Inflation continues to fall as the money supply shrinks

In November, I looked at where inflation might be headed and suggested that “The answer is ‘down,’ and perhaps reasonably sharply.” Looking at it again in January, I saw “a sharp slowing of inflation ahead.” Since then, the year-on-year rate of increase in the Consumer Price Index (CPI) has fallen from 6.3% to 4.1% in May, the lowest rate since April 2021, as Figure 1 shows. So far, so good for those forecasts.

Figure 1

What led me to this forecast was the same observation that led me to forecast the coming of inflation back in 2021, or at least to be less sanguine than many policymakers. This was the observation of a close relationship between the rate of growth in the CPI — inflation — and the rate of growth in the money supply.

On the broad, M2, measure, the money supply in the United States rose by 38.8% from the first quarter of 2020 to the second quarter of 2022 but real Gross Domestic Product (GDP) – the amount of goods and services available to spend that money on — only increased by 4.8% over the same period. The result of relatively more money chasing relatively fewer goods and services was inflation.

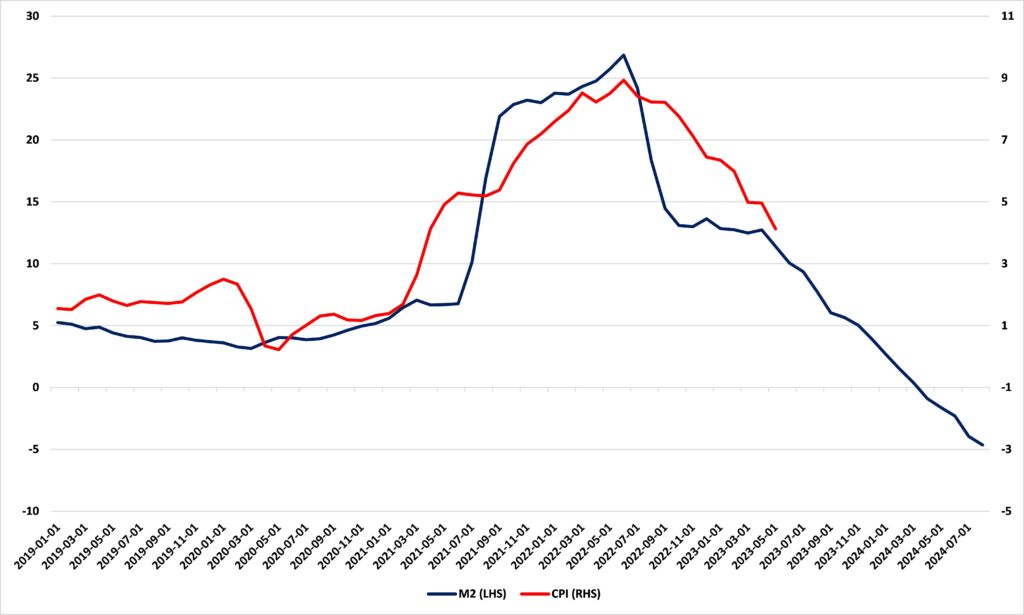

Figure 2 illustrates this relationship. Because it takes some time for money to swill its way through the economy and bid prices up, I have lagged the CPI by 16 months. We see a sharp acceleration in the rate of money growth followed by a sharp acceleration in the rate of growth in the CPI, inflation.

But we also see that, more recently, the growth rate of the money supply has collapsed. Indeed, the money supply has shrunk in every month since August 2022 and is now down by 4.7% from that peak. This might not sound like much, but it is unprecedented, at least since 1960. Until December 2022, M2 had never recorded a year-over-year decline: it has done so in every month since then.

Figure 2: M2 and CPI, % change from a year ago, M2 leading by 16 months

Looking forward, this leads me to stick with my forecast of falling inflation. It won’t be smooth, there might be some bumps and stops on the way, but the direction will be unmistakably down, I think. This does not necessarily mean that prices will fall, inflation is the rate of increase in the price level, not the level itself. Of course, if the CPI follows M2 into negative territory, you might see prices fall.

What does this monetary contraction — unprecedented since at least 1960 — mean for the American economy? I’ll look at that next week.