Reduce tax complexity for Minnesota’s businesses

Yesterday, we released our new Policy Briefing, ‘Reducing Tax Complexity for Minnesotans.’ Today, we release another, ‘Reducing tax complexity for Minnesota’s businesses.’

Minnesota ranked 45th out of 50 states in the Tax Foundation’s 2022 State Business Tax Climate Index and this was partly driven by our state’s high corporate tax rates: we ranked 45th in the United States. But there are other factors dragging Minnesota down the rankings and fixing them would help us climb them.

Conform to the federal depletion schedule

Minnesota is one of thirteen states that doesn’t fully conform to the federal system for the deduction for depletion. This works like depreciation, but applies to natural resources. By imposing its own schedule, Minnesota makes its tax system unnecessarily complex.

Conforming to the federal schedule would help this.

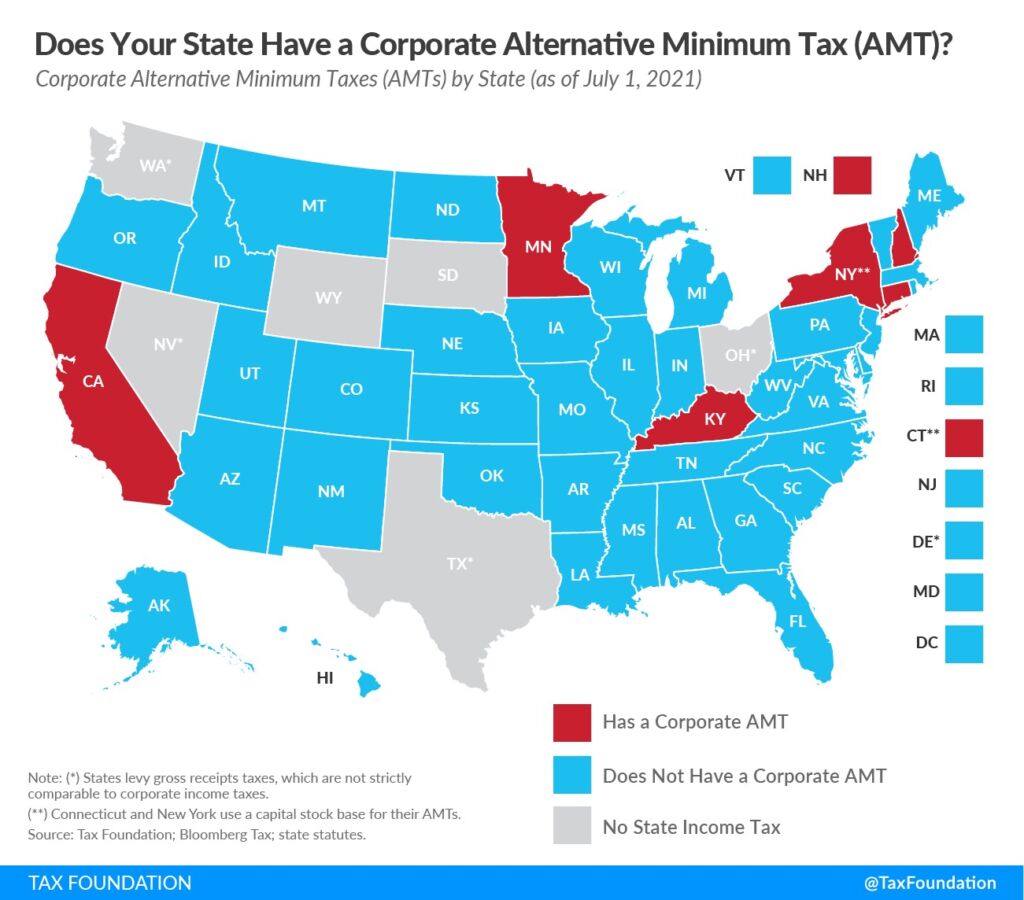

Eliminate the Alternative Minimum Tax for corporations

Minnesota is one of only six states imposing an alternative minimum tax (AMT) for corporations.

These corporate AMTs exist to prevent corporations from reducing their corporate income tax liability beyond a certain level, but they are an inefficient means of doing so. This inefficiency contributed to their repeal in several states and on the federal level.

Minnesota’s AMT requires corporations meeting certain requirements to compute their tax liability under two systems and to pay the higher amount. This undermines structural elements of the tax code, such as net operating loss provisions and deductions for business expenses. This requirement under the federal AMT imposes steep compliance costs on businesses, which in some cases is larger than collections.

With the repeal of the federal corporate AMT in the 2017 Tax Cuts and Jobs Act and the various federal modifications located throughout the Internal Revenue Code, the Minnesota Center for Fiscal Excellence (MCFE) notes that:

“…the Minnesota AMT calculation will likely be more complicated, confusing and burdensome (Is that even possible?) to taxpayers, if it remains. Practitioners are currently required to prepare additional forms calculating AMT, AMT credits, and AMT NOLs

[Net operating losses], which also requires additional time and resources for the Department to audit.”

MCFE also points out that:

“…the last time [Minnesota Department of Revenue] published a corporate income tax bulletin (about a decade ago) the corporate AMT constituted about 1% of state corporate income tax collections. Given the current circumstances, that’s not worth retaining.”

Reduce tax complexity for Minnesota’s businesses

Tax burdens are functions of the rates and the ease of complying with the laws. The more difficult compliance is, the more burdensome taxes are.

Both the failure to conform to the federal depletion schedule and the existence of the corporate AMT make Minnesota’s taxes more complex and burdensome. State legislators should conform to the federal depletion schedule and abolish Minnesota’s corporate AMT.