Want to eliminate the income tax? Start by cutting it

From A to Z

Last week I asked ‘What do states without an income tax do?‘ They get by, is the short answer: states do not need an income tax to thrive. So, if that is our ultimate destination in fiscal policy, how might we get there?

As I noted recently, Minnesota’s state government imposes a greater share of the state and local tax burden than in all but two other states and it takes a much greater share of that revenue in income tax than most other states. Eliminating the income tax would have to be, then, a longer term project. But “a journey of a thousand miles begins with a single step”, as the old Chinese proverb goes, and the first step on the road to no income taxes in Minnesota has to be lower income taxes in Minnesota.

Go to B

This goal is eminently achievable. In our report ‘It’s Our Surplus: Give It Back!‘ which we released in February, we used fiscal forecasts from Minnesota Management and Budget’s (MMB) November 2021 forecast and estimates from the Department of Revenue (DoR) on the revenue effects of various tax rate changes – their Budget Options – to offer suggestions on how the state government could leave the excess money it was forecast to take from the state’s citizens in their pockets. Using MMB’s updated estimates from July, 2022, and the DoR’s Budget Options from February, 2022 (these are not updated as regularly), we can update the exercise.

Table 1 shows how estimates of Minnesota’s state government revenue and spending have evolved over the last couple of years. You may recall that, in November, 2021, the surplus for the 2022-2023 biennium was estimated at $7.7 billion and that in February, 2022, this jumped to $9.3 billion. But this is not the total amount of new money available to be either spent or cut. For that, you have to turn to the Planning Horizon estimates, and that is what is shown in Table 1.

Table 1: Forecast Minnesota state government budget balances

What is striking here is that the forecast surplus for the 2022-2023 and 2024-2025 bienniums were lower at the End of the 2022 Regular Legislative Session in July, 2022, than they were at the time of the previous forecast in February. In both cases this was because of falls in forecast revenues – down 1.1% from February to July for 2022-2023 and 1.2% for 2024-2025 – and increases in forecast spending – up 3.0% from February to July for 2022-2023 and 0.5% for 2024-2025. In short, the forecast surpluses have shrunk from February to July because of lower forecast revenues and higher forecast spending.

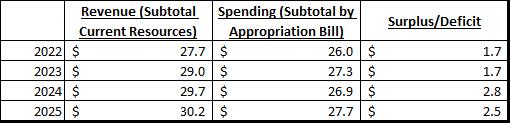

This gives less room for tax cuts but does not eliminate it entirely. Table 2 shows forecast annual state government revenues, spending, and the surplus or deficit annually using the July, 2022, forecast. This figure for the surplus — $1.7 billion for 2022 rising to $2.5 billion in 2024 — gives you the amount of revenue you can cut without touching spending. This is the smallest step towards eliminating the state income tax.

Table 2: Minnesota state government forecast revenue, spending, and deficits ($ billions)

Using the DoR’s Budget Options sheet for February, 2022, we can see that there are various possible ways that the state income tax could be cut by the amount of the forecast surpluses in Table 2. We will outline two.

A uniform cut across all rates

A one percentage point cut in each of Minnesota’s state income tax rates, for example, would reduce income tax revenues by $2.1 billion annually. This would be viable in both 2024 and 2025, on current numbers. Cutting each rate by 0.8 percentage points would lower revenues by $1.7 billion, so would be viable in 2022 and 2023. One idea then, perhaps the simplest, would be a 0.8 percentage point cut across the board in 2022 and 2023 rising to 1.0 percentage points in 2024 and 2025.

Concentrating cuts in the lowest rate

Another option is to concentrate the cut on the lowest income tax rate, 5.35% on income up to $20,525 annually if you’re married and filing separately or $41,050 is you’re married and filing jointly.

If we cut this rate to 3.05%, revenues would fall by $1.7 billion, so this measure would be viable in both 2022 and 2023 on current numbers. If we reduced it further, to 1.85%, revenues would fall by $2.5 billion annually, so this would be viable in 2024 and 2025. A second proposal, then, would be to cut the lowest tax rate to 3.05% in 2022 and 2023 and again to 1.85% in 2024 and 2025.

Pros and cons

Any such proposals have arguments for and against, and these are no exception. Economists often like to differentiate between positive – what is – and normative – what ought to be – questions. The numbers provided by MMB and the DoR allow us to answer the positive question of what the revenue effects will be from each of these measures. The normative question, which of them we should pick, is, thankfully, for the politicians.