Reduce tax complexity for Minnesotans

Today, we release our new Policy Briefing, ‘Reducing Tax Complexity for Minnesotans.’

This starts by noting that Minnesotans are some of the most heavily taxed citizens in the United States. On the Tax Foundation’s 2022 State Business Tax Climate Index, our state ranked 45th out of 50 states and the District of Columbia. While this is largely driven by the state’s high individual income taxes — we rank 45th out of 50 states — there are other factors dragging Minnesota down in these rankings and fixing them would help us to climb them.

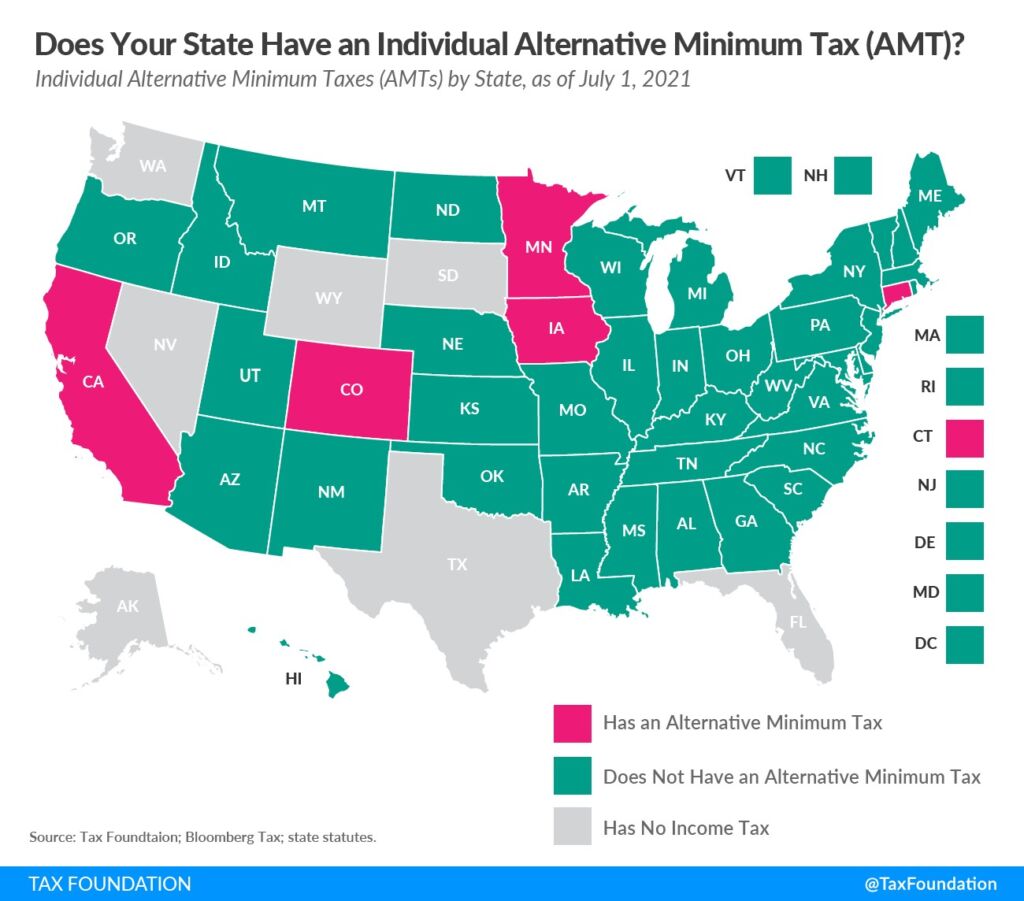

Abolish the Alternative Minimum Tax for individuals

Minnesota is one of just five states imposing an Alternative Minimum Tax (AMT) for individuals.

The federal AMT was created in 1963 to prevent high-income taxpayers from reducing their tax burden below a certain limit. It did so by requiring certain individuals to calculate their taxes twice. Several states followed the federal lead and implemented their own AMTs, which meant that some taxpayers had to calculate their tax liability four times: twice under the federal code and twice under their state’s code.

The 2017 Tax Cuts and Jobs Act increased the federal AMT’s exemption amounts and phased out thresholds through 2025, so fewer taxpayers will be required to calculate and pay the federal AMT in the future. Minnesota’s individual AMT does not conform exactly to the federal provision. It does not allow for the deduction of home mortgage interest and has one flat rate, while the federal AMT has two rates. Consequently, filers have to go through the process of calculating a state AMT even if they are no longer subject to a federal AMT.

