ron S. Jarmin, and Javier Miranda, “Who creates jobs? Small versus Large versus Young,” The Review of Economics and Statistics, Vol. 95, No. 2 (May 2013), available at http://www.mitpressjournals.org/doi/abs/10.1162/REST_a_00288#. VDthL3l0waU.

2 Edward C. Prescott and Lee E. Ohanian, “Behind the Productivity Plunge: Fewer Startups,” The Wall Street Journal, June 25, 2014, available at http://online.wsj.com/ articles/behind-the-productivity-plunge-fewer-startups-1403737197.

3 See e.g., Annie Baxter, “Minnesota unemployment rate dips to 4.3 percent,” MPR News, September 18, 2014, at http://www.mprnews.org/story/2014/09/18/jobless-rate- august.

4 James Sherk, “Not Looking for Work: Why Labor Force Participation Has Fallen During the Recession,” Backgrounder #2722, Heritage Foundation Center for Data Analysis (Updated September 4, 2014), available at http://www.heritage.org/research/reports/2014/09/not-looking-for-work-why-labor-force-participation-has-fallen-during- the-recovery (“Unemployment remains high because new job creation dropped when the recession began and has not recovered.”); and Floyd Norris, “Fewer Layoffs, but Not Much Hiring,” New York Times, February 14, 2014, available at http://www.nytimes. com/2014/02/15/business/job-loss-numbers-are-heartening-but-hiring-remains-slow. html.

5 U.S. Bureau of Labor Statistics, Alternative Measures of Labor Underutilization for States, at http://www.bls.gov/lau/stalt.htm. At 10.0 percent, the unemployed PLUS marginally attached workers PLUS part time for economic reasons was more than double the standard unemployment rate of 4.9 percent for the third quarter of 2013 through the second quarter of 2014 averages.

6 Adam Belz, “Minnesota employers added 8,500 jobs in June,” Star Tribune, July 17, 2014, available at http://www.startribune.com/business/267596451.html.

7 Peter J. Nelson, “What else does the November Budget & Economic Forecast Have to Say?”, Center of the American Experiment Blog, December 20, 2013, at http://www. americanexperiment.org/blog/201312/what-else-does-minnesotas-november-forecast- have-to-say.

8 Ricardo Lopez, “With an economy on the upswing, Dayton is tough target,” Star Tribune, August 24, 2014, available at http://www.startribune.com/politics/ statelocal/272436491.html

9 Binyamin Appelbaum, “Central Bankers’ New Gospel: Spur Jobs, Wages

and Inflation,” New York Times, August 24, 2014, available at http://www.nytimes. com/2014/08/25/business/central-bankers-new-gospel-spur-jobs-wages-and- inflation.html?emc=edit_tnt_20140825&nlid=68358415&tntemail0=y&_r=1; and Minnesota House of Representatives Select Committee on Living Wage Jobs, Making Work Pay in Minnesota, available at http://www.house.leg.state.mn.us/comm/docs/ LivingWageJobsFinalReport.pdf (“The true degree of slack in Minnesota’s labor markets is substantially under-estimated.”).

10 Minnesota Management and Budget, Budget and Economic Forecast (November 2013), available at http://www.mn.gov/mmb/images/Budget%2526Economic_Forecast_ Nov2013.pdf.

11 Adam Belz, “State jobs picture brightens as Minnesota added 6,100 jobs in August,” Star Tribune, October 2, 2014, available at http://www.startribune.com/ business/275689201.html (quoting state labor market economist Steve Hine saying, “It’s quite safe to say that this is really a result of demographics, which also suggests that it will continue for some time”).

12 James Sherk, “Not Looking for Work: Why Labor Force Participation Has Fallen During the Recession,” Backgrounder #2722, Heritage Foundation Center for Data Analysis (Updated September 4, 2014), available at http://www.heritage.org/research/ reports/2014/09/not-looking-for-work-why-labor-force-participation-has-fallen-during- the-recovery; Christopher J. Erceg and Andrew T. Levin, “Labor Force Participation and Monetary Policy in the Wake of the Great Recession,” International Monetary Fund Working Paper 13/245 (July 2013), available at https://www.imf.org/external/pubs/ft/ wp/2013/wp13245.pdf (concluding “the post-2007 decline in [labor force participation rate] is mainly attributable to the Great Recession and its aftermath); Julie Hotchkiss and Fernando Rios-Avila, “Identifying Factors behind the Decline in the Labor Force Participation Rate,” Macrothink Institute, Business and Economic Research, Vol. 3, No. 1 (2013), available at http://www.macrothink.org/journal/index.php/ber/article/ view/3370; and Willem Van Zandweghe, “Interpreting the Recent Decline in Labor Force Participation,” Economic Review, Federal Reserve Bank of Kansas City (2012), available at http://www.kc.frb.org/publicat/econrev/pdf/12q1VanZandweghe.pdf; Daniel Aaronson, Jonathan Davis, and Luojia Hu, “Explaining the Decline in the U.S. Labor Force Participation Rate,” Chicago Fed Letter #296, Federal Reserve Bank of Chicago (March 2012), available at https://www.chicagofed.org/webpages/publications/chicago_ fed_letter/2012/march_296.cfm.

