Minnesota should lower its corporate tax rate

Recently I wrote in support of Minnesota Senate bill 2526, introduced by Senator Ann H. Rest (DFL), arguing that Minnesota should ditch its alternative minimum tax for corporations. Today, I had the pleasure of testifying before the Minnesota House Tax committe in favor of House bill 3989, introduced by Representative Joe McDonald (R). This bill would lower Minnesota’s corporate tax rate from 9.8% to 8.8%.

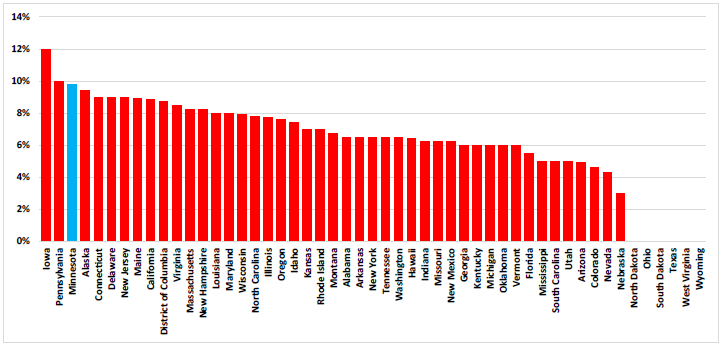

This is sound economics. As we wrote in our recent report The State of Minnesota’s Economy: 2017, Minnesota’s 9.8% top rate of Corporate Income Tax is the third highest in the United States. As Figure 1 shows, only Iowa (12%) and Pennsylvania (9.99%) have higher rates.

Figure 1 – Top rates of corporate income tax

Source: The Tax Foundation

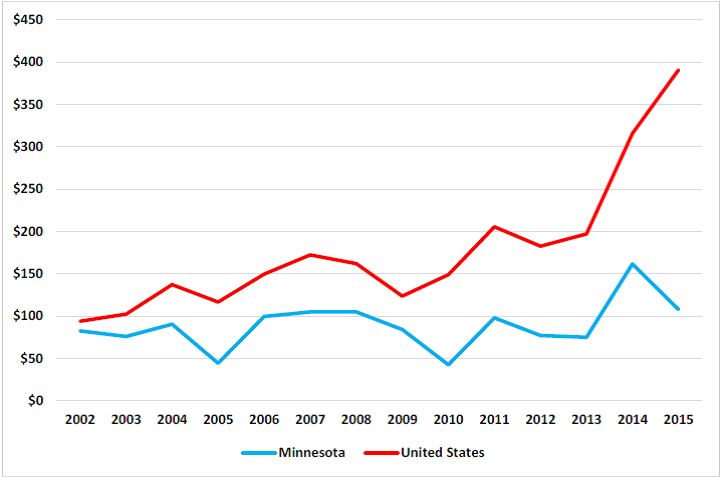

The state’s relatively uncompetitive position can be seen in its poor recent record in attracting venture capital, shown in Figure 2. In 2015, the average American worker had $391 of venture capital behind him or her. In Minnesota, the figure was just $108.

Figure 2 – Venture capital per worker, 2002-2015

Source: PwC/NVAC Money Tree Report, Bureau of Economic Analysis

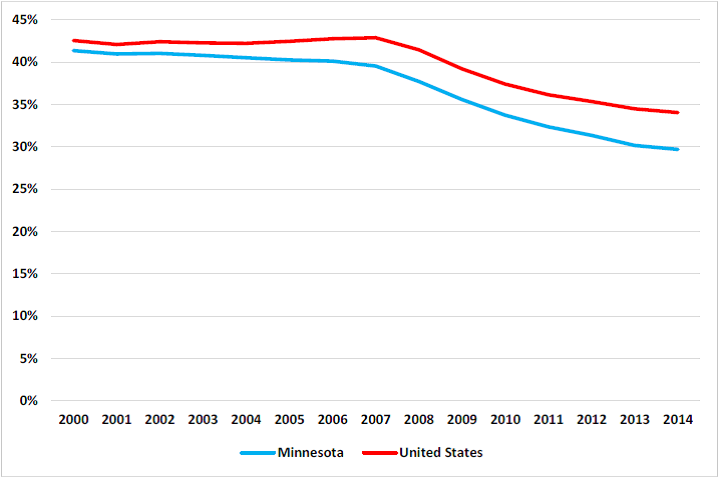

In turn, the effects of this lack of venture capital can be seen in Minnesota’s relatively poor record on new business creation. Figure 3 shows the share of new and young businesses (those aged 0 through 5 years) for Minnesota and the U.S. These businesses are of vital economic importance. They create the majority of new jobs and the small companies of today are the big companies of tomorrow. In 2000, new and young businesses as a share of all businesses were 41% in Minnesota and 43% nationally. By 2014, that number had fallen nationally to 34% but in Minnesota to 30%.

Figure 3 – New and Young Businesses as a share of all businesses, 2000-2014

Source: Census Bureau

Corporate taxes cut into the amount of money businesses have to plough back into investment and employment. Given our high rates of corporate taxation, it is no surprise that our workers have less capital per worker than the national average. This, in turn, contributes to the fact that Minnesota’s workers are less productive than the national average both on a per worker and a per hour basis. And, with Minnesota’s working population set to shrink as a share of total population, continued per capita economic growth will require the workers who remain to become more productive. This is not going to happen with the third highest corporate tax rate in America.

The Tax Foundation ranks Minnesota 46th out of the 50 states for its business tax climate. Taken together with Sen. Rest’s bill, it is encouraging to see a bipartisan appetite to address this worrying situation. Even if Rep. McDonald’s bill is passed, Minnesota will have the eighth highest corporate tax rate in the United States. The bill is a small step, but it is a step in the right direction for our state.

John Phelan is an economist at Center of the American Experiment.