The Minnesota AMT was estimated to raise about $23.6 million in tax year 2017, from about 9,500 taxpayers, or 0.1 percent of total state tax collections. While the number of taxpayers paying the state AMT is expected to increase in future years as real income increases and as AMT preference items, such as home mortgage interest and property taxes, increase more rapidly than inflation, the original goal of the AMT — to prevent deductions from eliminating income tax liability altogether — can be better achieved by simplifying the existing tax structure, not by establishing an alternative tax, which adds complexity and lacks transparency and neutrality.

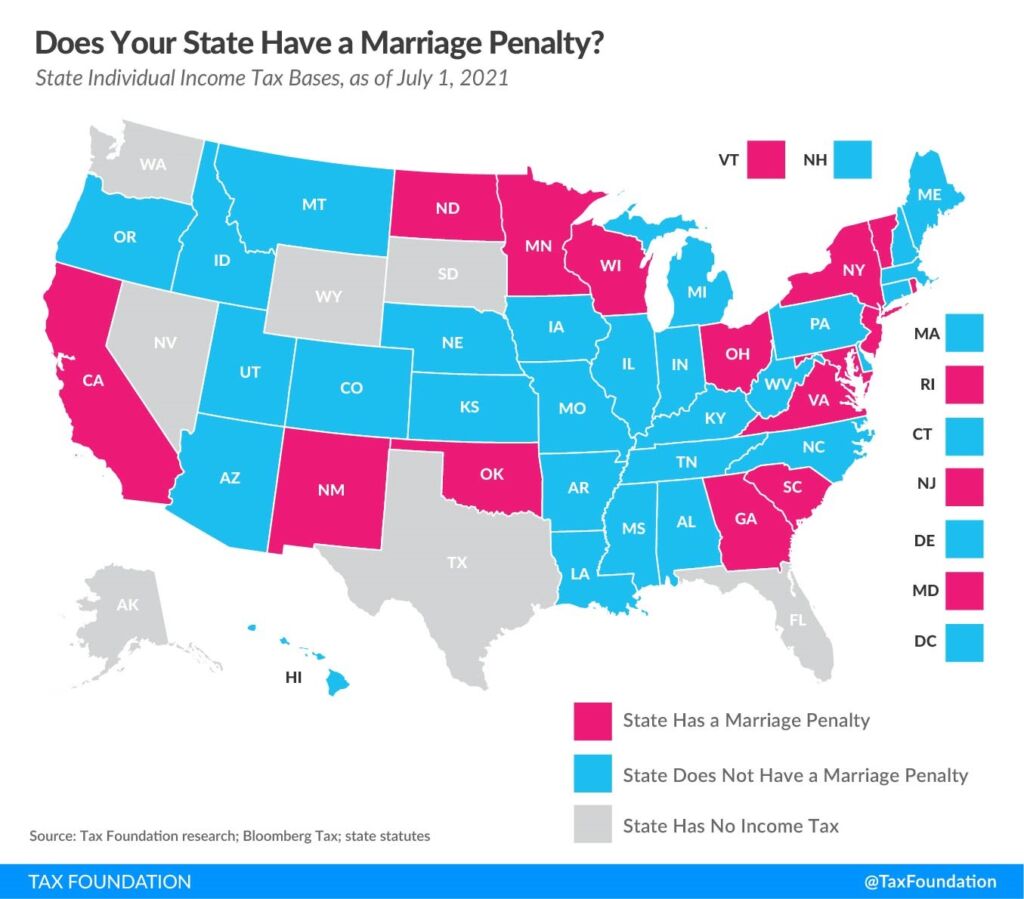

Eliminate the marriage tax penalty

Minnesota is one of fifteen states to have a “marriage tax penalty” built into its tax code.

Under a graduated-rate income tax system such as Minnesota’s, a taxpayer’s marginal

income is subject to progressively higher tax rates. When a state’s standard deduction and tax brackets for married taxpayers filing jointly are less than double those for single filers, a “marriage penalty tax penalty” is said to exist. In other words, married couples who file jointly under this scenario have a higher effective tax rate than they would if they filed as two single individuals with the same amount of combined income.

A marriage penalty tax is not only discriminatory by penalizing marriage in the tax code, but it also has negative economic consequences. Owners of pass-through businesses pay taxes on their business income under the individual income tax system. With a marriage tax penalty in place, married business owners are subject to higher effective tax rates on their business income than they would be otherwise. This is a real problem given that married couples dominate the top-earning 20 percent of taxpayers — they account for 85 percent of that category — and that that same top-earning 20 percent also has the highest concentration of business owners of all income groups. Because of these concentrations, marriage penalties have the potential to affect a significant share of pass-through businesses.

Simplify taxes for Minnesotans

Tax burdens are functions of the rates and ease of compliance with the laws. The more difficult that is, the more burdensome the taxes. The existence of the individual AMT and marriage penalty tax in Minnesota make our state’s taxes more complex and burdensome than they need be. State legislators should get rid of both.