Slashed growth forecasts show that inflation isn’t rising because the economy is booming

Last week, the Financial Times reported:

The pace of US consumer price growth pushed higher in September, hovering at a 13-year high as inflationary pressures drove up the cost of food, energy and rent.

The consumer price index published by the Bureau of Labor Statistics on Wednesday rose 5.4 per cent in September from a year ago, slightly higher than the annual increase reported for August. Analysts had expected a 5.3 per cent increase.

On a monthly basis, prices climbed 0.4 per cent, up from the 0.3 per cent a month earlier. Stripping out volatile items such as food and energy, “core” CPI ticked up 0.2 per cent from August. That compares to the previous month-on-month increase of 0.1 per cent, and maintains an annual pace of 4 per cent.

…

Food prices jumped a significant 0.9 per cent for the month, and shelter costs were also higher. Together those two categories accounted for more than half of the monthly increase in the headline figure.

The “food at home” index increased 1.2 per cent over the month as all six big grocery store food group indices rose, bringing the annual increase to 4.5 per cent. Dining out costs also rose, up 4.7 per cent for the year.

…

Energy prices rose 1.3 per cent in September, and are up 24.8 per cent for the year. On Wednesday, the US Energy Information Administration separately forecast a sharp rise in domestic heating bills this winter, as a global energy crisis begins to reach American consumers.

This is pretty grim reading. Or is it? There are those, mostly connected to the Biden administration, like White House Press Secretary Jen Psaki, who think that these rising prices are a good thing because they show that the economy is bouncing back vigorously from the COVID-19 pandemic:

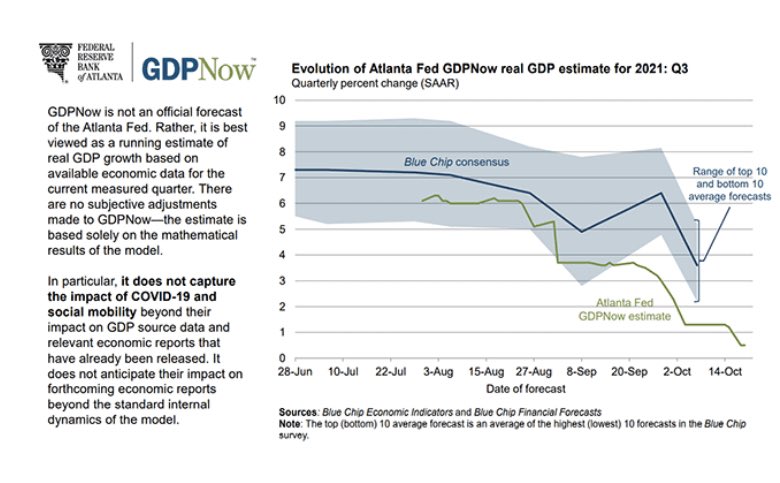

But it isn’t clear that the economy is bouncing back all that vigorously anymore. Yesterday, the Atlanta Fed’s GDPNow tracker downgraded its forecast for real GDP growth in Q3 2021 to just 0.5 percent. This has fallen from a forecast of 6 percent in late August, as the chart below shows:

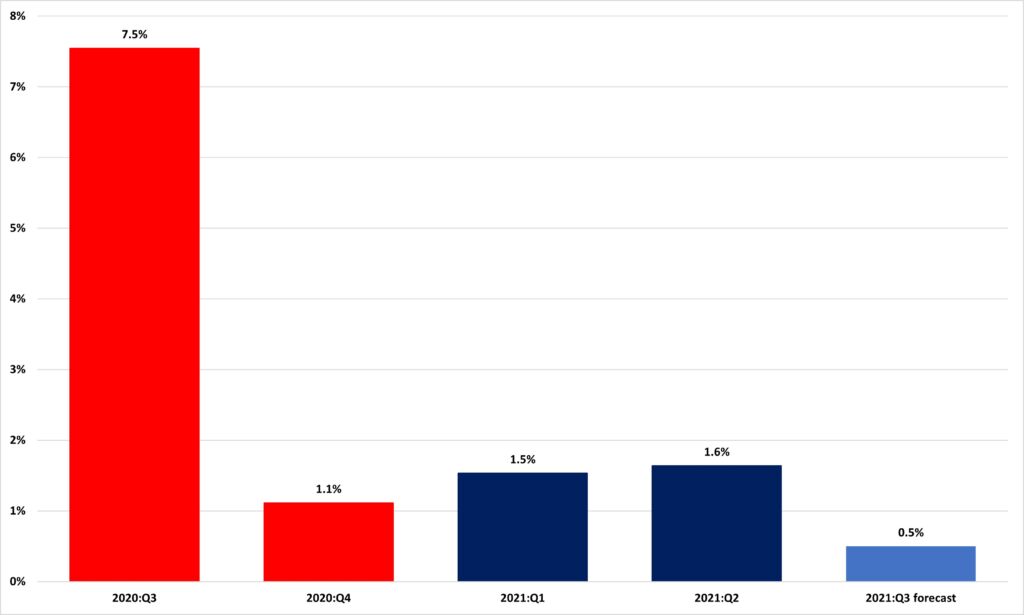

This would represent a distinct slowdown in growth, not the vigorous recovery Jen Psaki is seeing. Indeed, as Figure 2 shows, it would be the slowest quarterly rate of GDP growth since the economy returned to growth in the middle of 2020.

Figure 2: Real GDP growth rates

Source: Bureau of Economic Analysis and Atlanta Fed

A couple of week ago I quoted the economist Milton Friedman:

Inflation is always and everywhere a monetary phenomenon in the sense that it is and can be produced only by a more rapid increase in the quantity of money than in output.

As measured by M2, the quantity of money is still increasing at double digit rates from month to month. At the same time, output growth — real GDP — seems to be slowing. If Friedman was right, then inflation could get worse before it gets better.