13 John E. Broda and Robert P. Tate, “Comprehensive Revision of Gross Domestic Product by State: Advance Statistics for 2013 and Revised Statistics for 1997–2012,” Bureau of Economic Analysis Survey of Current Business(July2014), available at http://www.bea.gov/scb/pdf/2014/07%20July/0714_gdp_by_%20state.pdf

14 John Haltiwanger, Ron Jarmin, and Javier Miranda, Business Dynamics Statistics Briefing: Where Have All the Young Firms Gone? Kauffman Foundation (May 2012), available at http://www.census.gov/ces/pdf/BDS_StatBrief6_Young_Firms.pdf.

15 Kauffman Index of Entrepreneurial Activity by State, 2013 p21 http://www. kauffman.org/~/media/kauffman_org/research%20reports%20and%20covers/2014/04/ kiea_2014_report.pdf

16 Peter J. Nelson, Minnesotans on the Move to Lower Tax States, Center of the American Experiment (April 2013), available at http://www.americanexperiment.org/ sites/default/files/article_pdf/MN%20Income%20Migration.pdf.

17 Author calculations based on data Bureau of Economic Analysis and Bureau of Labor Statistics Current Employment Statistics. Productivity per Employee equals Private Nonfarm GDP divided by Private Nonfarm employment.

18 See Paul Demko, “Border battle: Officials spar over tax policies,” Finance and Commerce, October 7, 2013, available at http://finance-commerce.com/2013/10/border- battle-officials-spar-over-tax-policies/.

19 Lori Sturdevant, “Minnesota state economist Tom Stinson: The exit interview,” Star Tribune, June 29, 2013, available at http://www.startribune.com/opinion/ commentaries/213593351.html.

20 Remarks by Dale Craymer at the Minnesota Center for Fiscal Excellence 88th Annual Meeting of Members (October 8, 2014).

21 Edward Glaeser and Cass Sunstein, “Regulatory Review for the States,” National Affairs (Summer 2014), available at http://www.nationalaffairs.com/publications/detail/ regulatory-review-for-the-states.

22 Thumbtack.com Small Business Friendliness Survey, in partnership with the Kauffman Foundation (2014), available at http://www.thumbtack.com/mn/#/2014/1.

23 Forbes, The Best States for Business and Careers (2013), available at http://www. forbes.com/best-states-for-business/.

24 Minnesota Center for Fiscal Excellence, Finding Our Balance: Taxes, Spending and Minnesota Competitiveness (February 2013), available at http://www.fiscalexcellence.org/our-studies/finding-our-balance-full-report.pdf.

25 Harvard Business School, “Harvard’s Michael Porter Unveils New Tool to Improve Economic Development,” September 29, 2014, available at http://www.hbs.edu/news/ releases/Pages/michael-porter-improve-economic-development.aspx; and U.S. Cluster Mapping website, at http://ClusterMapping.us/.

26 Deloitte Consulting LLP, Strategies to Support the Survival and Growth of Small Businesses in the 11 County Twin Cities Metro Area (May 13, 2013), available at https://mn.gov/deed/images/SmallBizStudy-Recommendations-Final.pdf.

27 Andrew Moylan and R.J. Lehman, “Five principles for regulating the peer production economy,” R Street Policy Study No. 26 (July 2014), available at http://www. rstreet.org/policy-study/five-principles-for-regulating-the-peer-production-economy/.

28 Minnesota State Colleges and Universities and the University of Minnesota, Getting Prepared: A 2010 Report on Recent High School Graduates Who Took Developmental/Remedial Courses (January 2011), available at http://www.mnscu.edu/ media/newsreleases/2011/pdf/1_getting_prepared.pdf.

29 ManpowerGroup, 2014 U.S. Talent Shortage Survey Infographic, available at http://www.manpowergroup.us/campaigns/talent-shortage-2014/assets/pdf/MPG_US_ TalentShortagVertInfogrphcFINAL.pdf

30 Achieve, Inc., Rising to the Challenge: Are High School Graduates Prepared for College and Work? (February 2005), available at http://www.achieve.org/files/ pollreport_0.pdf.

31 Minnesota Department of Employment and Economic Development, The 2011 Minnesota Skills Gap Survey (2011), available at http://mn.gov/deed/data/research/skills- gap-survey.jsp.

32 Minnesota Department of Revenue, Minnesota State and Local Tax System: How Minnesota compares to other states; the principles of good tax policy and how Minnesota measures up; and social and economic trends affecting the tax system, available at http://www.revenue.state.mn.us/legislativeupdate/Documents/MN_Tax_Sytem_Overview_ Jan_2013.pdf

33 Edward Glaeser and Cass Sunstein, “Regulatory Review for the States,” National Affairs (Summer 2014), available at http://www.nationalaffairs.com/publications/detail/ regulatory-review-for-the-states.

34 Office of the Governor, State of Rhode Island, “Accelerated Regulatory Reform Initiative,” at http://www.governor.ri.gov/initiatives/regulatory/; and Rhode Island Office of Management and Budget, Office of Regulatory Reform: Period Four Regulatory Look Back Report (September 26, 2014), available at http://www.omb.ri.gov/documents/ reform/regulatory-review/Period%20Four_2014.pdf.

35 Minn. Stat. § 214.002, available at https://www.revisor.mn.gov/ statutes/?id=214.002.

36 Governor’s Office for Regulatory Innovation and Assistance, State of Washington, at http://www.oria.wa.gov/; and Jason Barrett and Kevin Klowden, Effective Government and Economic Expansion: How California Is Improving Permitting and Communication to Spur Business, Milken Institute (July 23, 2014), available at http://www.milkeninstitute. org/publications/view/654.

37 Andrew Phillips, et al., Total state and local business taxes, Council on State Taxation (August 2014), available at http://www.cost.org/WorkArea/DownloadAsset. aspx?id=87982

38 See Carl Davis, Tax Incentives: Costly for States, Drag on the Nation, Institute on Taxation and Economic Policy (August 12, 2013), available at http://itep.org/ itep_reports/2013/08/tax-incentives-costly-for-states-drag-on-the-nation.php#. VDmLW3l0waU.

39 See Governor Dayton’s Small Business Capital Access Task Force: Final Report to the Governor (October 2011), available at http://archive.leg.state.mn.us/docs/2012/ other/120136.pdf ; and Kevin Klowden, et al., Investing in California: Recommendations from the Milken Institute California Summit (March 19, 2014), available at http://www. milkeninstitute.org/publications/view/626.

40 Monte Hanson, “Job Creation Fund Making a Mark,” Kenyon Leader, September 9, 2014, available at http://www.southernminn.com/the_kenyon_leader/opinion/ article_2eee88be-b471-5100-a3cc-50bba1888244.html

41 See Robert I. Lerman, Can the United States Expand Apprenticeship? Lessons from Experience, IZA Policy Paper No. 46 (September 2012), available at http://ftp.iza.org/ pp46.pdf.

42 Minnesota Secretary of State, Economic and Business Conditions Reports, available at http://www.sos.state.mn.us/index.aspx?page=1837.

43 See Dick Resch, “Outside Opinion: Apprenticeship programs can close skills gap,” Chicago Tribune, July 13, 2014, available at http://www.chicagotribune.com/ business/ct-furniture-skills-oo-0713-biz-20140713-story.html ; and Parija Kavilanz, “$100K manufacturing jobs,” CNN Money, July 23, 2012, available at http://money.cnn. com/2012/02/27/smallbusiness/youth_manufacturing_jobs/.

44 Daniel Lowry, “High School Students get on TRACK in Manufacturing,” Kentucky Association of Manufacturers, The Goods, Vol. 7, No. 5 (October 2013)

45 “Florida Leads the Nation in Number of Industry Tours for National Manufacturing Day,” FLATE Focus, October 2014, at http://flate-mif.blogspot. com/2014/10/florida-leads-nation-in-number-of.html.

46 Grace Schneider, “Ford to boost technical education for teachers,” The Courier- Journal, October 8, 2014, available at http://www.courier-journal.com/story/news/ local/2014/10/08/fords-help-jcps-training/16910057/.

47 “Alfred State to Partner with Buffalo’s Burgard High School on Advanced Man- ufacturing Early College Program,” Alfred State, July 7, 2014, available at https://www. alfredstate.edu/news/2014-07-07/alfred-state-to-partner-with-buffalo%E2%80%99s-bur- gard-high-school-on-advanced-manufacturing-early-college-program.